Stress Test Investment Plan Before You Trust It

A plan can look convincing when the projection is calm. The real test is what happens when markets fall early, recovery takes longer, inflation reduces purchasing power, fees drag the result, or your contributions become harder to maintain.

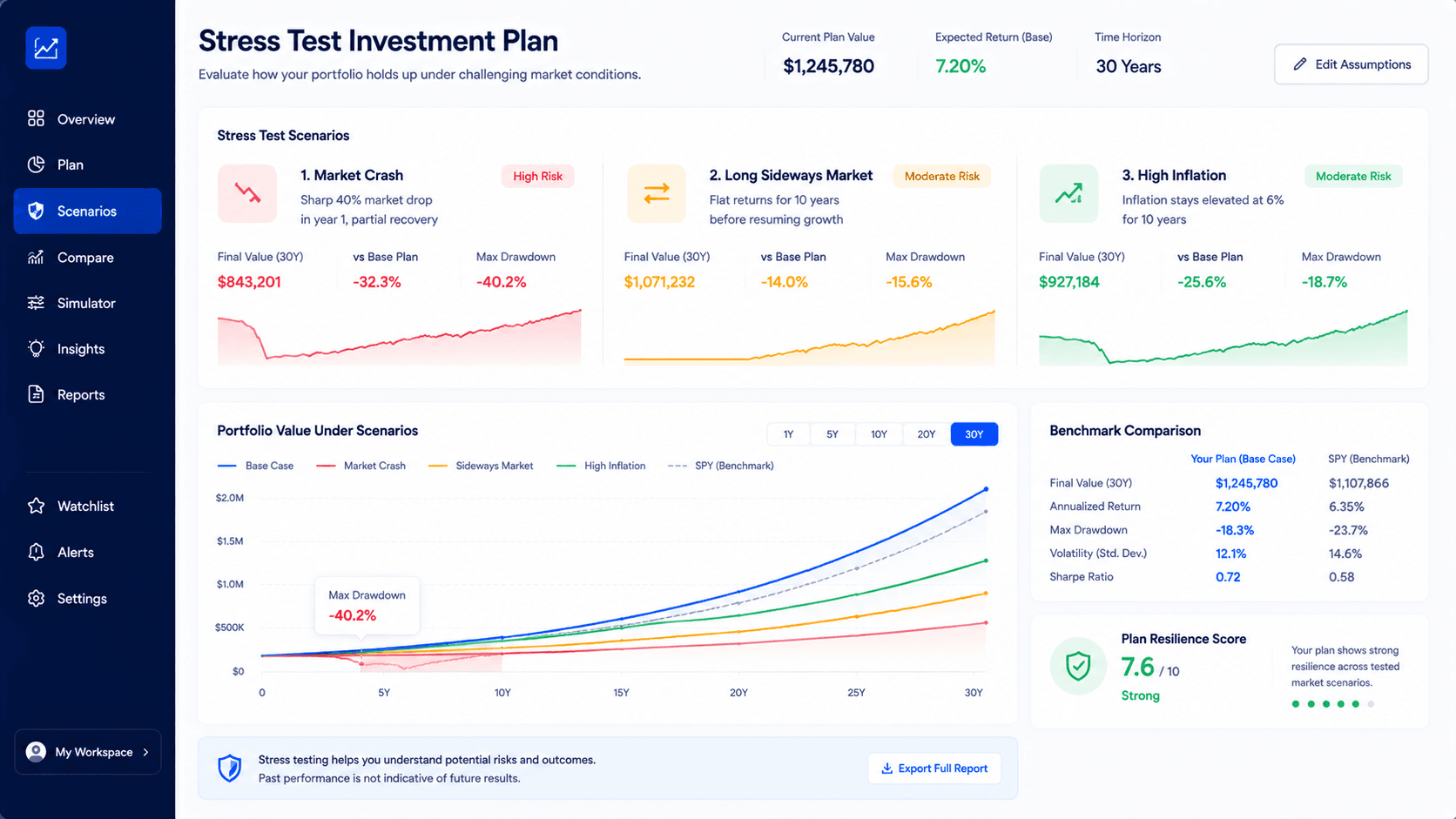

A stress test turns a projection into a decision.

To stress test investment plan assumptions means testing the same portfolio under difficult but realistic conditions before trusting the result. Instead of only asking what the balance could become, you ask how the plan behaves when the path becomes uncomfortable.

The goal is not to predict the next crash. It is to understand whether the plan remains usable if returns arrive in the wrong order, contributions change, inflation stays high, fees compound, or a simple benchmark performs better than the custom portfolio.

A strong stress test investment plan workflow compares the baseline, the stressed version and the decision that follows. If the test does not change how you think about the allocation, contribution amount, timeline or benchmark, it is probably noise rather than useful planning.

The number is less important than the path.

Most investors do not quit a plan because the final value estimate looked bad. They quit because the journey becomes harder than expected. A portfolio falls more than they imagined. A recovery takes longer. Contributions feel unrewarding. A benchmark wins while the custom strategy lags. A future-value projection can hide those moments because it compresses the experience into one ending number.

This is why a stress test investment plan process belongs inside a serious investment workflow. It slows the decision down just enough to ask better questions. What happens if the first year is negative? What happens if the worst decline arrives right after a lump sum investment? What happens if monthly contributions are reduced for a year? What happens if inflation cuts the real value of the ending balance?

Stress testing is not the same as pessimism. It is a way to make uncertainty visible. If the test shows that a plan can survive a hard path, the investor gains stronger confidence. If the test exposes a weak assumption, the investor can adjust before money is committed. Both outcomes are useful.

The WhatIfInvested system is built around that logic: Simulate, Compare, Understand. Simulate the plan to see the historical path. Compare the plan against harder conditions and benchmarks. Understand whether the strategy still fits the investor’s behavior, timeline and risk tolerance.

Investor.gov describes investment risk as the possibility of losing some or all of the money invested, and explains that different investments carry different types of risk. Their educational overview is a useful external reference for readers who want a broader foundation: Investor.gov on risk.

Run these tests before trusting the plan.

A good stress test is specific. It does not ask a vague question like “what if things go badly?” It names the condition, changes one input and compares the result. That makes the insight usable.

Start before a crash

Build the baseline, then test a period that includes a major downturn. Review the maximum drawdown, recovery time and whether the investor could realistically keep contributing.

Lower contributions

Reduce the contribution amount for part of the plan. This shows whether the goal depends on a perfect savings schedule or whether it can survive normal life interruptions.

Benchmark the portfolio

Compare the custom allocation with a simple benchmark. If the plan adds complexity but does not improve the result or reduce risk, the extra work needs a clear reason.

Test inflation and real return

A portfolio can grow in nominal dollars while still losing purchasing power. A stress test investment plan review should look at real return when the decision depends on lifestyle, retirement income or long-term buying power. This connects naturally to inflation adjusted investment growth.

Test fee drag

Fees rarely feel dramatic in one year, but they compound quietly. Test higher fees or advisory costs to see how much value disappears over time. If two portfolios have similar returns but one has lower fee drag, the simpler option may be more durable. The article on investment fees and compound growth supports this part of the workflow.

Test concentration risk

A concentrated portfolio can look excellent when the largest asset wins. It can also be fragile when that asset underperforms. To stress test investment plan concentration, compare the concentrated portfolio with a diversified version and a benchmark. The useful question is not whether concentration can win. It can. The useful question is whether the extra risk is intentional and visible.

Do not judge the plan by final value alone.

Final value is only one output. It tells you where the plan ended, but it does not tell you how hard the path was. A stress test investment plan decision should compare the outcome, the pain required to reach it and the reason the strategy deserves to exist.

| Signal | What it reveals | Decision to consider |

|---|---|---|

| Maximum drawdown | The largest decline from peak to low. | Lower risk, diversify, or accept the pain consciously. |

| Recovery time | How long the plan stayed below its previous high. | Extend the timeline or reduce assumptions if patience is unrealistic. |

| Benchmark gap | Whether complexity helped versus a simple reference. | Keep the strategy only if it adds return, lowers risk or fits a goal. |

| Contribution dependence | How much the ending value relies on future deposits. | Use a more realistic savings amount or link the plan to a budget. |

| Real return | How much purchasing power remains after inflation. | Adjust goals, timeline or expected spending power. |

| Fee drag | How much cost compounds against the investor. | Compare lower-cost options or justify the cost with clear value. |

A plan that ends slightly lower but requires much less drawdown may be easier to follow. A plan that beats the benchmark but takes much more risk may still be a poor fit. A plan that looks strong before inflation may be weaker in real terms. The stress test helps the user see those tradeoffs before the decision becomes expensive.

How to interpret a bad stress test without panicking.

A weak stress test result does not automatically mean the portfolio is broken. It means the plan has shown you where the pressure point is. That is useful. The worst outcome is not a bad test. The worst outcome is discovering the weakness only after real money is already exposed and the investor is making decisions under stress.

When you stress test investment plan assumptions, read the result in layers. First, look at the ending value. Then look at the maximum drawdown. Then look at recovery time. Then compare the result with a benchmark. Finally, ask whether the plan still fits the investor’s real life. This sequence is important because final value alone can make an aggressive plan look better than it feels.

If the ending value is low

A low ending value can mean several things. The contribution amount may be too small for the goal. The timeline may be too short. The expected return may be too conservative. Inflation or fees may be taking more than expected. The correct response is not always to take more risk. Sometimes the better answer is to extend the timeline, increase contributions gradually, lower the target or use a more realistic goal.

This is where the stress test investment plan workflow becomes practical. The result should lead to a decision you can actually act on. If the gap is contribution-related, test a higher monthly amount. If the gap is timeline-related, test five more years. If the gap is risk-related, compare the same plan with a more diversified allocation.

If the drawdown is too high

A deep drawdown does not always destroy the plan mathematically, but it can destroy the plan behaviorally. If the portfolio falls 35, 45 or 55 percent, the key question is whether the investor could keep following the strategy. Many investors say yes when looking at a chart. Fewer say yes when the decline is happening in real time.

If the drawdown feels unacceptable, the answer may be to reduce concentration, use a broader allocation, lower the risky asset exposure or build a larger cash buffer outside the portfolio. The goal is not to remove volatility completely. The goal is to make the plan followable.

If the benchmark wins

Benchmark underperformance is uncomfortable, but it is one of the most useful stress test signals. If a simple benchmark beats the custom portfolio with less complexity, the custom strategy needs a reason to exist. That reason could be lower drawdown, income, tax considerations, currency exposure, diversification or a goal that the benchmark does not serve.

If there is no clear reason, the benchmark result is telling you something important. Complexity is not a virtue by itself. A stress test investment plan comparison should make the investor ask whether the extra moving parts improve the decision or only make the portfolio feel more sophisticated.

If the plan depends too heavily on perfect contributions

Some plans only work if the investor contributes exactly as planned for many years. That may be fine for a stable high-income household. It may be unrealistic for someone with variable income, debt payments, major upcoming expenses or an emergency fund that is still incomplete.

When contributions are the fragile assumption, the best next test is not another market scenario. It is a budget scenario. Test the plan with a lower contribution amount. Test a one-year pause. Test a slower increase. If the plan still works under a more realistic savings schedule, confidence improves. If it fails, the goal needs to be adjusted before the investor depends on it.

Use a five-step stress test investment plan workflow.

Build the baseline

Choose the portfolio, starting amount, contribution, time period and benchmark you actually expect to use. A baseline should be realistic, not optimized to look impressive. If asset selection is unclear, begin with investment simulator assets.

Change one hard condition

Test one stress condition at a time: a crash period, lower contributions, higher inflation, fee drag, benchmark underperformance or concentration risk. If too many inputs change at once, the result becomes harder to understand.

Compare the path

Look beyond final value. Review drawdown, recovery, benchmark gap and whether the result would have been emotionally realistic. This is where the Investment Simulator is more useful than a static projection.

Save the scenario

Keep the baseline and stressed version so the decision can be reviewed later. The article on save investment scenarios explains why saved assumptions turn a one-time test into a repeatable planning process.

Write the decision

Decide what the test changed. Maybe the allocation should be diversified. Maybe the contribution amount is too aggressive. Maybe the benchmark is hard to beat. Maybe the plan is still strong, but the investor now understands the risk.

This workflow keeps stress testing useful. The purpose is not to collect scary scenarios. The purpose is to identify the assumption most likely to break the plan, then decide whether to change it.

Turn the stress test into a clear next move.

The value of a stress test is not the chart. The value is the decision it creates. After running the test, the user should be able to say one of four things: keep the plan, adjust the plan, compare another version, or move the workflow into a more complete Premium planning setup.

This matters because investment research can become endless. It is easy to run another scenario, change another assumption or search for another perfect portfolio. A stress test investment plan process should reduce uncertainty, not expand it forever. The decision rule keeps the work grounded.

Keep the plan when the downside is acceptable

If the plan survives a hard period, keeps a reasonable benchmark gap, has a drawdown the investor can tolerate and does not rely on unrealistic contributions, the right answer may be simple: keep the plan. This does not mean the future is guaranteed. It means the tested assumptions are coherent enough to move forward.

Adjust the plan when one assumption is clearly fragile

If one variable causes most of the weakness, change that variable first. A concentrated portfolio may need broader diversification. A contribution-heavy plan may need a more realistic savings amount. A high-fee plan may need a lower-cost version. A short timeline may need more years. The best adjustment is usually specific, not dramatic.

Compare another version when the tradeoff is not obvious

Sometimes two plans are close. One has a higher final value but more drawdown. Another has lower return but smoother behavior. In that situation, the correct next step is comparison, not immediate action. Use compare investment strategies to clarify whether the tradeoff is worth it.

Move to Premium when the workflow becomes repeatable

Premium becomes logical when the user wants to save multiple scenarios, compare several portfolios, review a benchmark, export a report or revisit the assumptions later. That is not a cosmetic upgrade. It is the point where the investor is no longer doing a one-time calculation. They are building a decision record.

The strongest funnel for this article is therefore natural: learn how to stress test investment plan assumptions, run the free simulator, compare the results, save the scenario conceptually, then review Premium access when the process needs to become organized.

Three examples that make the test concrete.

The investor starting before a crash

An investor wants to begin a monthly ETF plan. The normal projection looks strong over 20 years. The stress test starts the same plan before a severe downturn. The ending value may still be positive, but the path may include years of discomfort. If the investor can keep contributing through that decline, the plan may be durable. If not, the allocation or contribution amount may need to change.

The investor with an unstable contribution schedule

Another investor assumes a $900 monthly contribution, but the household budget can only support $500 with confidence. A stress test investment plan comparison should test both versions. The $900 version may look better, but the $500 version may be more honest. A plan that can actually be repeated is often more valuable than a plan that looks impressive but depends on perfect behavior.

The investor with a concentrated growth portfolio

A third investor holds a portfolio dominated by one growth asset. The past result looks impressive. The stress test compares that portfolio with a diversified allocation and a benchmark. If the concentrated version wins only during a narrow period and suffers much deeper drawdowns, the investor should understand the tradeoff before choosing it.

These examples show why stress testing belongs inside the product funnel. The user begins with a simple question, then realizes that the plan needs comparison, benchmarks, saved scenarios and a clear report. That is exactly where Premium can feel valuable without being forced.

A practical checklist before you trust the projection.

Use this checklist when an investment projection looks attractive. It keeps the stress test simple and prevents the user from overbuilding the analysis. The point is to test the main weak assumptions, not to build a complicated institutional risk model.

- Write the baseline first. Document the portfolio, contribution amount, timeline and benchmark before changing anything.

- Choose one stress condition. Test a crash, lower contribution, flat market, higher inflation, fee drag or benchmark underperformance one at a time.

- Review the drawdown. Ask whether the worst decline is something the investor could realistically tolerate.

- Check the recovery. A plan may recover eventually but still require years of patience.

- Compare with a benchmark. Use a simple reference to see whether complexity improved the result.

- Save the scenario. Keep the baseline and stressed version so the decision can be reviewed later.

- Make one decision. Keep the plan, adjust one assumption, compare another version or move to a Premium workflow.

A checklist also protects the user from overreacting. A bad stress test does not always mean the investment plan is wrong. Sometimes it means the investor needs a stronger emergency fund, a more realistic contribution schedule, a longer timeline or clearer expectations about volatility. The result should inform judgment, not replace it.

Stress testing should clarify, not confuse.

- Testing only the worst possible period. Extreme periods matter, but they are not the only risk. A useful stress test investment plan review should include crash, flat market, contribution, inflation, fee and benchmark tests.

- Changing everything at once. If the asset mix, contribution, period and benchmark all change together, the user cannot tell what caused the result.

- Ignoring behavior. A plan can be mathematically profitable and emotionally unrealistic. Drawdown matters because behavior matters.

- Forgetting inflation and fees. Nominal results can look better than real results. Fees and inflation can quietly reduce the value that actually matters.

- Skipping the benchmark. A custom portfolio may still be valid if it trails a benchmark, but the reason should be clear. Maybe it reduces risk. Maybe it fits taxes. Maybe it produces income. Without the benchmark, complexity can hide weakness.

Where this article fits in WhatIfInvested.

Start with the Investment Simulator when you want to see historical paths. Use compare investment strategies when you need to test different methods. Use portfolio benchmark SPY when you need a simple reference. Use portfolio allocation comparison when concentration or diversification is the main question.

The stress test investment plan article connects those pieces into one decision habit. A simulator without stress testing can feel like a calculator. A simulator with stress testing becomes a decision environment. That is the growth logic behind this content: teach the user the method, send them to the tool, then let Premium become relevant when the workflow becomes repeatable.

This article should not compete with the guides on fees, inflation, taxes, benchmarks or saved scenarios. It should send authority toward them and receive authority back from them. It acts as the risk-testing satellite inside the Portfolio Strategy cluster.

FAQ about stress testing an investment plan

What is an investment plan stress test?

An investment plan stress test checks how a portfolio plan behaves under difficult assumptions such as market crashes, long flat periods, lower contributions, higher inflation, fee drag or benchmark underperformance.

How do I stress test investment plan assumptions?

Start with a baseline, change one stressful condition at a time, compare final value and drawdown, then save the result so you can review it later.

Is stress testing the same as predicting a crash?

No. Stress testing does not predict the next crash. It helps you understand whether your plan is durable if a difficult market or life event happens.

Which metric matters most in a stress test?

Maximum drawdown is often the most important because it shows the pain an investor may need to tolerate. Final value, benchmark gap, recovery time and real return also matter.

Can free tools stress test an investment plan?

Free tools can handle simple stress tests. Premium becomes more useful when you need multiple portfolios, saved scenarios, benchmark comparison, exports and repeatable reporting.

Should I change my portfolio after a bad stress test?

Not automatically. A bad stress test is a signal to review the assumptions. You may need a more diversified allocation, a different contribution plan, a better emergency fund, or simply clearer expectations.

Test the hard version before the market does.

Run the baseline, test a bad market, lower the contribution, compare a benchmark and save the result. If the plan still makes sense after that, it becomes easier to trust.