Best DCA Frequency: Daily, Weekly or Monthly?

The best DCA frequency is usually the one you can automate consistently without creating extra friction. Daily, weekly and monthly investing can all work, but the right choice depends on pay schedule, fees, volatility, asset type and how much attention you want your investing plan to require.

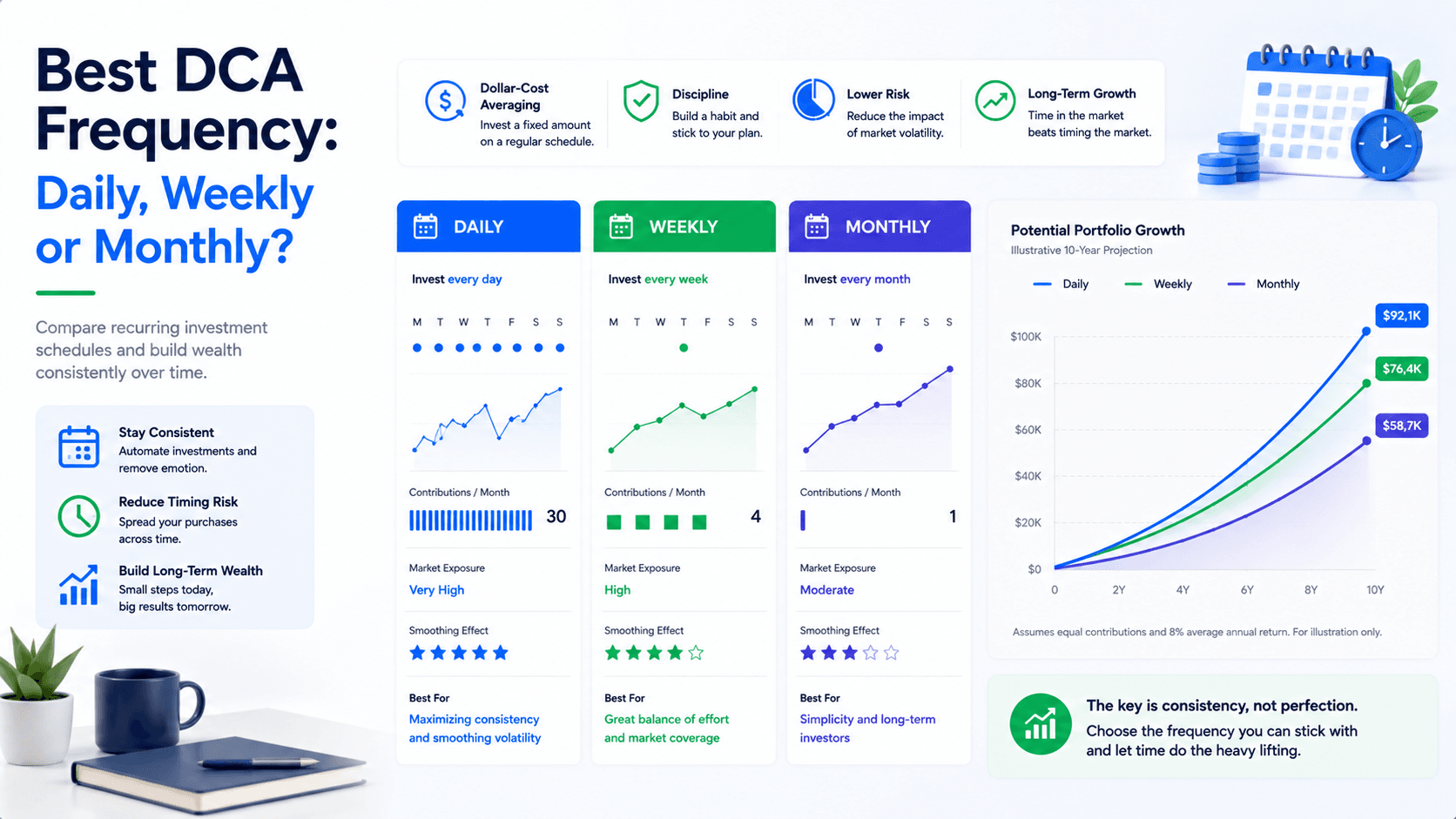

Daily, weekly and monthly DCA at a glance

The chart is not the whole decision. It is a quick visual way to compare how each schedule feels: daily gives the most entry points, weekly smooths the experience, and monthly keeps the plan simple enough for most investors to follow.

Best DCA frequency: quick answer

The best DCA frequency for most long-term investors is monthly. Monthly DCA is simple, easy to automate, aligned with bills and pay cycles, and frequent enough to build discipline. Weekly DCA can make sense if you are paid weekly or biweekly, if your broker supports free fractional investing, or if you are investing in a volatile asset and want a smoother average entry price. Daily DCA is rarely necessary for ETFs and long-term portfolios because it adds complexity without usually changing the result enough to matter.

The important word is “usually.” The best DCA frequency is not a universal math answer. It is a behavioral answer supported by math. A plan that runs every month for ten years will usually beat a theoretically perfect daily plan that you stop after three months because it feels too busy. Consistency matters more than tiny timing differences.

Start with monthly DCA if you want the cleanest long-term habit. Move to weekly or biweekly when it fits your paycheck. Use daily only when the platform is low-friction and the asset is volatile enough to justify the extra activity.

On this page

What DCA frequency really means

DCA frequency is how often you invest a fixed amount into an asset or portfolio. A daily DCA plan might invest every trading day. A weekly plan might invest every Monday or every Friday. A monthly plan might invest on payday or on the first trading day of each month. The core idea is the same: instead of trying to choose one perfect entry date, you spread purchases over time.

That spreading can reduce timing regret. If the market drops after the first contribution, the next contribution buys at a lower price. If the market rises, the earlier contribution is already working. DCA does not guarantee better returns than lump sum investing, and it does not remove market risk. Its strength is that it turns investing from a high-pressure timing decision into a repeatable habit.

Frequency matters because it changes the number of entry points, the size of each purchase, the amount of cash waiting on the side, and the complexity of the system. A person investing $600 per month could invest $600 once per month, about $150 per week, or about $20 per trading day. The total monthly commitment is similar, but the experience feels different.

For most investors, the difference between daily, weekly and monthly DCA is smaller than the difference between investing consistently and not investing at all. This is why the best dollar-cost averaging strategies usually start with automation, asset selection and realistic contribution amounts before optimizing frequency.

Daily vs weekly vs monthly DCA

The best way to compare frequencies is to look at the tradeoff between precision and simplicity. More frequent purchases give you more entry points. Fewer purchases give you a cleaner routine. Neither one is automatically superior. The right answer depends on how much the extra precision is worth to you.

| DCA frequency | Best for | Main advantage | Main drawback | Typical verdict |

|---|---|---|---|---|

| Daily DCA | Crypto, very volatile assets, small automatic purchases | Many entry points and very smooth averaging | Can feel excessive and may create recordkeeping noise | Useful in narrow cases, rarely needed for ETFs |

| Weekly DCA | Weekly or biweekly paychecks, investors who want smoother entry than monthly | Good balance between consistency and simplicity | More transactions than monthly | Strong choice when automation is free |

| Monthly DCA | Most ETF investors and long-term savers | Simple, durable and aligned with budgeting | Slightly fewer entry points | Default choice for most people |

Daily DCA can feel attractive because it sounds mathematically refined. But if you are buying a broad ETF for 20 or 30 years, daily purchases may not meaningfully improve your life. It may simply make the plan feel more complicated. Weekly DCA is often the middle ground: frequent enough to feel smooth, but not so frequent that the system becomes noisy.

Monthly DCA remains powerful because it is easy to repeat. Many investors receive income monthly or organize their finances around monthly bills. If the contribution happens automatically after payday, the plan can run with very little attention. That quiet automation is a feature, not a weakness.

Fees, spreads and friction can decide the best DCA frequency

The best DCA frequency changes when transaction costs exist. If each trade costs money, daily DCA can become inefficient very quickly. Even small commissions, spreads, currency conversion costs or platform fees can reduce the benefit of frequent purchases. A plan that looks clever before costs can become wasteful after costs.

For commission-free ETF platforms, the fee issue is smaller, but spreads and currency conversion can still matter. If you buy a U.S.-listed ETF from a Canadian account every day and pay conversion friction each time, the frequency may be working against you. If you buy a Canadian-listed ETF with free trades once per month, the plan may be cleaner and more efficient.

Crypto can be different. Some platforms support recurring daily or weekly purchases, but spreads can be wide and hidden. A daily crypto DCA plan might reduce timing regret, yet still lose efficiency if each purchase includes a high spread. The question is not only “how often should I buy?” It is “what does each buy cost?”

You can use the DCA Calculator to model contribution amounts, but you should also think about real-world trading friction. For advanced comparisons with fees and portfolio assumptions, the Premium workflow is the better path.

Match your DCA frequency to your paycheck

The strongest DCA frequency is often the one that matches cash flow. If you are paid monthly, monthly DCA is natural. If you are paid every two weeks, biweekly DCA can feel cleaner than waiting for a calendar month. If you are paid weekly, weekly DCA can keep money from sitting idle and make the plan feel connected to income.

This is not only about returns. It is about budget design. A contribution schedule that fights your cash flow creates stress. A schedule that matches cash flow can become invisible. The investor gets paid, the contribution moves automatically, and the remaining money is easier to budget.

For example, someone investing $400 per month could invest $400 on the first of each month. Another person paid every two weeks might invest $200 every payday. A weekly worker might invest $100 per week. All three plans can be reasonable if the total contribution is sustainable.

If you need to find the amount you can invest safely, start with WhatIfBudget or the guide on how much to save monthly. The best frequency cannot fix a contribution amount that is too high for your real budget.

Best DCA frequency for ETFs, stocks and crypto

The asset type changes the answer. Broad ETFs, individual stocks and crypto do not behave the same way. A broad ETF may be diversified, relatively efficient and suitable for monthly contributions. A single stock may have company-specific risk. Crypto can trade every day and move sharply, which makes frequency feel more important.

Best DCA frequency for ETFs

For ETFs, monthly DCA is usually enough. Broad funds are built for long-term exposure, not minute-by-minute optimization. If you are buying a low-cost index ETF for retirement, the biggest drivers are savings rate, time horizon, fees, allocation and staying invested. Weekly DCA can still be fine, especially if it matches your paycheck, but daily ETF DCA is usually unnecessary.

Best DCA frequency for individual stocks

For individual stocks, frequency does not solve concentration risk. Buying a stock daily or weekly can smooth the entry price, but it does not make the company safer. If the business underperforms, frequent DCA can simply add more money to a weak position. For stocks, use frequency only after you are comfortable with the business risk and position size.

Best DCA frequency for crypto

For crypto, weekly DCA is often a reasonable middle ground. Daily DCA can make sense if automation is free and spreads are acceptable, because crypto is highly volatile and trades continuously. Monthly DCA can still work, but some investors prefer weekly to reduce the emotional weight of one monthly purchase. The key is to keep the position size appropriate for the risk.

If you want to see how recurring crypto contributions can behave over time, compare this article with the Bitcoin DCA example in the crypto cluster. For most investors, though, the lesson is simple: increase frequency only when it improves behavior or reduces meaningful timing risk without adding hidden costs.

Does daily DCA produce better returns?

Daily DCA does not automatically produce better returns. It simply creates more purchase dates. If prices decline steadily, daily DCA may buy along the way down. If prices rise steadily, investing more money earlier may have been better. If the market is choppy, daily DCA can smooth the entry price. The outcome depends on the path of prices.

The danger is false precision. A daily plan can make investors feel like they have optimized something important, when the difference may be tiny compared with asset allocation, contribution amount or time horizon. If daily DCA helps you stay calm and costs nothing, it can be useful. If it makes you check the market every day, it may hurt behavior.

For long-term investors, a better question is: “Which frequency will I follow for years?” A monthly plan that runs for 15 years is more powerful than a daily plan that becomes a distraction. The best DCA frequency is the frequency that keeps the investment process boring enough to continue.

Common mistakes when choosing a DCA frequency

The first mistake is over-optimizing frequency before choosing a realistic contribution amount. Investing $100 per month consistently is usually better than designing a daily plan that your budget cannot support. Contribution size and consistency are the foundation. Frequency is a tuning decision.

The second mistake is ignoring fees. If each transaction costs money, frequent DCA can quietly reduce returns. This is especially important for small contributions. A $2 fee on a $20 daily purchase is not small. It is a major drag.

The third mistake is using frequency to avoid making a real asset allocation decision. Daily DCA into a risky asset is still risky. Weekly DCA into a concentrated stock is still concentrated. Monthly DCA into a broad ETF may be more durable than daily DCA into a speculative idea.

The fourth mistake is checking results too often. A weekly plan can become a weekly emotional event if the investor watches every purchase. The goal of DCA is to reduce timing pressure, not create more moments to react.

The fifth mistake is changing frequency every time the market moves. If the plan changes from monthly to daily after prices fall, then back to monthly after prices rise, the investor may be market timing without admitting it. Decide the rule in advance, then follow it long enough to matter.

A simple decision framework

Use this decision framework if you want a practical answer quickly. Start with monthly DCA as the default. Move to weekly or biweekly if your paycheck arrives that way, if trades are free, or if you are investing in a more volatile asset and want smoother entries. Consider daily only if automation is effortless and costs are effectively zero.

| Investor situation | Recommended frequency | Reason |

|---|---|---|

| Long-term ETF investor paid monthly | Monthly | Simple, aligned with income and easy to automate. |

| Investor paid every two weeks | Biweekly | Matches cash flow and keeps money moving steadily. |

| Crypto investor with free automated buys | Weekly or daily | Higher volatility can make more frequent entries feel smoother. |

| Small contribution with trading fees | Monthly | Reduces cost drag from frequent transactions. |

| Advanced investor comparing scenarios | Test multiple frequencies | Use tools to compare fees, timing, and portfolio assumptions. |

If you still cannot decide, choose monthly and automate it. You can revisit the frequency later, but the most important step is getting the plan running. A good DCA habit started today is usually more valuable than a perfect DCA schedule delayed for months.

DCA frequency examples by investor profile

The best DCA frequency becomes clearer when it is tied to a real investor profile. A student investing from part-time income, a salaried worker investing every payday, a crypto investor managing volatility, and a family investing for retirement do not need the same schedule. The goal is to choose a frequency that makes the plan easier to follow, not one that looks impressive on paper.

Beginner investing $50 to $100 per month

For a beginner investing a small amount, monthly DCA is usually the cleanest choice. The contribution is easy to remember, easy to automate, and less likely to be eaten by trading friction. If a platform allows free fractional investing, weekly DCA can still work, but the improvement may be mostly emotional. The beginner’s main job is to build the habit, learn the tool, and avoid stopping after normal volatility.

At this stage, contribution amount matters more than frequency. A beginner who invests $75 every month for years is building a stronger foundation than someone who tries to invest a tiny amount daily, forgets to automate it, and abandons the plan. The most useful next step is to open the DCA Calculator, test a monthly amount, and ask whether that amount can survive rent, debt payments, emergency savings, and normal life costs.

Paycheck investor contributing $200 to $800 per month

For a paycheck investor, the best DCA frequency is often the paycheck frequency. If income arrives every two weeks, biweekly investing is natural. If income arrives monthly, monthly investing is natural. This keeps investing connected to cash flow and reduces the chance that money needed for bills is accidentally invested too early.

This investor may benefit from a two-layer system: a fixed contribution every paycheck, plus an occasional extra contribution when cash flow is stronger than expected. That extra contribution should still follow rules. For example, the investor might add surplus cash only after the emergency fund target is met and no high-interest debt is due. That keeps DCA from becoming impulsive “buy the dip” behavior.

ETF investor building a long-term portfolio

For a broad ETF investor, monthly DCA is usually enough. ETFs are often used for long-term exposure, and the difference between buying once per month and four times per month is usually less important than allocation, fees, tax location, and staying invested through downturns. Weekly DCA is acceptable if it fits the investor’s routine, but daily ETF DCA is rarely worth the extra attention.

The ETF investor should pay attention to reinvestment, asset allocation, and whether contributions are going into one ETF or a portfolio. If the portfolio includes multiple funds, the contribution schedule can also become a rebalancing tool. New money can go toward the underweight asset instead of automatically buying everything in the same proportion. That is where a more advanced Premium workflow can be useful.

Crypto investor managing volatility

Crypto investors may reasonably choose weekly or even daily DCA because the asset can move sharply and trades continuously. A daily plan can reduce the emotional weight of one large purchase, especially for someone who is nervous about volatility. But crypto frequency should never be used to justify a position size that is too large. Buying a risky asset more often does not make the asset low risk.

The crypto investor must check spreads, platform fees, and custody risk. If a daily recurring buy has a wide spread, the plan may be more expensive than it looks. Weekly DCA is often a better compromise: frequent enough to smooth entry points, but less noisy than daily execution. Monthly can still work if the investor wants simplicity and is comfortable with larger individual purchases.

Advanced investor comparing multiple portfolios

An advanced investor should not decide frequency in isolation. Frequency interacts with portfolio weights, cash drag, fees, rebalancing rules, taxes, and withdrawals. For example, a weekly DCA plan across four assets may create different allocation drift than a monthly plan that rebalances contributions toward underweight assets. A portfolio with recurring withdrawals may need a different schedule than a portfolio that only receives deposits.

This is where the Premium workflow becomes more relevant. If the decision affects a large portfolio, a retirement plan, or a serious long-term strategy, the investor should compare multiple scenarios instead of guessing. The best DCA frequency may be the one that produces the most durable plan after fees, behavior, and portfolio management are included.

Trusted external perspective

External investor education sources generally frame dollar-cost averaging as a discipline and timing-risk tool rather than a guaranteed return booster. FINRA’s investor education material on dollar-cost averaging makes the same practical point: regular investing can reduce the pressure of choosing the perfect time, but investors still need to understand risk, fees and their time horizon.

That framing matches the WhatIfInvested approach. DCA frequency should help you follow a plan. It should not become a distraction that makes investing feel more complicated than it needs to be.

Related guides and tools

Frequently asked questions

What is the best DCA frequency?

The best DCA frequency for most long-term investors is monthly because it is simple, easy to automate and aligned with normal budgeting. Weekly or biweekly can also work well if it matches your paycheck.

Is daily DCA better than weekly DCA?

Daily DCA creates more entry points, but it is not automatically better. It can help with volatile assets if fees are zero, but for most ETF investors weekly or monthly DCA is simpler and usually sufficient.

Is weekly DCA better than monthly DCA?

Weekly DCA may feel smoother and can fit weekly or biweekly paychecks. Monthly DCA is usually easier to manage and often produces a similar long-term result for broad ETF investors.

Should I DCA every paycheck?

DCA every paycheck can be a strong approach because it matches investing with income. It works best when the contribution amount is sustainable and the trades are free or very low cost.

Does DCA frequency matter for ETFs?

DCA frequency matters less for broad long-term ETFs than contribution amount, fees, allocation and time horizon. Monthly DCA is usually enough for ETF investors.

Does DCA frequency matter for crypto?

It can matter more for crypto because crypto is highly volatile and trades continuously. Weekly or daily DCA can smooth entries, but spreads and platform costs must be checked.

Can I change my DCA frequency later?

Yes. You can start monthly and switch to weekly or biweekly later if it better matches your income or behavior. Avoid changing frequency only because of short-term market moves.

What tool should I use to compare DCA frequencies?

Use the WhatIfInvested DCA Calculator for simple contribution planning. Use Premium when you need to compare multiple scenarios, fees, portfolios, saved assumptions and exportable reports.