Portfolio Benchmark SPY: Benchmarking Your Portfolio Against SPY

A portfolio benchmark SPY comparison helps you answer a simple but uncomfortable question: is your portfolio actually improving the outcome, or would a plain S&P 500 benchmark have done the job with less complexity?

Quick answer

A portfolio benchmark SPY comparison uses SPY, the SPDR S&P 500 ETF Trust, as a practical stand-in for broad U.S. large-cap market exposure. The goal is not to prove that every portfolio must beat SPY every year. The goal is to understand whether your extra complexity, asset selection, fees, concentration, rebalancing, or timing decisions improved the result enough to justify the tradeoff.

If your portfolio had a higher final value but took much deeper drawdowns, the benchmark result is mixed. If it beat SPY after fees with similar or lower drawdown, the strategy may have added value. If it underperformed SPY while requiring more work, more risk, and more moving parts, the portfolio benchmark SPY result is warning you that the strategy may not be earning its complexity.

The best way to use a portfolio benchmark SPY workflow is to compare final value, ROI, max drawdown, best and worst years, fees, diversification, and behavior. A simple benchmark is not a complete investment plan, but it gives every portfolio a reality check before the story becomes too flattering.

What a portfolio benchmark SPY comparison really means

A benchmark is a reference point. It is the line in the sand that tells you whether a portfolio is doing something useful, something risky, or something unnecessarily complicated. When investors use SPY as a benchmark, they are usually asking whether their portfolio is doing better or worse than a broad, low-cost, widely followed U.S. stock market proxy.

That is a useful question because many portfolios sound intelligent before they are measured. A portfolio might include dividend stocks, technology stocks, international ETFs, bonds, crypto, sector funds, or individual companies. Each position can have a story. But a story is not a result. A portfolio benchmark SPY analysis turns the story into a comparison: what happened to the money, how much risk was taken, and whether the extra decisions improved the outcome.

SPY is not magic. It is an ETF designed to track the S&P 500 Index, which represents large U.S. companies. State Street publishes details for the SPDR S&P 500 ETF Trust, including fund objective, holdings, costs, and performance information. That makes SPY a practical benchmark because it is transparent, liquid, familiar, and backed by long historical data in most simulation tools.

Still, the benchmark is only useful when the comparison is fair. If your portfolio is 100 percent U.S. large-cap stocks, SPY may be a very relevant benchmark. If your portfolio includes global stocks, bonds, cash, commodities, or crypto, SPY may still be useful, but it may not be the only benchmark. The question becomes: are you comparing a portfolio to SPY because SPY matches the portfolio, or because SPY is simply the most familiar reference?

A good benchmark does not make the decision for you. It clarifies the decision. If the portfolio beats SPY, you still need to ask how and why. If it trails SPY, you need to ask whether the portfolio had a different purpose, lower risk, better income, better global exposure, or more emotional comfort. The benchmark tells you where to investigate, not what to blindly buy.

Why SPY is useful as a benchmark

SPY is useful because it gives investors a simple, recognizable baseline. Many people invest in portfolios that are more complicated than a single S&P 500 fund. They may own several ETFs, a few stocks, a small crypto allocation, and a cash position. Without a benchmark, it is easy to believe that complexity equals sophistication. A portfolio benchmark SPY comparison challenges that assumption.

The first advantage is simplicity. SPY represents broad exposure to large U.S. companies. It is not the full global market, but it captures a large and economically important part of the public equity market. If a portfolio with more moving parts cannot beat, match, or justify itself against that simple reference, the investor has learned something valuable.

The second advantage is behavior. A benchmark helps separate strategy quality from investor emotion. Suppose a portfolio underperforms SPY because the investor sold during a drawdown, chased a hot sector, or held too much cash after a market decline. The issue may not be the portfolio design. It may be the behavior around the portfolio. This is why the article on how much better SPY is than the average investor matters: benchmark returns and investor returns are not always the same thing.

The third advantage is cost awareness. A portfolio can underperform because of fees, trading costs, management fees, or tax drag. SPY is not free, but it is a low-cost, transparent reference. If a complex portfolio trails SPY by a small amount while charging much higher fees or requiring more management, the benchmark exposes the cost of complexity.

The final advantage is communication. If you are explaining a portfolio to yourself, a spouse, a client, or a future version of yourself, SPY gives you a plain-language reference. You can say: this portfolio returned less than SPY but had lower drawdown. Or: this portfolio beat SPY but required more volatility. Or: this portfolio did not justify its extra holdings. That clarity is exactly what a portfolio benchmark SPY process is supposed to create.

When SPY is the wrong benchmark

SPY is popular, but it is not always the right benchmark. A benchmark should match the question. If your portfolio is built for global diversification, comparing it only to SPY may overstate or understate quality depending on the period. U.S. stocks can lead global markets for long stretches, but that does not mean a global portfolio is broken. It may simply have a different objective.

If your portfolio includes bonds, SPY may be too aggressive as the only comparison. A balanced portfolio is usually designed to reduce volatility and drawdown, not to beat an all-equity benchmark in every bull market. If a 60/40 portfolio trails SPY during a strong equity decade, that may be normal. The better question is whether the balanced portfolio provided a smoother path, lower worst-year loss, or better fit for the investor's risk tolerance.

If your portfolio includes crypto, SPY may be too conservative for the growth sleeve and too narrow for the risk profile. Crypto can create very different return paths, drawdowns, and recovery periods. A portfolio benchmark SPY view may still be useful, but it should be paired with asset-level analysis. This is where the guide on investment simulator assets helps users choose which assets to test and how to interpret each asset's role.

If your goal is income, SPY may also be incomplete. A covered-call ETF, dividend portfolio, bond ladder, or retirement income strategy may prioritize cash flow. Comparing only final value can miss the reason the strategy exists. That does not mean income portfolios get a free pass. It means the benchmark should include total return, drawdown, income, taxes, and the investor's actual spending goal.

| Portfolio type | SPY as benchmark? | What to add |

|---|---|---|

| U.S. large-cap equity portfolio | Strong fit | Compare costs, drawdown, sector concentration and tracking difference. |

| Global equity portfolio | Useful but incomplete | Add global equity benchmark or all-in-one ETF comparison. |

| Balanced stock/bond portfolio | Too aggressive alone | Compare risk-adjusted return and max drawdown. |

| Crypto or alternative portfolio | Reference only | Add asset-level volatility, recovery, and concentration analysis. |

| Income portfolio | Incomplete alone | Add cash flow, taxes, total return and withdrawal needs. |

The key is intellectual honesty. Do not pick a benchmark that makes the portfolio look good. Pick a benchmark that exposes the decision. If SPY is a fair reference, use it directly. If it is only a partial reference, say so and add another comparison.

The metrics that matter beyond final value

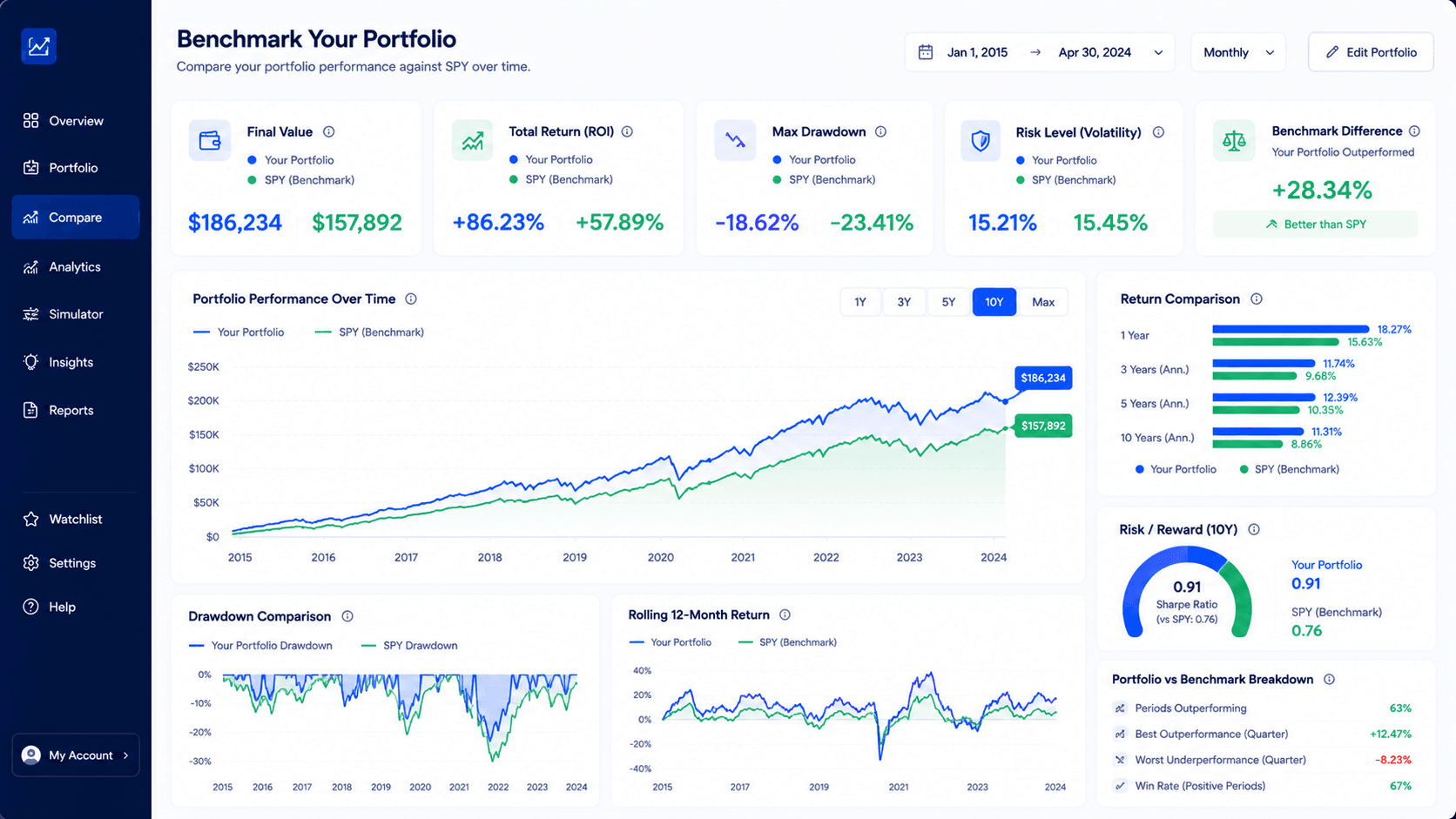

Final value is the number most people look at first. It is also the number most likely to mislead. A portfolio can finish with more money than SPY but require a much deeper drawdown, a worse worst year, more concentration, higher fees, and more emotional pressure. Another portfolio can trail SPY slightly but provide a smoother path and better fit for the investor. The benchmark decision lives in the details.

A good portfolio benchmark SPY workflow reads these metrics together. If a portfolio beats SPY by 2 percent but had twice the drawdown, the result may not be as strong as it looks. If it trails SPY by 1 percent but reduces drawdown dramatically, the result may be acceptable for a risk-conscious investor. If it trails SPY while taking more risk, charging more fees, and adding more complexity, the benchmark is pointing to a real problem.

This is why Premium workflows are valuable. A free backtest can answer the first question. But a serious benchmark review often needs multiple portfolios, weighted allocations, fees, DCA vs lump sum, saved scenarios, and exportable reports. The value is not just more numbers. The value is having the right numbers next to each other.

How to benchmark your portfolio against SPY

The workflow should be structured enough to avoid a biased conclusion. Start by defining the portfolio you actually want to test. List each asset, weight, contribution behavior, timeline, and fee assumption. Then choose SPY as the benchmark only if it is relevant to the decision. If the portfolio is mixed or global, keep SPY as a reference while acknowledging its limits.

1. Define the portfolio exactly

A portfolio benchmark SPY comparison is only as good as the inputs. If your portfolio is 40 percent VOO, 20 percent QQQ, 20 percent international equity, 10 percent bonds, and 10 percent Bitcoin, write that down before running the comparison. Do not change the weights after seeing the result. The point is to test the strategy, not to optimize the past until it looks impressive.

2. Match the time period

Benchmarks must use the same start and end dates as the portfolio. If one asset has shorter history, note the limitation. A portfolio that includes a newer ETF may not have the same data window as SPY. In that case, the simulation should use the common available period or explain why the comparison is limited.

3. Compare both lump sum and DCA when relevant

If the investor is contributing monthly, a lump sum benchmark may not answer the real question. A recurring investor needs to know how contributions would have behaved over time. This is where the DCA Calculator and the Investment Simulator support different parts of the decision. DCA answers contribution rhythm. Simulation answers historical path.

4. Read the risk before celebrating the return

If the portfolio beats SPY, check how much pain it required. Was the worst drawdown deeper? Was the worst year harder to tolerate? Did one asset create most of the result? Was the result driven by a short period that may not repeat? A benchmark is not just a scoreboard. It is a stress test for the story behind the portfolio.

5. Decide what action the benchmark supports

The benchmark should lead to a decision. Maybe the portfolio is worth keeping. Maybe it should be simplified. Maybe the investor should reduce fees, diversify, rebalance, change the contribution plan, or compare a second benchmark. A benchmark without a decision is only trivia.

Practical rule: if your portfolio does not beat SPY, does not reduce risk, does not improve fit, and does not help you stay invested, the benchmark is telling you to simplify.

For a broader allocation process, use how to compare portfolio allocations. That guide helps you decide whether the portfolio mix itself makes sense before SPY becomes the final benchmark.

Example: portfolio vs SPY interpretation

Imagine two investors test a 10-year period. Investor A owns a simple SPY benchmark. Investor B owns a portfolio with SPY, QQQ, a dividend ETF, a bond fund, and a small crypto allocation. The custom portfolio finishes with a higher final value. At first glance, Investor B wins. But the deeper view matters.

If the custom portfolio had a much higher max drawdown, the investor had to tolerate more pain. If the crypto allocation drove most of the outperformance, the portfolio may have been more concentrated than it looked. If fees were higher, some of the return advantage may disappear in a longer period. If the investor would have sold during the worst year, the simulated outperformance may not be behaviorally realistic.

| Metric | SPY benchmark | Custom portfolio | Interpretation |

|---|---|---|---|

| Final value | Lower | Higher | Custom portfolio won the headline result. |

| Max drawdown | Moderate | Much deeper | Outperformance came with more emotional pressure. |

| Worst year | Manageable | Severe | Investor behavior becomes a key risk. |

| Fees | Low | Higher | Fee drag should be tested over longer periods. |

| Diversification | Broad U.S. stocks | Multiple assets but concentrated drivers | More holdings did not automatically mean better diversification. |

The conclusion is not automatically that the custom portfolio is bad. It may be acceptable if the investor wanted higher growth and could tolerate the volatility. But the portfolio benchmark SPY comparison changes the conversation. The question becomes: was the extra return worth the extra risk, complexity, and tracking effort?

This is the reason benchmark articles belong inside a product-led SEO system. They do not only educate. They move the user toward the tool. Reading about benchmarks is useful, but running the comparison with actual assets is more useful. The article should naturally lead to a simulation.

How to turn the benchmark result into a decision

The most useful part of a portfolio benchmark SPY review is not the score itself. It is the decision that follows. After you compare the portfolio with SPY, write down what the result is telling you. If the portfolio won on final value, identify whether that win came from broad diversification, one concentrated asset, a lucky start date, higher risk, or a repeatable process. If the portfolio lost, identify whether the loss was acceptable because the portfolio had a different job.

A portfolio benchmark SPY workflow should end with one of four decisions. The first decision is to keep the portfolio as designed because it delivered a better or more suitable result than SPY. The second decision is to simplify because SPY delivered a similar or better result with fewer moving parts. The third decision is to adjust risk because the portfolio outperformed but required a drawdown the investor may not tolerate. The fourth decision is to run another benchmark because SPY was useful but not sufficient for the portfolio's objective.

This step matters because investors often stop at the result. They see that a portfolio beat SPY and assume the strategy is superior. Or they see that it trailed SPY and assume the strategy failed. Both reactions can be too shallow. A portfolio benchmark SPY comparison should answer the deeper question: what should change because of this evidence?

For example, if a three-ETF portfolio beat SPY by a small margin but required a much deeper drawdown, the next action may be to reduce concentration or add a risk-control rule. If a global portfolio trailed SPY but delivered lower volatility and better international exposure, the next action may be to compare it with a global benchmark instead of forcing it to behave like a U.S. large-cap index. If a sector-heavy portfolio crushed SPY during one decade, the next action may be to stress test the result across different market periods.

The strongest benchmark decision is usually written as a sentence: “This portfolio is worth keeping because...” or “This portfolio should be simplified because...” That sentence forces the investor to connect the data to an action. Without that step, benchmark analysis becomes entertainment. With that step, a portfolio benchmark SPY review becomes part of a real planning process, and the portfolio benchmark SPY result becomes easier to explain later.

Common mistakes when comparing against SPY

Mistake 1: using SPY for every portfolio

SPY is useful, but it is not universal. A global, balanced, income-focused, or crypto-heavy portfolio may need additional benchmarks. Use SPY as a reference, not as the only possible truth.

Mistake 2: ignoring drawdown

Beating SPY with a much deeper drawdown may not be a better result for a real investor. The ability to stay invested matters. A strategy that looks good in a spreadsheet can fail if the investor abandons it during the worst period.

Mistake 3: changing the portfolio after seeing the result

Backtests are easy to overfit. If you keep changing weights until the portfolio beats SPY, you are not benchmarking a strategy. You are designing a story around the past. A useful benchmark tests a plan that could have been followed in real time.

Mistake 4: forgetting fees and taxes

Fees and taxes can reduce the advantage of a more complex portfolio. Compare gross returns only as a first pass. Then review fee drag, tax drag, and rebalancing friction when the decision becomes serious.

Mistake 5: confusing benchmark underperformance with failure

A portfolio can trail SPY and still be appropriate if it had a different goal. Lower volatility, global diversification, income stability, or better investor behavior can justify a different result. The mistake is not underperforming SPY. The mistake is not knowing why.

Related ETF comparisons can help sharpen the benchmark. If the question is S&P 500 ETF choice, read SPY vs VOO. If the question is S&P 500 versus Nasdaq-heavy growth, read SPY vs QQQ. Those articles compare assets. This article compares your portfolio against the benchmark role SPY can play.

FAQ

Is SPY a good benchmark for my portfolio?

SPY can be a good benchmark if your portfolio is mostly U.S. large-cap equity exposure or if you want a simple market reference. It is less complete for global, balanced, income-focused, or alternative portfolios.

Should I compare my portfolio to SPY or VOO?

SPY and VOO both track the S&P 500, so either can work as an S&P 500 benchmark. SPY is often used because of its long history and liquidity, while VOO is often discussed because of its low cost.

What if my portfolio has international stocks?

Use SPY as a U.S. market reference, but do not make it the only benchmark. A global portfolio may need a global equity benchmark or an all-in-one ETF comparison to make the evaluation fair.

Is beating SPY enough to prove a strategy is better?

No. A portfolio can beat SPY while taking much more risk, charging higher fees, or relying on a concentrated bet. Compare final value, ROI, drawdown, fees, diversification, and investor behavior before deciding.

Can I benchmark a DCA portfolio against SPY?

Yes. A DCA portfolio can be compared against a SPY DCA path using the same contribution amount, dates, and frequency. That is often more realistic than comparing a recurring contribution plan against a lump sum benchmark.

What tool should I use to compare my portfolio against SPY?

Start with the free Investment Simulator for a simple portfolio benchmark SPY comparison. Use Premium planning when you need multiple weighted portfolios, fees, benchmark overlays, saved scenarios, and exportable reports.

Bottom line

A portfolio benchmark SPY comparison is a reality check. It asks whether your portfolio improved the outcome compared with a simple S&P 500 reference, and whether any improvement was worth the added risk, fees, complexity, and behavior burden. The goal is not to worship SPY. The goal is to measure your strategy against a clear baseline.

If your portfolio beats SPY with acceptable risk, the benchmark supports the strategy. If it trails SPY but provides lower drawdown or better fit, the portfolio may still make sense. If it trails SPY while adding complexity and risk, the benchmark is telling you to simplify or rethink the plan.