Bitcoin vs Gold: ROI, Volatility, Inflation Protection and Portfolio Role

Bitcoin and gold are often compared as stores of value, but they behave very differently. Gold is the older defensive asset. Bitcoin is the newer digital scarcity asset. The right choice depends on return goals, drawdown tolerance, custody comfort and how each asset fits inside the rest of your portfolio.

Bitcoin vs gold is not one winner. It is two different jobs.

Bitcoin vs gold is most useful when you separate upside, stability, inflation protection, custody, and portfolio behavior. Bitcoin has historically delivered much higher potential ROI, but with extreme volatility. Gold has historically delivered lower return potential, but with a longer defensive record and a smoother emotional path.

The practical answer is conditional. Bitcoin may fit as a small asymmetric sleeve. Gold may fit as a stabilizing hedge. A blend may fit investors who want exposure to both digital scarcity and traditional monetary insurance without depending entirely on either one.

What makes Bitcoin and gold worth comparing?

A store of value is an asset people trust to preserve purchasing power over time. That trust can come from physical scarcity, monetary history, network security, liquidity, social acceptance, or a combination of those qualities. Gold and Bitcoin both compete for this role, but they earn that trust in very different ways.

Gold is scarce because it is physically hard to mine and refine. It has been recognized across cultures for centuries, and it does not depend on a software network, password, exchange account, or internet connection to exist. That gives gold a deep psychological advantage as a traditional hard asset.

Bitcoin is scarce because its issuance schedule is transparent and enforced by a decentralized network. The original Bitcoin whitepaper described a peer-to-peer electronic cash system, and the market later built a broader digital scarcity narrative around it. That is why Bitcoin is often called digital gold, even though its market behavior can look much more like a high-volatility technology adoption cycle.

| Store-of-value trait | Gold | Bitcoin | Investor implication |

|---|---|---|---|

| Scarcity | Slow physical supply growth | Programmatic issuance and capped supply | Both are scarce, but the source of scarcity is different. |

| Track record | Very long history as money, jewelry, reserve asset, and hedge | Shorter record with rapid institutional adoption | Gold has trust history; Bitcoin has adoption momentum. |

| Portability | Expensive and slow to move at scale | Can move globally through digital rails | Bitcoin has a portability advantage when custody is handled well. |

| Volatility | Lower than crypto, but not risk-free | Historically very high | Bitcoin requires stronger position sizing discipline. |

| Market structure | Deep global market with physical and ETF access | 24/7 digital market with spot, custody, and ETF access in some countries | Both are liquid, but trading behavior and risks differ. |

For neutral background, you can review the Bitcoin whitepaper, World Gold Council gold data, and Investor.gov's explanation of asset allocation. Those references support the same core idea: a store-of-value decision is not just about past return. It is also about risk, liquidity, trust, and how the asset behaves in a portfolio.

Bitcoin vs gold returns: ROI alone does not tell the full story

From a pure historical return perspective, Bitcoin has produced much stronger upside over many windows. That is the reason the bitcoin vs gold debate became so intense. A small Bitcoin allocation made before a major adoption cycle could have done more for portfolio growth than a much larger gold allocation.

But ROI can mislead if it ignores the path. Bitcoin's return profile has included repeated crashes, long underwater periods, regulatory shocks, exchange failures, and sentiment cycles that can pressure investors into selling at the wrong time. Gold's returns have usually been lower, but the asset is often easier to hold because its volatility is usually less extreme.

- Higher historical upside during adoption cycles.

- Extreme drawdowns during crypto bear markets.

- High sensitivity to liquidity, regulation, and investor sentiment.

- Best suited to investors who can hold through severe volatility.

- Lower long-term growth potential than Bitcoin.

- Longer record as a defensive monetary asset.

- Often attracts demand when financial confidence weakens.

- Best suited to investors seeking ballast rather than explosive upside.

The question is not only which asset would have made more money in hindsight. The better question is which asset produced returns an investor could realistically capture. A return stream that looks incredible on a chart is less useful if most investors abandon it during a 60%, 70%, or 80% drawdown.

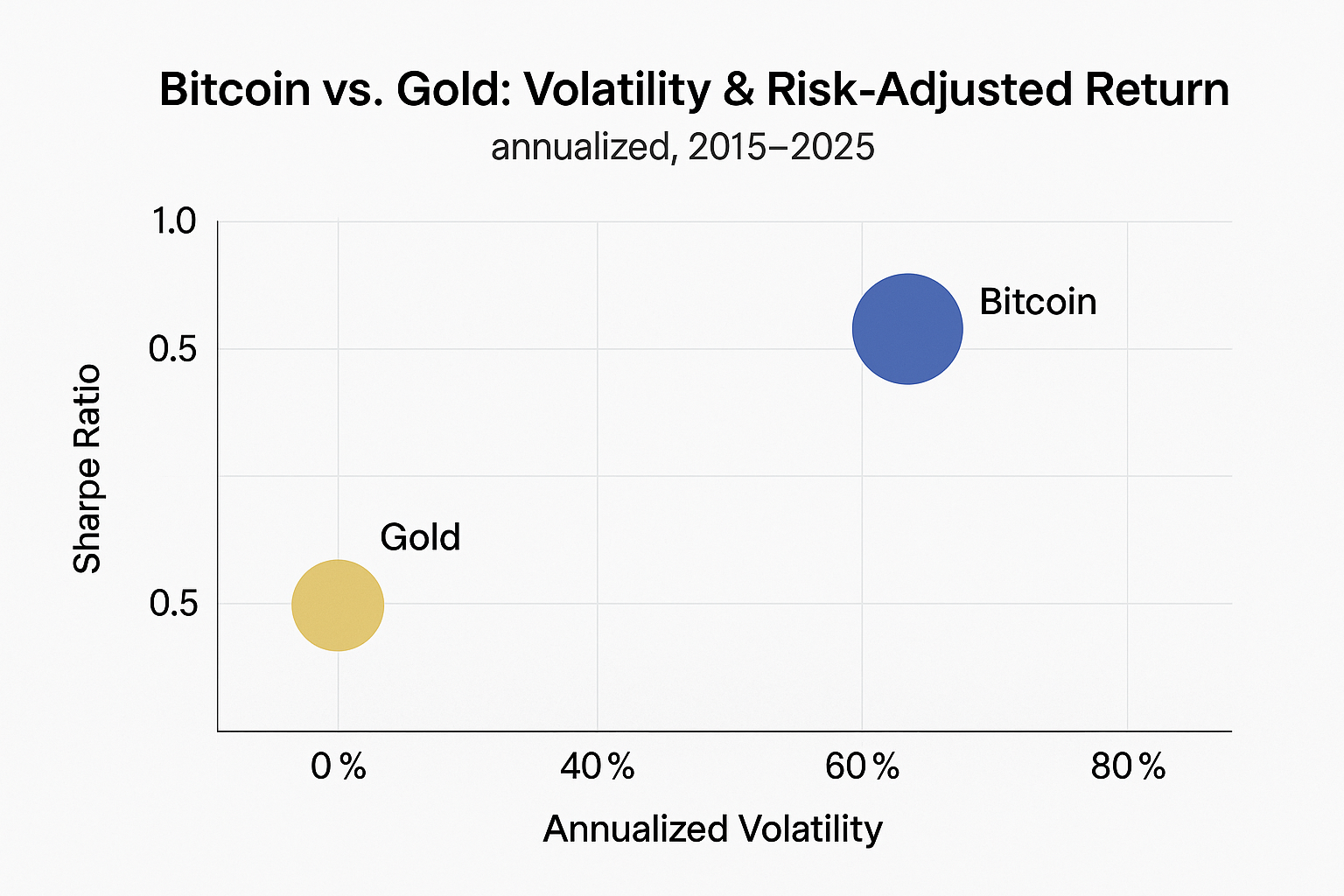

Volatility is where Bitcoin and gold separate sharply

Risk is not just the probability of a permanent loss. For real investors, risk is also the chance that volatility forces a bad decision. Bitcoin's largest historical drawdowns have been severe enough to test experienced investors. Gold can decline too, but its drawdowns have usually been less violent than crypto bear markets.

This difference changes how each asset should be sized. Bitcoin can be useful at a small allocation and destructive at an allocation that overwhelms the rest of the plan. Gold can be useful as a stabilizer, but too much gold can create opportunity cost if productive assets compound faster over long periods.

| Risk dimension | Bitcoin | Gold | Planning response |

|---|---|---|---|

| Daily volatility | High | Moderate | Keep Bitcoin small enough to hold through stress. |

| Bear market depth | Can be extreme | Usually milder | Use rebalancing bands and avoid all-in exposure. |

| Regulatory risk | Evolving | Mature | Prefer clear, compliant access routes. |

| Custody risk | Private keys, exchange risk, phishing | Storage, insurance, product structure | Choose custody before choosing position size. |

| Behavioral risk | Very high | Lower, but still present | Use predefined rules, not price emotions. |

Gold is a traditional hedge. Bitcoin is a younger scarcity bet.

Gold is often called an inflation hedge, but it is more accurate to say that gold is a monetary-confidence hedge. It tends to attract interest when investors worry about currency debasement, real interest rates, geopolitical risk, or financial instability. Gold does not rise every time inflation rises, but it has a long history of being treated as protection when confidence weakens.

Bitcoin has a different macro profile. Its fixed supply supports the digital scarcity thesis, but Bitcoin has also traded like a high-beta risk asset during some liquidity contractions. When markets sell speculative assets, Bitcoin can fall with them. That does not necessarily invalidate the long-term thesis, but it means Bitcoin should not be treated as a simple one-for-one gold replacement.

Investors seek a traditional hedge against currency risk, policy uncertainty, or financial stress.

Liquidity improves, adoption expands, and investors reward scarce digital assets.

Expenses are near-term. Neither Bitcoin nor gold should replace an emergency fund.

For diversified investors, this distinction matters. Gold may act as a stabilizer. Bitcoin may act as a high-conviction optionality sleeve. They can live in the same portfolio, but they should not be assigned the same job.

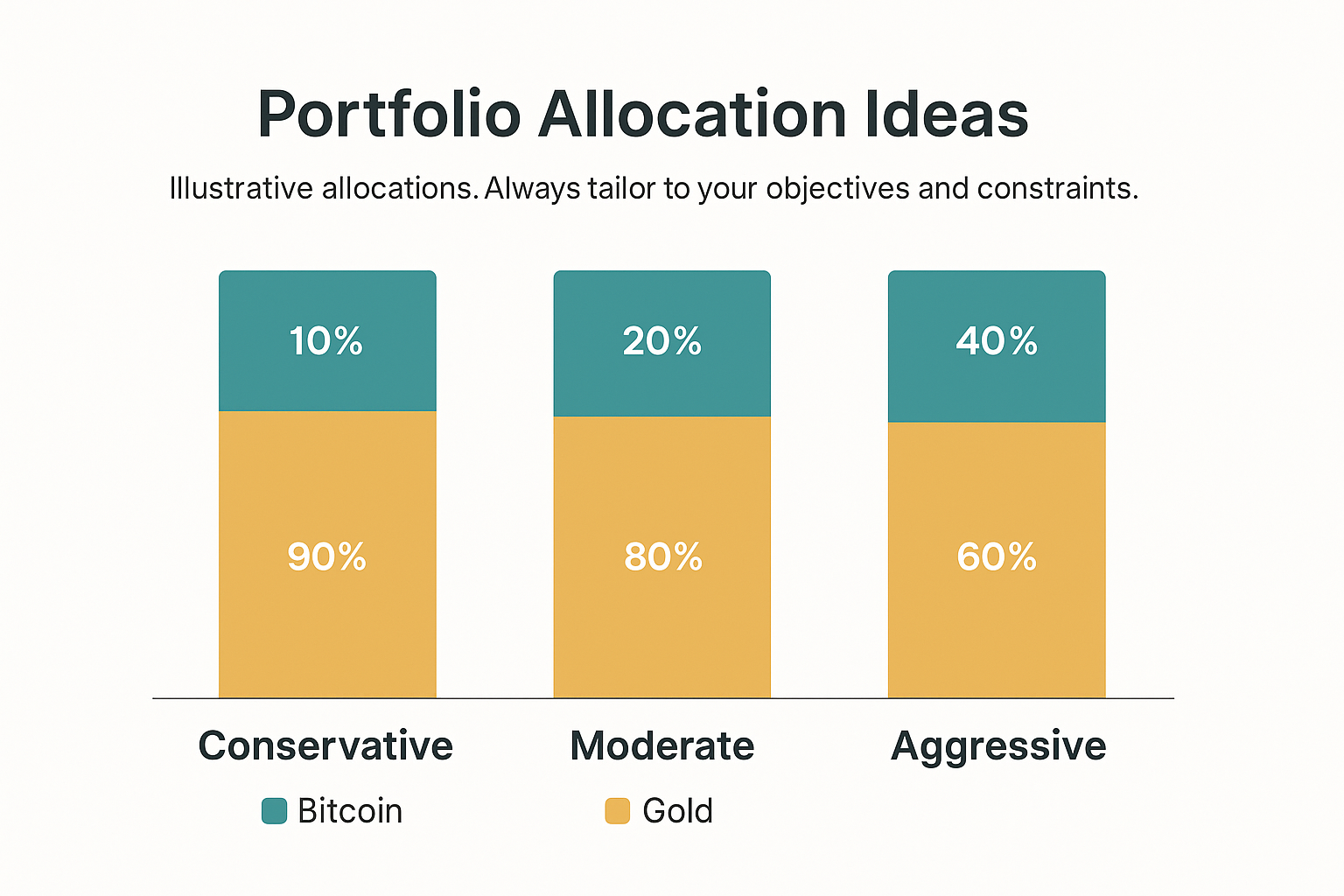

How much Bitcoin or gold makes sense?

The strongest practical insight from a bitcoin vs gold comparison is that allocation size matters more than labels. A 2% Bitcoin position is not the same decision as a 25% Bitcoin position. A 5% gold position is not the same as replacing your equity portfolio with gold. The asset can be useful at one weight and harmful at another.

For many investors, gold works best as a stabilizing sleeve. Bitcoin works best as a smaller asymmetric sleeve. The exact mix depends on age, risk tolerance, income stability, investment horizon, and whether the rest of the portfolio is already aggressive.

| Investor profile | Possible gold allocation | Possible Bitcoin allocation | Why |

|---|---|---|---|

| Conservative | 5% to 10% | 0% to 2% | Defense matters more than upside. |

| Balanced | 3% to 8% | 1% to 5% | Gold stabilizes while Bitcoin adds optionality. |

| Aggressive | 0% to 5% | 5% to 10% | Higher growth target with higher volatility tolerance. |

| Speculative | Optional | 10%+ | Only suitable if drawdowns will not derail the plan. |

Bitcoin can grow from a small allocation to a large portfolio weight quickly during bull markets. Rebalancing prevents a successful position from quietly becoming your entire risk profile. Gold can also drift, but usually less dramatically. A simple annual or threshold-based rebalancing rule can keep the portfolio aligned with the original plan.

To model your own mix, use the Investment Simulator. If you plan to build exposure gradually, compare recurring contributions with the DCA Calculator. For broader allocation context, use the guide on how to compare portfolio allocations.

Custody, access, fees, and taxes can change the real result

The investment thesis is only one part of the decision. Execution matters. Gold can be held through physical bullion, gold ETFs, mining equities, or allocated storage products. Bitcoin can be held through exchanges, hardware wallets, Bitcoin ETFs, or other regulated products depending on your country. Each route has different fees, risks, and tax treatment.

- Physical coins or bars.

- Gold ETFs.

- Allocated storage products.

- Mining stocks, which add business and equity risk.

- Self-custody hardware wallet.

- Centralized exchange.

- Spot Bitcoin ETF where available.

- Crypto broker or app platform.

For beginners, the easiest product is not always the cheapest, and the cheapest product is not always the safest. A Bitcoin hardware wallet can reduce exchange risk but introduces key-management risk. A gold ETF can simplify buying and selling but does not feel the same as owning physical metal. The best structure is the one you can understand and maintain correctly.

Taxes also matter. Selling either asset may create taxable gains depending on your jurisdiction and account type. Frequent trading can turn a good investment thesis into a poor after-tax result. If your goal is long-term wealth building, keep turnover low and document your cost basis carefully.

When Bitcoin can lead, and when gold can lead

A stronger comparison looks at different market environments instead of assuming one permanent winner. Bitcoin and gold respond to different investor fears and incentives. Bitcoin is usually rewarded when people believe adoption, network value, and digital scarcity will grow. Gold is usually rewarded when investors want a traditional hedge outside ordinary financial confidence.

In a liquidity-driven bull market, Bitcoin can dramatically outperform because its market is smaller, more reflexive, and more sensitive to risk appetite. A wave of institutional adoption, ETF flows, or retail enthusiasm can push prices much faster than gold. That upside is why many investors accept Bitcoin's volatility.

In a recession or financial stress scenario, the answer is less obvious. Gold has a longer record of attracting defensive flows. Bitcoin may mature into a more reliable hedge over time, but it has also sold off during periods when investors were forced to raise cash. This is why investors should avoid assuming that Bitcoin always behaves like gold during panic periods.

Bitcoin may lead when liquidity is abundant, speculation is rewarded, and adoption narratives strengthen.

Gold may lead when investors seek a familiar hedge against currency and geopolitical uncertainty.

A blend can reduce regret because each asset can respond to a different driver.

DCA vs lump sum for Bitcoin and gold

Dollar-cost averaging can be especially useful when comparing Bitcoin and gold because both assets are emotional. Bitcoin creates fear of missing out during rallies and fear of collapse during crashes. Gold creates a different problem: investors often buy it only after fear is already high. A recurring contribution plan reduces the pressure to guess the perfect entry point.

For Bitcoin, DCA can be psychologically powerful. It turns volatility into a schedule. Instead of asking whether today is the bottom or top, the investor follows a fixed contribution rule. This does not guarantee better returns than lump sum. In long upward markets, lump sum often wins mathematically because money is invested earlier. But DCA can improve behavior, and behavior is often the real bottleneck.

For gold, DCA is less dramatic but still useful. Gold can move sideways for long periods, then rise quickly during stress. A gradual allocation plan prevents the common mistake of buying too much after a crisis headline. Investors who want a permanent gold allocation can build it systematically instead of reacting to news.

| Strategy | Bitcoin | Gold | Best use case |

|---|---|---|---|

| Lump sum | Higher potential if bought before strong adoption cycles. | Useful when the portfolio lacks any hedge. | Investor has high conviction and accepts timing risk. |

| DCA | Reduces regret and spreads volatility. | Builds hedge gradually without panic buying. | Investor wants discipline and smoother entry. |

| Hybrid | Initial position plus recurring buys. | Core hedge plus annual rebalancing. | Investor wants exposure now while keeping flexibility. |

For a dedicated comparison, read DCA vs lump sum. If you want to model monthly contributions into Bitcoin, gold, or ETFs, start with the DCA Calculator.

How to decide between Bitcoin, gold, and a blended allocation

The easiest way to make the bitcoin vs gold decision is to stop asking which asset is better and start asking which problem you are solving. Are you trying to protect purchasing power? Diversify away from equities? Add asymmetric upside? Hedge monetary uncertainty? Reduce portfolio volatility? Each answer points to a different weight.

- You already own a lot of growth assets.

- You want a lower-volatility hedge.

- You value a long historical record.

- You dislike digital custody complexity.

- You want a crisis asset that is widely understood.

- You have a long time horizon.

- You can tolerate deep drawdowns.

- You believe digital scarcity will keep gaining adoption.

- You can secure your holdings properly.

- You only need a small upside sleeve.

For most households, the decision should also fit cash flow. If you have credit card debt, no emergency fund, or unstable income, Bitcoin and gold allocation debates are secondary. First build financial resilience. Then use satellite assets as part of a broader plan.

A simple framework is to define three buckets. The first bucket is safety: emergency savings, debt control, and short-term cash. The second bucket is core growth: diversified ETFs, retirement accounts, and long-term contributions. The third bucket is optional diversifiers: gold, Bitcoin, and other alternatives. Problems happen when investors skip the first two buckets and overfill the third.

Bitcoin vs gold vs ETFs: each asset has a different job

Most investors should not use Bitcoin or gold as a replacement for a diversified stock and bond portfolio. Broad ETFs remain the core engine for many long-term plans because they give exposure to productive businesses, dividends, earnings growth, and global diversification. Gold and Bitcoin are better viewed as satellite allocations around that core.

| Asset | Main job | Strength | Weakness |

|---|---|---|---|

| Broad ETFs | Long-term wealth building | Diversification and exposure to productive businesses | Market crashes still happen. |

| Gold | Defensive hedge | Long trust history and lower volatility | No cash flow and modest long-term growth. |

| Bitcoin | Asymmetric scarce asset | High upside and portability | Extreme volatility and custody complexity. |

For more portfolio context, read ETF vs crypto: what the data says, top ETFs for long-term investing, and top ETFs for monthly DCA contributions.

What investors get wrong in the Bitcoin vs gold debate

Bitcoin's historical upside is impressive, but buying after major rallies without a risk plan can create poor outcomes.

Both assets require execution discipline. Storage, private keys, fees, and tax records matter.

A useful hedge can become a portfolio problem if the allocation is too large for your goals.

They are both scarcity assets, but volatility, liquidity sensitivity, and investor bases are very different.

Bitcoin and gold are usually satellites. Diversified ETFs still do the heavy lifting for many investors.

Bitcoin can become too large after a bull market. Gold can become too large after fear-driven buying.

Model the decision instead of guessing

A static article can explain the logic, but your own allocation depends on dates, contribution size, risk tolerance, and the rest of the portfolio. Use WhatIfInvested to turn the bitcoin vs gold question into a simulation.

Test Bitcoin, gold, and ETF allocations before committing.

Use the free simulator to compare historical paths. When you need multiple portfolios, saved scenarios, benchmarks, drawdowns, fees, and export-ready reports, compare Premium access.

Bitcoin vs gold FAQ

Is Bitcoin a better store of value than gold?

Bitcoin can offer higher upside because of its fixed supply and adoption curve, but gold has a much longer track record and lower volatility. Bitcoin is not automatically better; it is more aggressive and requires stronger risk tolerance.

Is gold still useful if Bitcoin exists?

Yes. Gold can still serve as a defensive hedge, especially for investors who want a non-digital asset with deep global acceptance and less volatility than crypto.

Should I own both Bitcoin and gold?

Many investors can justify owning both in small amounts. Gold can play defense, while Bitcoin adds asymmetric upside. The key is sizing each position so it supports the portfolio rather than dominating it.

Is Bitcoin more risky than gold?

Yes. Bitcoin has historically been much more volatile and has experienced deeper drawdowns. It also introduces digital custody, regulatory, and platform risks that gold investors may not face in the same way.

How much Bitcoin should a beginner own?

A beginner should usually start very small, if at all. The allocation should be small enough that a severe Bitcoin drawdown would not disrupt the broader plan, emergency fund, or long-term investing behavior.

How much gold should a portfolio hold?

There is no universal answer. Some investors use a 3% to 10% gold allocation as a defensive sleeve, while others hold none. The right weight depends on risk tolerance, income stability, and how much diversification the rest of the portfolio already provides.

Is DCA better than lump sum for Bitcoin or gold?

DCA can reduce timing regret and make volatile assets easier to buy consistently. Lump sum may perform better in rising markets, but DCA can improve behavior. The best choice depends on cash availability, risk tolerance, and whether you can hold through drawdowns.

What is the simplest Bitcoin vs gold strategy?

The simplest strategy is to keep a diversified ETF core, then add small satellite allocations to gold and Bitcoin based on clear rules. Rebalance when the weights drift too far from the intended plan.

This article is for education only and is not financial advice. Historical performance does not guarantee future results. Consider your objectives, risk tolerance, account type, fees, taxes, and local rules before making investment decisions.