Top 5 ETFs for Monthly DCA Contributions

A practical guide to choosing ETFs for monthly dollar-cost averaging, with portfolio roles, account placement, risk controls, and internal tools to help you turn recurring savings into a long-term investing system.

Best ETFs for monthly DCA start with role, not hype

For most long-term investors, the best ETFs for monthly DCA are broad, low-cost, liquid funds that represent a clear role in the portfolio. VTI and IVV can act as core US equity holdings. VEU can add international diversification. AGG can reduce volatility for investors who want bonds. QQQ can be used as a smaller growth tilt, but it should not replace a diversified core for most investors.

The point of monthly dollar-cost averaging is not to find a perfect entry price. The point is to build a repeatable investing habit. A strong DCA portfolio should be simple enough to automate, diversified enough to survive bad periods, and transparent enough that you understand what you own. That is why ETFs for monthly DCA should be chosen for durability first.

- Broad-market ETFs such as VTI or IVV can be strong monthly DCA building blocks because they are diversified, liquid, and low-cost.

- A mix of broad US equity, global equity, bonds, and limited growth exposure usually beats chasing one trendy fund.

- The best ETF is the one you can buy consistently, understand clearly, and keep holding when markets fall.

- Start with one broad-market core ETF, add diversification only when it improves your plan, and use the DCA Calculator to model how recurring contributions may grow over time.

What monthly DCA really means

Dollar-cost averaging means investing a fixed amount of money on a fixed schedule, regardless of what the market did that week or month. Instead of trying to guess the perfect day to buy, you turn investing into a system. When prices are lower, your contribution buys more shares. When prices are higher, it buys fewer shares. Over time, the strategy smooths your entry points and reduces the emotional burden of market timing.

DCA does not guarantee better returns than lump-sum investing. In rising markets, investing a large amount upfront often wins because more money is exposed to growth earlier. But many real investors do not have a large lump sum. They have monthly cash flow from a salary, business income, or budgeting surplus. For them, monthly DCA is not a second-best theory. It is the natural way wealth gets built, and ETFs for monthly DCA can make that process easier to repeat.

The behavioral advantage is huge. A good monthly plan removes the repeated question: "Should I invest now or wait?" That question often causes paralysis. Investors wait for a dip, then fear the dip will become a crash. They wait for confirmation, then feel the market has already moved. A monthly contribution schedule replaces prediction with process.

ETFs can make monthly DCA easier to maintain

ETFs work well for monthly DCA because they combine diversification, transparency, liquidity, and low costs. A single broad-market ETF can hold hundreds or thousands of securities. That means each monthly contribution can instantly spread across many companies, sectors, and sometimes countries. For many beginners, ETFs for monthly DCA are simpler than building a basket of individual stocks.

This matters because repeated small purchases should be efficient. If your plan requires buying twenty individual stocks each month, it becomes harder to maintain. You need more decisions, more tracking, and more emotional judgment. ETFs reduce that friction. They allow you to decide on the plan once, automate the habit, and review the allocation occasionally rather than constantly.

A good ETF still needs a good plan

ETFs do not prevent market drawdowns. They do not remove the need for asset allocation. They do not make short-term money safe. They do not guarantee positive returns. They also do not replace tax planning in taxable accounts.

For investors who want to compare DCA with one-time investing, the Lump Sum vs DCA analysis is a useful next read. If you want to run your own scenario, use the Investment Simulator.

How to choose ETFs for monthly contributions

Monthly DCA rewards consistency, but consistency only helps if the fund is worth holding for years. Before picking an ETF, evaluate the fund's role. Is it your core equity exposure, a diversifier, a bond stabilizer, or a satellite tilt? Most portfolio mistakes start when investors buy funds because they sound exciting rather than because they serve a clear purpose.

| Selection factor | Why it matters for DCA | What to look for |

|---|---|---|

| Expense ratio | Fees compound against you over long periods. | Prefer low-cost funds for core allocations. |

| Liquidity and spread | Monthly purchases can lose value to poor execution. | Look for established funds with tight bid-ask spreads. |

| Diversification | DCA works better when the asset is suitable for long-term holding. | Broad market exposure is usually better than narrow themes for the core. |

| Tracking quality | The ETF should do what it says it does. | Compare official fund pages and long-term tracking information. |

| Tax behavior | Distributions and account type can affect after-tax results. | Use tax-advantaged accounts where appropriate and keep records in taxable accounts. |

| Portfolio overlap | Owning many similar ETFs can create fake diversification. | Check whether funds hold the same large companies. |

For example, VTI and IVV overlap heavily because both are US equity funds, but they are not identical. VTI includes the total US stock market, while IVV tracks the S&P 500. An investor may not need both in the same portfolio unless they intentionally want a particular weighting. Likewise, QQQ can be useful as a growth tilt, but it is more concentrated and should be sized carefully. This is why ETFs for monthly DCA should be selected by portfolio role, not by ticker popularity.

How to compare ETFs for monthly DCA without chasing returns

The biggest mistake investors make when choosing ETFs for monthly DCA is ranking funds only by recent performance. A fund can look perfect after a strong five-year period and still be a poor fit for the role you need. Monthly DCA works best when the fund is suitable for repeated purchases through good markets, bad markets, boring markets, and emotionally difficult markets.

Start by asking whether the ETF belongs in the core or the satellite part of the portfolio. Core ETFs should usually be broad, low-cost, diversified, and easy to keep buying even after a large decline. Satellite ETFs can be more focused, but they should stay smaller because they add concentration risk. This distinction matters more than finding the fund with the most exciting chart.

For example, VTI or IVV can act as a core holding because they provide broad US equity exposure. VEU can be a diversifier because it adds non-US stocks. AGG can be a stabilizer because it adds bond exposure. QQQ can be a growth satellite because it concentrates more heavily in Nasdaq-100 companies. These are different jobs, so they should not be judged by one return number alone.

Use role, cost, overlap, and behavior as the test

A practical ETF comparison should answer four questions. First, what role does this fund play? Second, what does it cost to hold for years? Third, how much does it overlap with what you already own? Fourth, will you actually keep buying it during drawdowns?

This is where ETFs for monthly DCA should be judged differently from short-term trades. A monthly investor is not just buying a ticker. The investor is building a repeatable process. If the fund is too narrow, too expensive, too volatile for the investor's temperament, or too similar to existing holdings, the plan may become harder to follow.

When two ETFs appear similar, simplicity usually wins. If one fund already gives you the exposure you need, adding another fund with nearly identical holdings may only create tracking work. If a new ETF genuinely adds diversification, lowers cost, improves account fit, or supports a specific objective, it may deserve a place in the plan.

| Comparison question | Good sign | Warning sign |

|---|---|---|

| Does the ETF have a clear role? | Core, diversifier, stabilizer, or limited satellite. | You are buying it only because it recently went up. |

| Is the fund affordable to hold? | Low expense ratio for the role it plays. | High fee for exposure you can get cheaper elsewhere. |

| Does it overlap with current holdings? | It adds exposure you do not already have. | It duplicates the same top holdings repeatedly. |

| Can you keep buying it during declines? | The strategy still makes sense after a bad year. | You would abandon it after normal volatility. |

For many readers, the best ETFs for monthly DCA will be the funds that make the plan easier to maintain, not the funds that make the portfolio look more impressive. A recurring contribution system is valuable only if it survives real life. That means the ETF list should be small enough to understand, broad enough to support long-term compounding, and flexible enough to fit your account structure.

Before adding any new ETF, compare it against the current portfolio rather than judging it in isolation. If the new fund improves diversification, reduces cost, or clarifies the strategy, it may help. If it only adds another ticker with similar holdings, it may dilute focus. This is the difference between collecting funds and building a portfolio.

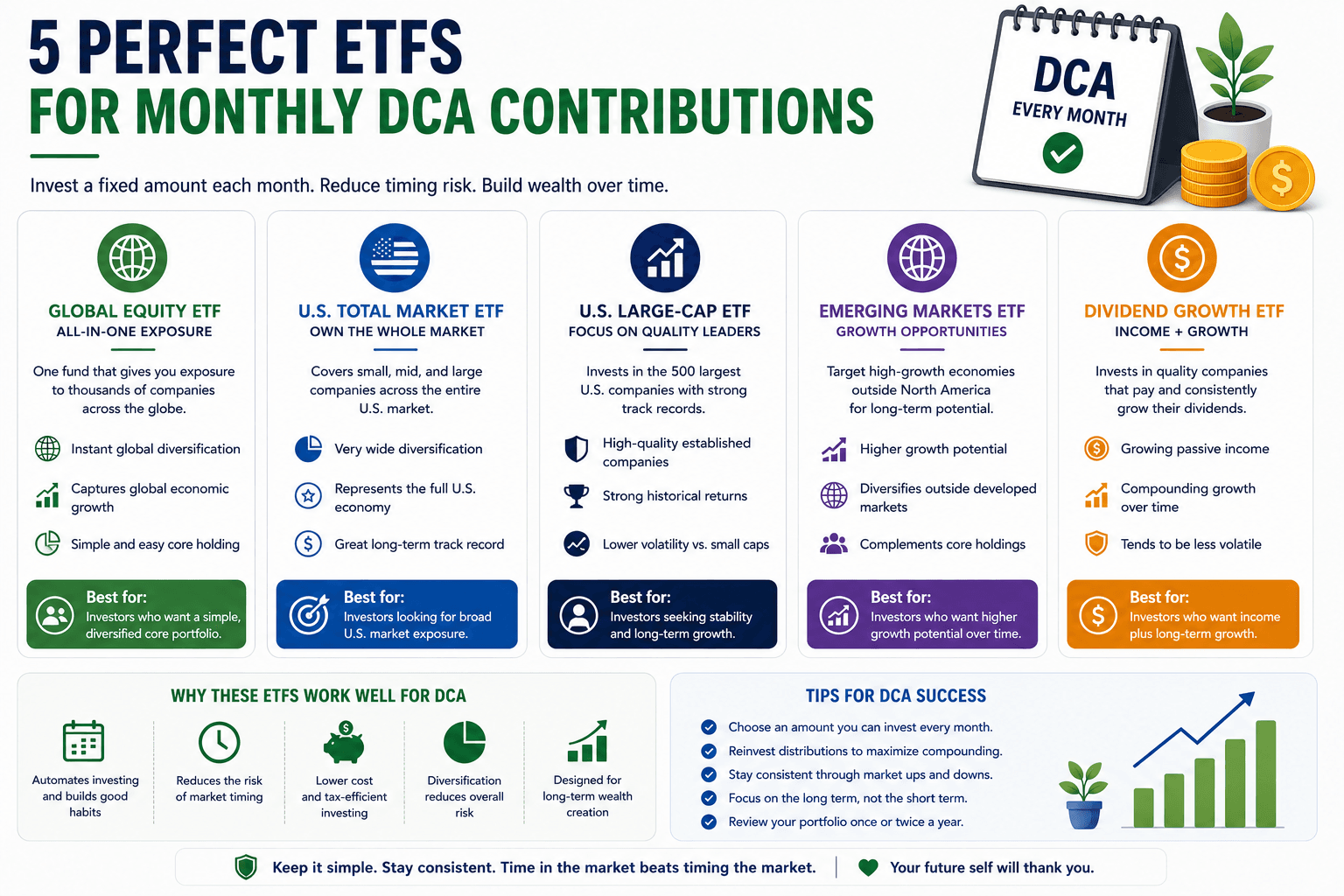

Top 5 ETFs for monthly DCA contributions

The following ETFs are not a personalized recommendation. They are examples of large, widely used ETF categories that can fit a monthly DCA strategy. Always verify the official fund page before investing because fees, holdings, distributions, and index methodology can change. Treat this list of ETFs for monthly DCA as a decision framework, not a buy list.

| ETF | Portfolio role | Why it can fit monthly DCA | Best used as |

|---|---|---|---|

| VTI Vanguard Total Stock Market ETF | Total US equity market | Broad exposure across large, mid, and small US companies, making it a strong one-fund US equity core. | Core holding |

| IVV iShares Core S&P 500 ETF | Large-cap US equity | Tracks major US large companies with strong liquidity and low cost, useful for investors who want S&P 500 exposure. | Core holding |

| VEU Vanguard FTSE All-World ex-US ETF | International equity | Adds non-US developed and emerging-market exposure to reduce dependence on one country. | Diversifier |

| AGG iShares Core U.S. Aggregate Bond ETF | Investment-grade bonds | Can help reduce volatility and provide bond exposure for investors who do not want an all-equity portfolio. | Stabilizer |

| QQQ Invesco QQQ Trust | Nasdaq-100 growth tilt | Provides exposure to large innovative growth companies, but with more concentration risk than broad-market funds. | Satellite |

1. VTI: broad US market core

VTI can fit investors who want broad US exposure in one ticker. Because it includes more than just the largest companies, it gives exposure to the broader US business landscape. For monthly DCA, that simplicity is valuable. A recurring purchase of VTI can represent a complete US equity sleeve without needing separate large-cap, mid-cap, and small-cap funds.

2. IVV: S&P 500 core exposure

IVV is useful for investors who specifically want S&P 500 exposure. The S&P 500 is large-cap focused, but it covers many of the most important US public companies. Monthly contributions into IVV can be simple, low-cost, and easy to understand. The tradeoff is that it is less broad than a total-market fund.

3. VEU: international diversification

VEU can help reduce home-country or US-only concentration by adding non-US equities. This is especially relevant for investors whose portfolio is already dominated by US stocks. International stocks can lag for long periods, which is exactly why a disciplined DCA approach may help investors keep buying when a region is unpopular.

4. AGG: bond exposure for smoother volatility

AGG is not designed to deliver the same growth profile as equity ETFs. Its role is different. It can add stability, income, and diversification for investors who do not want a fully stock-based portfolio. Younger aggressive investors may use little or no bond exposure, while conservative investors may use bonds as a meaningful allocation.

5. QQQ: growth satellite, not the whole plan

QQQ can be attractive because it holds many high-profile growth companies. But investors should be careful: strong historical performance can create performance-chasing behavior. QQQ is more concentrated than broad-market ETFs and may experience deeper swings. In a DCA plan, it often makes more sense as a satellite allocation than as the entire portfolio.

Example monthly DCA portfolio structures

A list of ETFs is useful, but a portfolio needs structure. The right structure depends on your goal, time horizon, risk tolerance, and account type. Below are educational examples, not personal advice. The best ETFs for monthly DCA only work well when the allocation around them is clear.

| Investor profile | Possible monthly allocation | Why it may fit |

|---|---|---|

| Aggressive long-term investor | 70% VTI or IVV, 20% VEU, 10% QQQ | Equity-heavy portfolio with global diversification and a limited growth tilt. |

| Balanced growth investor | 55% VTI or IVV, 20% VEU, 20% AGG, 5% QQQ | Still growth-oriented, but bonds reduce volatility and QQQ remains controlled. |

| Simple one-fund US approach | 100% VTI or 100% IVV | Very simple, but less globally diversified unless other holdings exist elsewhere. |

| Conservative accumulator | 40% VTI or IVV, 20% VEU, 40% AGG | Lower stock exposure can reduce drawdowns, but may also reduce long-term growth. |

The more complex your portfolio becomes, the more you need a rebalancing rule. If your monthly contribution is small, a five-ETF portfolio may create too much operational friction. In that case, a simpler one-ETF or two-ETF structure can be better because it is easier to maintain. Simplicity is often one of the most underrated advantages when choosing ETFs for monthly DCA.

Where should you hold monthly DCA ETFs?

Account placement can matter almost as much as ETF selection. The same ETF may create different after-tax results depending on whether it sits in a TFSA, RRSP, FHSA, IRA, 401(k), or taxable account. Because this site serves both Canadian and US readers, the key is to understand the general account logic and then verify your local rules. ETFs for monthly DCA should be matched with the account that best supports the goal.

| Account type | DCA fit | Practical note |

|---|---|---|

| TFSA | Strong for Canadian investors who want flexible tax-free growth. | Useful for long-term ETF compounding and flexible withdrawals. Compare account order in TFSA vs RRSP vs FHSA. |

| RRSP | Useful when tax deductions are valuable and the money is for retirement. | Can be strong for high-income years, but withdrawals are generally taxable later. |

| FHSA | Potentially useful for eligible Canadian first-home goals. | Equity ETFs may be too volatile if the home purchase is soon. |

| IRA or 401(k) | Common for US retirement-focused DCA. | Tax treatment depends on traditional vs Roth structure and plan rules. |

| Taxable brokerage | Flexible but requires more record-keeping. | Track dividends, capital gains, cost basis, and tax-loss harvesting rules. |

If you are Canadian and choosing between VFV, VOO, VEQT, XEQT, or US-listed ETFs, read VFV vs VOO for Canadians and VEQT vs XEQT. Those pages connect ETF choice with account structure, currency, and simplicity.

How to implement monthly ETF DCA

A good DCA plan should be boring in the best possible way. The fewer decisions you need to make every month, the more likely you are to keep investing through headlines, volatility, and personal distractions.

- Define the monthly amount. Start with a number your budget can support consistently. Use WhatIfBudget if you need to identify surplus cash flow.

- Choose the account first. Decide whether the money belongs in a retirement account, tax-free account, first-home account, or taxable brokerage.

- Pick the ETF roles. Choose core equity, optional international exposure, optional bonds, and any satellite tilt.

- Automate the transfer. Move money from your bank to your brokerage on a fixed schedule.

- Use recurring purchases if available. Some platforms support automated ETF buys or fractional shares.

- Review quarterly or annually. Do not turn DCA into daily monitoring. Review contributions, allocation drift, and whether your goals changed.

If your brokerage does not support automatic ETF purchases, create a calendar reminder. Manual investing can still work if the process is simple. The key is that the contribution happens before lifestyle spending absorbs the cash. ETFs for monthly DCA work best when the contribution habit is protected before the rest of the budget gets noisy.

Tax, rebalancing, and tracking considerations

Monthly DCA creates many small purchases. That is fine inside tax-advantaged accounts, but taxable accounts require better records. Each purchase can become part of your cost basis. Dividends and distributions may also create taxable events depending on your jurisdiction and account type.

Rebalancing is another area where simple rules help. If your target portfolio is 70% stocks and 30% bonds, market movements will eventually push it away from target. You can rebalance by selling overweight assets, but in taxable accounts that may create capital gains. A gentler method is to direct new monthly contributions toward the underweight ETF until the portfolio moves closer to target.

When possible, rebalance with monthly contributions instead of selling. This can reduce taxes and transaction friction.

Consider rebalancing only when an allocation is meaningfully off target. Constant micro-rebalancing can be unnecessary.

Tracking does not need to be complicated. A simple spreadsheet with date, ticker, contribution amount, shares purchased, and account type is enough for many investors. If you use multiple accounts, review your total household allocation rather than judging each account in isolation. This makes ETFs for monthly DCA easier to manage across taxable and tax-advantaged accounts.

Common monthly DCA mistakes

Downturns are uncomfortable, but they are also when DCA buys more shares for the same dollar amount.

A fund that recently outperformed may already reflect high expectations.

VTI, IVV, and QQQ can all hold many of the same large US companies.

ETF choice should connect to taxes, withdrawal needs, and time horizon.

A complicated plan is harder to automate and easier to abandon.

If you need the cash soon, a volatile ETF may be inappropriate no matter how good the long-term return looks.

As income rises, a static monthly amount may become too small relative to your goals.

The best way to avoid these mistakes is to write down your rules before emotions are involved. Decide how much you invest, which ETFs you buy, when you review, and what would justify a change. Then let the system work. A written rule set turns ETFs for monthly DCA into a repeatable investment process instead of a monthly guessing game.

Model the ETF contribution plan before you automate it

Start with the free DCA Calculator to test monthly ETF contributions. When you need multiple portfolios, benchmark comparisons, saved scenarios, and export-ready reports, compare Premium access.

ETFs for monthly DCA FAQ

What is the best ETF for monthly DCA?

There is no single best ETF for everyone. For many investors, a broad-market ETF such as VTI or IVV can be a strong core choice because it is diversified, liquid, and low-cost.

Is DCA better than lump sum investing?

Lump sum often wins in rising markets because money is invested sooner. DCA can still be better behaviorally because it reduces timing anxiety and fits monthly income.

How many ETFs should I use for monthly contributions?

Many investors can build a strong portfolio with one to five ETFs. More ETFs can add complexity and overlap unless each fund has a clear role.

Should I include bond ETFs in a DCA portfolio?

Bond ETFs can help reduce volatility, especially for conservative investors or shorter time horizons. Aggressive long-term investors may use little or no bond exposure.

Can I DCA into ETFs inside a TFSA or RRSP?

Yes. Canadian investors commonly use ETFs inside TFSA and RRSP accounts. The best account depends on tax bracket, goals, withdrawal needs, and contribution room.

Is QQQ good for monthly DCA?

QQQ can fit as a growth satellite, but it is more concentrated than broad-market ETFs. Many investors should size it carefully rather than using it as the entire portfolio.

What if I only have a small amount to invest each month?

Small monthly contributions can still matter over time. Use a low-cost brokerage, consider fractional shares if available, and keep the ETF list simple.

Should I buy ETFs on the same day every month?

A fixed monthly schedule is fine for most investors. The exact day usually matters less than consistency, low costs, and staying invested.

Verify fund details before investing

Before investing, verify the latest fees, holdings, distributions, and risks directly from the fund providers.

- Vanguard VTI official fund page

- iShares IVV official fund page

- Vanguard VEU official fund page

- iShares AGG official fund page

- Invesco QQQ official fund page

This article is for educational purposes only and is not financial advice. Investors should consider their objectives, risk tolerance, fees, taxes, account rules, and local regulations before investing.