🇨🇦 TFSA vs RRSP vs FHSA: Which Account Should You Fund First?

A practical Canadian decision framework for choosing between TFSA, RRSP, and FHSA based on income, taxes, home-buying plans, retirement goals, and flexibility.

FHSA usually deserves first look because it can combine an RRSP-style deduction with a TFSA-style tax-free qualifying home withdrawal.

RRSP can be powerful when your current tax rate is higher than your expected retirement tax rate, especially if you invest the refund.

TFSA is often best when you need tax-free growth, flexible withdrawals, or expect your income to rise later.

Quick Verdict: TFSA vs RRSP vs FHSA

The best account depends on the job the money needs to do. FHSA is usually strongest for eligible first-time home buyers. RRSP is strongest when you want a tax deduction during higher-income years. TFSA is strongest for flexibility, tax-free withdrawals, and saving when your future tax rate may be higher. That is why the TFSA vs RRSP vs FHSA decision should start with your goal, not only the account name.

Most Canadians do not need to pick only one forever. A strong plan often uses all three over time: FHSA for a first home, RRSP for retirement tax planning, and TFSA for flexible long-term compounding.

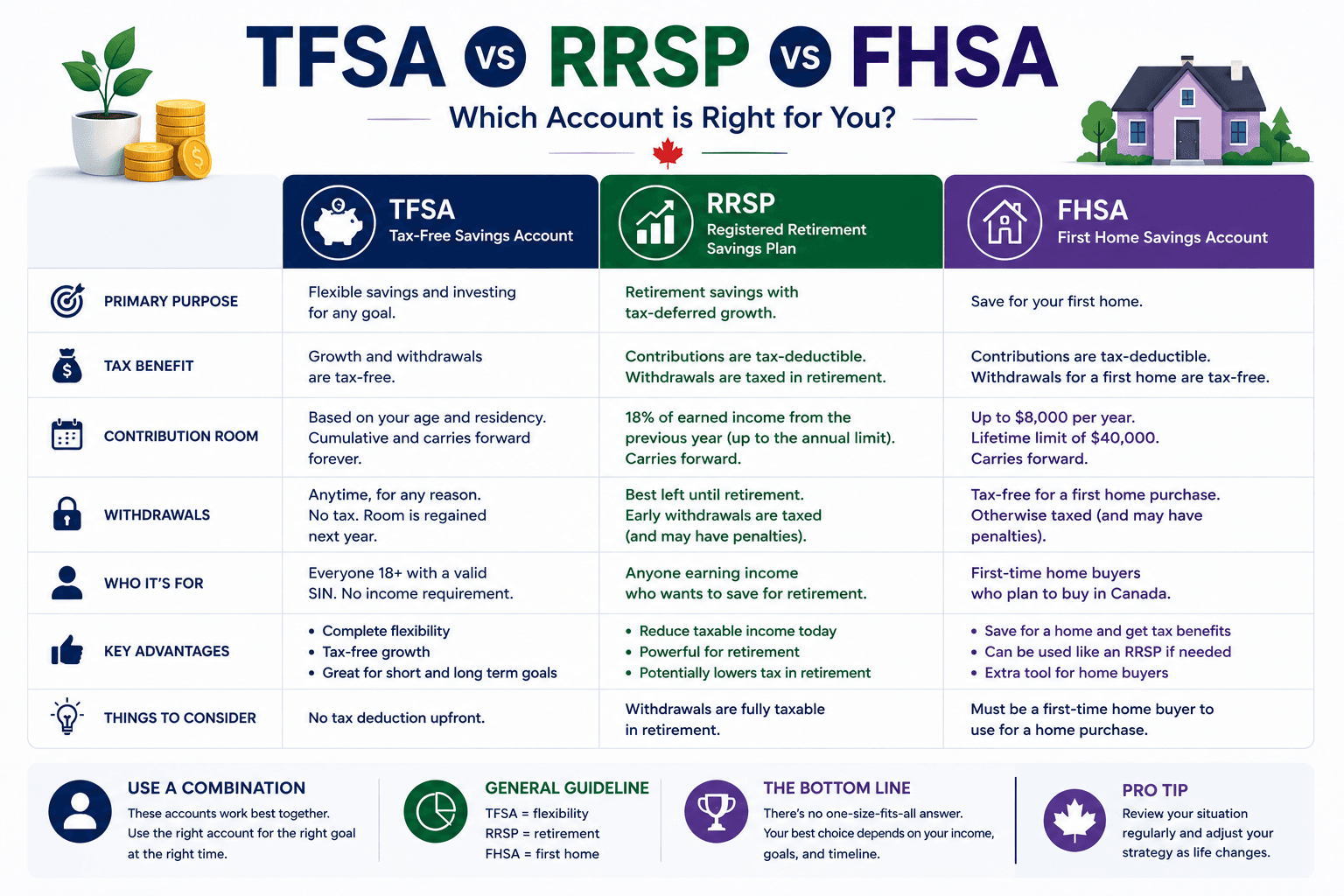

What TFSA, RRSP, and FHSA Actually Do

These accounts are not investments by themselves. They are tax shelters that can hold eligible investments such as cash, GICs, stocks, bonds, and ETFs. The account choice affects taxes, withdrawals, room, and flexibility. A useful TFSA vs RRSP vs FHSA comparison separates the account rules from the investments held inside them.

That distinction matters because many Canadians ask “which account has the best return?” when the better question is “which account creates the best after-tax outcome for this specific goal?” The same ETF can produce a different after-tax result depending on whether it sits in a TFSA, RRSP, FHSA, or taxable account. A dollar meant for a down payment in three years should not be treated the same way as a dollar meant for retirement in thirty years.

TFSA

Contributions use after-tax dollars. Growth and withdrawals are generally tax-free. Withdrawals restore contribution room the following calendar year.

- Best for flexibility

- Useful for low to mid income years

- Strong for long-term tax-free compounding

RRSP

Contributions can reduce taxable income today. Growth is tax-sheltered, and withdrawals are generally taxable later.

- Best for high-income years

- Designed for retirement planning

- Most powerful when future tax rate is lower

FHSA

Contributions can be deductible, and qualifying first-home withdrawals can be tax-free. It is designed for eligible first-time home buyers.

- Best for first-home goals

- Annual and lifetime contribution limits apply

- Has a maximum participation period

For example, a young saver in a modest tax bracket may get less immediate value from an RRSP deduction than a high-income professional. That same young saver may benefit more from the TFSA because they preserve future RRSP room for higher-income years and keep withdrawals flexible. A first-time buyer, however, may put the FHSA ahead of both because the FHSA can combine two benefits that normally live separately: a deduction on contribution and a tax-free qualifying withdrawal.

Current Contribution Limits and Rules to Know

Contribution room is personal, so always verify your own room in CRA My Account before contributing. The general federal limits below are useful for planning, but your available room may be different because of past contributions, withdrawals, pension adjustments, and unused room.

| Account | Current planning limit | Important room rule | Official source |

|---|---|---|---|

| TFSA | The annual TFSA dollar limit is $7,000 for the current planning year. | Withdrawals are added back to contribution room the next calendar year, not immediately. | CRA TFSA room |

| RRSP | The RRSP dollar limit is $33,810 for the current planning year, subject to your personal deduction limit. | Your RRSP deduction limit depends on earned income and pension adjustments. | CRA registered plan limits |

| FHSA | Annual FHSA participation room is generally $8,000, with a $40,000 lifetime FHSA deduction limit. | Unused annual FHSA participation room can carry forward within limits; eligibility and maximum participation period matter. | CRA FHSA deductions |

Which Account Should You Fund First?

Use this funding order as a starting framework. The right order depends on home-buying plans, income level, employer pension, emergency fund needs, and whether your future tax rate is likely to be higher or lower. In practice, TFSA vs RRSP vs FHSA is a funding-order question before it is an investment-selection question.

If you plan to buy a first home

- Start with FHSA if eligible.

- Use TFSA for extra down-payment flexibility.

- Use RRSP if your income makes the deduction valuable or if the Home Buyers' Plan fits your strategy.

If retirement is the main goal

- Use RRSP during high-income years.

- Use TFSA when you value tax-free withdrawals and benefit flexibility.

- Consider both if you can max more than one account.

- Confirm short-term cash needs first. Do not lock money into a volatile portfolio if you need it soon.

- Check FHSA eligibility. If you qualify and want a first home, FHSA is usually hard to beat.

- Compare tax brackets. RRSP works best when your deduction today is worth more than taxes paid later.

- Use TFSA for flexibility. It is excellent when your income may rise, your goals are uncertain, or you want tax-free withdrawals.

A practical funding order for most situations

If you are eligible for an FHSA and genuinely want to buy a first home, start there unless your timeline is so short that investment risk is inappropriate. After that, the TFSA often acts as the flexible second bucket. RRSP then becomes more attractive as income rises, especially when deductions can be claimed in a higher bracket and the refund is invested rather than spent.

If you are not a home buyer, the decision is usually TFSA versus RRSP. In lower-income years, TFSA can preserve optionality. In high-income years, RRSP can reduce taxable income and help you shift taxation into a future lower-income period. If you have an employer match in a group RRSP or pension plan, that match should usually be treated as a priority because it is part of your compensation.

How to avoid treating the accounts like a one-time choice

The TFSA vs RRSP vs FHSA decision should be reviewed as your life changes. A student, a new graduate, a first-time buyer, a parent, a self-employed worker, and a near-retiree do not need the same account order forever. Income changes can make RRSP deductions more or less valuable. A home purchase goal can make FHSA room urgent. A period of uncertainty can make TFSA flexibility more important than a deduction.

A simple review rhythm works well. Once per year, compare your current tax bracket, your expected next major goal, your contribution room, and your time horizon. Then decide where the next twelve months of savings should go. This keeps the TFSA vs RRSP vs FHSA choice practical instead of theoretical. The account you funded first last year may not be the account that deserves the next dollar this year.

This also prevents a common planning mistake: optimizing for tax savings while ignoring behavior. The best account is the one you can fund consistently, invest appropriately, and use for the intended goal. A perfect RRSP deduction is less useful if the refund is spent. A flexible TFSA is less useful if it is raided every few months. A powerful FHSA is less useful if short-term home money is invested too aggressively.

TFSA vs RRSP vs FHSA Side-by-Side Comparison

| Feature | TFSA | RRSP | FHSA |

|---|---|---|---|

| Tax deduction | No deduction | Contributions may be deductible | Contributions may be deductible |

| Tax on growth | Generally tax-free | Tax-deferred until withdrawal | Tax-free if used for qualifying first home |

| Withdrawals | Generally tax-free | Generally taxable as income | Tax-free for qualifying home purchase; otherwise taxable/transfer rules apply |

| Best for | Flexibility, lower-income years, tax-free compounding | High-income years and retirement planning | Eligible first-time home buyers |

| Benefit impact | Withdrawals usually do not count as taxable income | Withdrawals can affect income-tested benefits | Qualifying withdrawals are tax-free |

| Common mistake | Re-contributing too soon after a withdrawal | Spending the tax refund instead of investing it | Opening too late or ignoring the participation window |

Tax Bracket Strategy: When RRSP Beats TFSA, and When It Does Not

The RRSP is often misunderstood. It is not simply “better” because it gives a refund. The refund is really a tax deferral. You get a deduction today, your investment grows tax-sheltered, and withdrawals are taxed later. The strategy works best when the deduction happens at a higher tax rate than the future withdrawal.

Imagine two Canadians who each contribute the same amount to an RRSP. One is in a high marginal tax bracket and expects lower taxable income in retirement. The RRSP deduction is valuable because it reduces high-tax income today, and the future withdrawal may be taxed at a lower rate. Another person is early in their career, earning modest income, and expects promotions later. For that person, using TFSA now and saving RRSP room for future high-income years can be smarter.

| Situation | Often stronger account | Why it can work |

|---|---|---|

| Low income today, higher income expected later | TFSA | Preserves RRSP room for higher-value deductions later and keeps withdrawals flexible. |

| High income today, lower retirement income expected | RRSP | Deduction can be valuable today, with potential lower-tax withdrawals later. |

| Eligible first-time home buyer | FHSA | Can combine deduction now with tax-free qualifying home withdrawal later. |

| Uncertain goal or emergency flexibility needed | TFSA | Withdrawals are generally tax-free and do not create taxable income. |

The biggest mistake is judging RRSP only by the size of the refund. A large refund feels good, but the long-term result depends on what you do with it. If the refund is invested in a TFSA, used to pay high-interest debt, or reinvested into the RRSP, the strategy becomes much stronger. If it disappears into lifestyle spending, the RRSP advantage is weakened.

Examples by Canadian Saver Profile

New graduate or early career

TFSA often comes first because income may rise later and flexibility matters. If you may buy a first home, open an FHSA early and contribute when cash flow allows.

Couple saving for a first home

FHSA usually gets priority if both partners are eligible. Extra savings can go to TFSA for flexibility and emergency reserves.

High earner with stable income

RRSP deductions can be valuable, especially if retirement withdrawals are expected in a lower tax bracket. Reinvesting the refund is key.

Self-employed or variable income

TFSA can provide flexibility in uncertain cash-flow years. RRSP can be used more heavily in stronger income years.

Example: early-career investor

Someone earning a modest salary with no immediate home plans may start by building an emergency fund, then investing monthly inside a TFSA. If their income rises sharply later, they can shift new money toward RRSP contributions when the deduction becomes more valuable. This approach keeps early savings flexible and avoids using RRSP room during lower-value deduction years.

Example: first-time home buyer

A first-time buyer with a realistic purchase timeline may open an FHSA as soon as eligible, even if the first contribution is small. Opening the account matters because participation timelines are tied to the account. Once the FHSA is funded, extra savings can go to a TFSA to keep down-payment flexibility. If the purchase timeline is short, the investments inside those accounts should usually be conservative.

Example: established high earner

A high-income earner who already has emergency savings and no near-term home purchase may prioritize RRSP contributions, especially if they expect a lower tax rate in retirement. A strong version of this strategy reinvests the tax refund into the TFSA or RRSP. That refund discipline can make a meaningful difference over decades.

Couples Strategy: Coordinating TFSA, RRSP, and FHSA as a Household

Households should think beyond individual accounts. A couple may have two TFSAs, two RRSPs, and potentially two FHSAs if both partners are eligible. That creates planning room, but it also creates coordination problems. The goal is to use the household’s combined tax situation, home plans, and income stability instead of optimizing each account in isolation.

If both partners qualify as first-time home buyers, opening and funding both FHSAs can be powerful. Each person’s eligibility and room should be checked individually. If one partner earns much more than the other, RRSP contributions may be more valuable for the higher-income partner, while TFSA contributions may still be useful for the lower-income partner’s flexibility. If one partner has an employer pension, the other partner’s RRSP and TFSA may become more important for balancing retirement income.

For home-buying couples

- Check FHSA eligibility for both partners.

- Keep short-term down-payment money conservative.

- Use TFSAs for flexible extra savings and closing-cost buffers.

For retirement-focused couples

- Compare marginal tax rates before deciding who contributes to RRSP.

- Use TFSAs to create tax-free retirement flexibility.

- Review pension income, RRSP/RRIF withdrawals, and taxable accounts together.

A good household plan also reduces emotional friction. Instead of debating every month, decide a default rule: first fund emergency savings, then FHSA if buying a home, then split between TFSA and RRSP according to tax bracket and timeline. Revisit the rule once or twice a year rather than constantly changing direction.

What Should You Hold Inside These Accounts?

The account is only the tax wrapper. The investment inside should match the goal and timeline. A home down payment needed soon should usually be invested more conservatively than a retirement portfolio with decades to compound.

This is where many savers accidentally take too much or too little risk. A TFSA can hold long-term equity ETFs, but it can also hold cash for a near-term goal. An RRSP can hold a diversified retirement portfolio, but someone close to retirement may need less volatility than someone in their twenties. An FHSA can hold growth investments if the home purchase is many years away, but a purchase planned within a couple of years usually calls for capital preservation.

| Goal | Possible account | Possible investment approach |

|---|---|---|

| Emergency fund | TFSA or taxable savings | High-interest savings or short-term cash equivalents |

| First-home purchase soon | FHSA / TFSA | Cash, GICs, or low-volatility holdings matching the timeline |

| Long-term retirement | RRSP / TFSA | Diversified ETFs such as global equity or balanced ETF portfolios |

| Long-term wealth building | TFSA / RRSP | Broad market ETF strategy, automated contributions, annual review |

For ETF ideas, compare VEQT vs XEQT, review VFV vs VOO for Canadians, or test recurring contributions with the DCA Calculator.

Withdrawal Planning: The Part Most People Ignore

Contribution strategy gets most of the attention, but withdrawal strategy can be just as important. TFSA withdrawals are generally the most flexible because they are not taxable and the room returns the following calendar year. RRSP withdrawals are taxable, which means they can affect your marginal tax rate and income-tested benefits. FHSA withdrawals are powerful when they qualify for a first-home purchase, but non-qualifying outcomes need careful handling.

For retirement, many Canadians benefit from having both RRSP and TFSA assets. RRSP/RRIF withdrawals can provide taxable retirement income, while TFSA withdrawals can cover extra spending without increasing taxable income. That flexibility can help manage tax brackets, benefit thresholds, and one-time expenses. A retiree with only RRSP assets has less control because every withdrawal is taxable income.

For home buying, withdrawal planning means matching the account to the timeline. FHSA can be excellent for the down payment, but market risk should be reduced as the purchase gets closer. TFSA can provide a flexible reserve for inspections, moving costs, furniture, emergency repairs, or closing costs. RRSP Home Buyers' Plan may help some buyers, but it creates a repayment obligation, so it should be compared carefully against other options.

Withdrawal planning is also where the TFSA vs RRSP vs FHSA comparison becomes very personal. Two people can contribute the same amount, earn the same investment return, and still get different results if one needs the money for a home, one needs flexible cash flow, and one expects lower retirement income. That is why the right account order should be tied to a real use case, not only to a generic tax rule.

Before withdrawing, ask what happens after the money leaves the account. A TFSA withdrawal may restore room next year, but not immediately. An RRSP withdrawal may create taxable income. A qualifying FHSA withdrawal may be tax-free, but only if the conditions are met. The account that looked best during contribution years can become less attractive if the exit plan is ignored.

Common Mistakes and How to Avoid Them

- Over-contributing: check CRA My Account and keep your own records before adding lump sums.

- Re-contributing TFSA withdrawals too early: TFSA room from withdrawals generally returns the next calendar year.

- Spending the RRSP refund: the RRSP strategy is much stronger when the refund is invested, not consumed.

- Using all-equity ETFs for short-term home money: if the purchase is near, volatility can hurt at exactly the wrong time.

- Ignoring future tax rate: RRSP is not automatically better than TFSA. The tax-rate difference matters in any serious TFSA vs RRSP vs FHSA review.

- Forgetting spouse or partner coordination: couples often miss opportunities by planning each account separately instead of optimizing household tax brackets and goals.

- Letting account choice delay action: a good-enough automated plan usually beats months of indecision. Start with the most logical account, then refine annually.

Use WhatIfBudget to estimate monthly surplus, then model investing scenarios with the Investment Simulator.

Frequently Asked Questions

Should I max my TFSA or RRSP first?

If your current tax rate is high and your retirement tax rate may be lower, RRSP can be attractive. If you need flexibility or expect higher income later, TFSA often comes first. The broader TFSA vs RRSP vs FHSA decision also depends on whether you qualify for FHSA and plan to buy a first home.

Is FHSA better than RRSP for first-time home buyers?

For eligible first-time home buyers, FHSA is often more attractive because it can provide a deduction and a tax-free qualifying home withdrawal.

Can I use FHSA and RRSP Home Buyers' Plan together?

Yes, these can generally be combined if you meet the eligibility rules for each program. Confirm the latest CRA rules before acting.

What happens if I do not buy a home with my FHSA?

You may be able to transfer eligible FHSA property to an RRSP or RRIF on a tax-deferred basis, subject to FHSA rules and timelines.

Does TFSA room come back after withdrawal?

Yes. TFSA withdrawals are generally added back to contribution room at the beginning of the following calendar year.

Can I hold ETFs in TFSA, RRSP, and FHSA?

Yes, qualified ETFs can generally be held in these accounts. The right ETF mix depends on your timeline, risk tolerance, and goal.

Is TFSA better than RRSP for low income?

Often, yes. If your current tax rate is low and your income may rise later, TFSA can preserve RRSP room for future years when the deduction may be more valuable.

Should couples fund both FHSAs?

If both partners are eligible first-time home buyers, funding both FHSAs can be useful. Each person should confirm eligibility, contribution room, and the home purchase timeline.

Should I invest my RRSP refund?

Usually yes. Reinvesting the refund into a TFSA, RRSP, or debt repayment often makes the RRSP strategy much stronger than spending the refund.

Is FHSA worth opening if I am not sure I will buy a home?

It can be worth considering if you are eligible, but the decision depends on your plans and timeline. If you do not buy, eligible transfers to an RRSP or RRIF may be possible under FHSA rules.