Bitcoin DCA Simulation: What $1,000/Month Since 2017 Shows

This Bitcoin DCA simulation studies a high-commitment plan: investing $1,000 every month from 2017 through the original model period. The point is not to predict the next cycle. It is to understand discipline, drawdowns, position sizing, and how a recurring crypto strategy behaves when the asset is extremely volatile.

Quick answer: what this Bitcoin DCA simulation shows

A $1,000/month Bitcoin DCA plan starting in 2017 would have been a powerful case study in disciplined investing. Under the original model assumptions, the recurring purchases accumulated roughly 17.23 BTC and produced a very large ending value because the plan kept buying through bear markets, recoveries, and renewed bull-market phases.

The important lesson is not that every future Bitcoin plan will produce the same result. It will not. The useful lesson is that a recurring plan changes the investor's job. Instead of trying to guess the perfect entry point, the investor must decide whether the monthly amount is affordable, whether the allocation is appropriate, whether they can tolerate drawdowns, and whether the custody and tax tracking process is strong enough.

That makes this article different from the smaller $100/month Bitcoin case study. A $100 plan is mainly about habit formation and accessibility. A $1,000/month plan is about serious portfolio impact. The dollar amount is large enough that Bitcoin can become a meaningful part of net worth, which means risk control matters as much as return.

| Question | Answer from the case study | What investors should learn |

|---|---|---|

| Does DCA remove Bitcoin risk? | No. | DCA reduces entry-date pressure, but Bitcoin remains highly volatile. |

| Why did the result look strong? | Consistent buying through multiple cycles. | Bear-market purchases mattered because they accumulated more BTC per dollar. |

| Is $1,000/month appropriate for everyone? | No. | The contribution must fit income, emergency savings, debt, and total portfolio allocation. |

| What should be simulated next? | Fees, start dates, allocation caps, and exits. | The same contribution can behave differently when assumptions change. |

Practical next step: use the Investment Simulator to test your own start date and contribution amount. Compare Premium plans when you need saved scenarios, exports, fees, and deeper comparison workflows.

How the $1,000 monthly Bitcoin DCA model works

The model is intentionally simple. It assumes a fixed monthly contribution, converts that contribution into Bitcoin using historical prices, deducts a small fee assumption, and tracks the cumulative BTC balance over time. The same rule applies whether Bitcoin is rising, falling, or moving sideways.

This structure is useful because it removes hindsight decisions. The plan does not buy more only after the chart looks obvious. It does not pause only because sentiment becomes negative. It follows the same contribution schedule, which makes the backtest easier to interpret.

| Model input | Assumption | Why it matters |

|---|---|---|

| Contribution | $1,000 per month | Large enough to create meaningful portfolio exposure. |

| Start year | 2017 | Captures a major bull market, deep bear markets, and recoveries. |

| Purchase rule | Same amount each month | Removes market-timing decisions from the simulation. |

| Fees | Small fee assumption | Prevents the model from pretending execution is always free. |

| Ending value | BTC accumulated multiplied by final model price | Shows the outcome under one valuation date, not a guarantee. |

Bitcoin itself is based on the original peer-to-peer electronic cash design described in the Bitcoin white paper. That protocol context matters, but an investment backtest still needs portfolio discipline. Technology, adoption, liquidity, regulation, custody, and market demand all affect investment outcomes. For the broader limits behind WhatIfInvested historical models, review the methodology.

A good Bitcoin DCA simulation should therefore show more than the final number. It should show contribution path, average cost behavior, drawdowns, concentration risk, and the psychological reality of continuing during long declines. Without those pieces, the result can look cleaner than the lived experience.

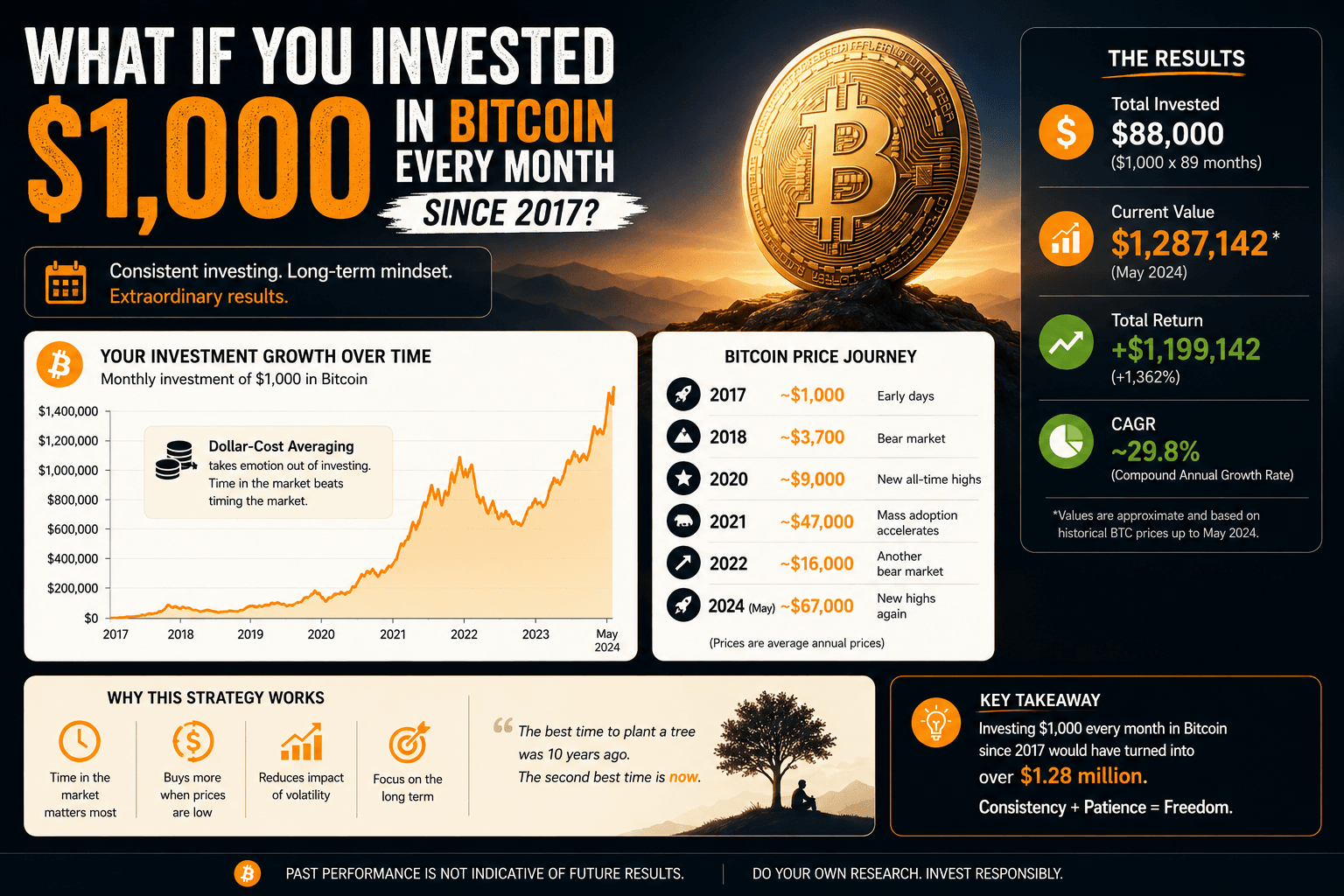

Bitcoin DCA simulation results from the original model

Under the original simulation assumptions, investing $1,000 per month would have accumulated roughly 17.23 BTC over the modeled period. The ending portfolio value was very high because the strategy accumulated Bitcoin before major price appreciation and kept buying during lower-price environments.

The result is impressive, but it should be read carefully. A backtest is not a forecast. The contribution schedule benefited from a specific historical path. A different start date, final date, fee assumption, purchase day, tax treatment, custody choice, or allocation limit could change the result materially.

| Metric | Original model result | Interpretation |

|---|---|---|

| Total contributed | About $100,000+ | The investor committed serious capital over many months. |

| BTC accumulated | About 17.23 BTC | Lower-price months added more BTC per dollar invested. |

| Ending value | About $1.1M in the original model | The result depends heavily on historical Bitcoin appreciation. |

| Main driver | Persistence through downturns | The plan kept buying when sentiment was uncomfortable. |

The real insight is that consistency created exposure across multiple market conditions. In a rising market, DCA participates gradually. In a falling market, DCA lowers the average purchase price but increases emotional pressure. In a long sideways market, DCA requires patience because the payoff is not immediate.

This is why DCA should be evaluated as a process, not only as a final account value. The investor must survive the journey. If the position becomes too large relative to net worth, the strategy can become psychologically fragile even if the spreadsheet looks attractive.

The drawdown risk behind the headline return

Bitcoin DCA can reduce the risk of putting all the money in at one unlucky moment. It does not remove Bitcoin's volatility. Once the accumulated Bitcoin balance becomes large, new monthly contributions become small relative to the total portfolio value. At that point, a major Bitcoin drawdown can create large dollar losses even though the investor is still following the plan.

This is the part many high-return case studies understate. Early in a DCA plan, volatility can feel useful because lower prices buy more units. Later, volatility can feel threatening because the portfolio is large. A $1,000 monthly buyer can eventually face portfolio swings that are many times larger than the monthly contribution.

Market risk

Bitcoin can move sharply in both directions, and historical recoveries do not guarantee future recoveries.

Behavior risk

The investor may stop buying or sell during the exact period when the DCA plan was supposed to keep working.

Concentration risk

A successful plan can make Bitcoin too large a share of the portfolio unless allocation rules are defined.

A useful guardrail is to define the maximum percentage of total investable assets that can be allocated to Bitcoin. For one investor, that may be 2% to 5%. For another, it may be higher. The right number depends on risk tolerance, income stability, emergency savings, debt, investment horizon, and whether the investor can tolerate large temporary losses without abandoning the plan.

Bitcoin DCA versus lump sum investing

Lump sum investing can outperform when the asset rises soon after the investment date because more capital is exposed earlier. DCA can help when the investor is unsure about timing, uncomfortable with a large one-time purchase, or trying to avoid the regret of buying right before a major decline.

For Bitcoin, this tradeoff is especially important. A lump sum buyer who enters near a major low can look brilliant. A lump sum buyer who enters near a cycle top can spend years underwater. DCA smooths the entry path, but it can also underperform if Bitcoin rises quickly and never revisits lower prices.

| Strategy | Strength | Weakness | Best fit |

|---|---|---|---|

| Monthly DCA | Reduces entry-date regret and supports habit. | Can lag a strong early bull market. | Investors who value process and emotional control. |

| Lump sum | Maximizes immediate exposure. | High regret and drawdown risk if timing is poor. | Investors with high conviction and strong risk capacity. |

| Hybrid | Combines partial immediate exposure with recurring buys. | Requires clear allocation and rebalancing rules. | Investors who want participation without all-in timing risk. |

For a broader strategy view, compare this case study with DCA vs Lump Sum and Best Dollar-Cost Averaging Strategies. The goal is not to find one strategy that wins every time. The goal is to match the strategy to the investor's psychology, time horizon, and risk capacity.

Why Bitcoin market cycles change the DCA experience

The same monthly contribution can feel very different depending on the market cycle. During a bull market, DCA feels rewarding because the portfolio value rises quickly. During a bear market, DCA feels uncomfortable because every new purchase may decline soon after. During a sideways market, DCA feels slow because progress is mostly measured in units accumulated, not portfolio value.

This cycle behavior matters because the investor's emotions often move opposite to the best process. Buying after a large rally feels exciting but may add at high prices. Buying during a deep decline feels dangerous but may add more BTC per dollar. A rules-based Bitcoin DCA simulation helps reveal that tension before real money is committed.

Bull markets

DCA participates, but each monthly contribution buys fewer BTC as prices rise.

Bear markets

DCA accumulates more BTC per dollar, but confidence is usually lowest.

Sideways markets

DCA tests patience because the strategy may not feel rewarding for months.

The best response is to define the plan before the cycle becomes emotional. How much will be invested monthly? What is the maximum allocation? When will the position be reviewed? Will gains be rebalanced? What happens if the asset falls 50%? These questions matter more for a $1,000/month plan than for a small habit-building contribution.

Where a $1,000/month Bitcoin plan fits in a portfolio

A $1,000 monthly Bitcoin plan is not just a savings habit. For many households, it is a major allocation decision. Before committing to that amount, the investor should know whether emergency savings are complete, whether high-interest debt is under control, and whether the rest of the portfolio is diversified.

Bitcoin has different risk characteristics than broad equity funds, bonds, cash, or real estate. It does not produce cash flow. It can be affected by regulation, exchange liquidity, custody practices, sentiment, security events, and adoption narratives. That does not make it automatically bad or good. It means the position should be sized intentionally.

| Investor situation | Bitcoin DCA consideration | Better next step |

|---|---|---|

| No emergency fund | $1,000/month may be too aggressive. | Build cash protection first. |

| High-interest debt | Debt payoff may provide a more reliable benefit. | Compare interest rates and risk before investing heavily. |

| Diversified base portfolio | Bitcoin can be modeled as a satellite allocation. | Set a maximum allocation and rebalance rule. |

| High crypto conviction | Monthly DCA may fit, but drawdowns must be expected. | Simulate multiple start dates and downside scenarios. |

A strong portfolio process asks: what happens if the strategy succeeds? If Bitcoin rises dramatically, the position may become too large. What happens if it fails? If Bitcoin falls sharply, the investor must know whether they will continue, pause, rebalance, or stop. A premium workflow becomes useful when these scenarios need to be compared and saved.

Scenario variations every serious Bitcoin DCA simulation should test

The base case is useful, but one path is not enough. A serious Bitcoin DCA simulation should test multiple versions of the same plan because the investor rarely experiences the perfect textbook setup. Contribution size can change. Fees can change. The purchase day can change. The investor may pause during stress, rebalance after gains, or reduce the contribution after income changes.

Testing scenario variations is especially important for a $1,000 monthly plan because the dollar amount is large. A small modeling error can become meaningful. A few months of missed contributions can change accumulated BTC. A higher fee or spread can reduce units purchased. A later start date can turn an impressive historical result into a much less exciting outcome.

| Scenario to test | What changes | Why it matters |

|---|---|---|

| Lower contribution | $250 or $500 per month instead of $1,000. | Shows whether a smaller plan still supports the goal with less pressure. |

| Delayed start | Begin after a major price increase. | Reveals how sensitive the result is to the starting point. |

| Pause during stress | Skip several bear-market months. | Shows the cost of stopping when the plan is emotionally hardest. |

| Higher fee or spread | Use a less efficient execution assumption. | Shows how friction compounds across recurring purchases. |

| Allocation cap | Stop or reduce purchases once Bitcoin reaches a portfolio percentage. | Controls concentration risk when the strategy succeeds. |

The allocation-cap version is often the most useful for serious investors. Without a cap, a successful Bitcoin plan can dominate the portfolio. With a cap, the investor can define a rule such as: keep Bitcoin below 10% of investable assets, rebalance annually, or redirect new contributions to diversified investments once the target is reached.

This is also where the premium workflow becomes more relevant. A free simulation can answer one question. A serious plan often needs multiple saved scenarios, notes, exports, and side-by-side comparisons. The value is not more complexity for its own sake. The value is seeing how fragile or durable the plan remains when assumptions change.

Custody, taxes, and tracking matter in a high-value Bitcoin plan

A Bitcoin DCA backtest can look clean because every monthly purchase is treated as a simple row in a model. Real life is messier. The investor needs to choose where purchases happen, how records are stored, whether assets stay on an exchange, how tax lots are tracked, and how security is handled.

Custody is not a small detail when the position becomes valuable. Leaving everything on an exchange may be convenient, but it introduces platform risk. Self-custody can reduce platform dependence, but it introduces personal security responsibility. A lost seed phrase, weak device security, phishing attack, or poorly managed backup can be as damaging as a market crash.

Execution records

Track dates, amounts, fees, prices, and units purchased. Every recurring buy becomes part of the cost basis history.

Custody rules

Decide when to move assets, how backups are protected, and who can access recovery information if needed.

Tax planning

Sales, swaps, and spending may create taxable events depending on jurisdiction. Keep records before the position becomes large.

Tax treatment varies by country and personal situation, so this article cannot give tax advice. The practical point is simpler: a $1,000/month Bitcoin plan can create many purchase lots. If the investor eventually sells part of the position, accurate records become important. Tracking should begin at the start, not after the portfolio becomes complicated.

Security planning should also scale with value. A small account may feel easy to manage casually. A six-figure or seven-figure position cannot be treated casually. A strong DCA plan is therefore not only a contribution schedule. It is a complete operating system: contribution rule, allocation rule, custody rule, recordkeeping rule, and review rule.

Who should consider, reduce, or avoid a $1,000/month Bitcoin plan?

The right conclusion from this Bitcoin DCA simulation is not that every investor should copy the $1,000 amount. The right conclusion is that contribution size must match financial strength. A high monthly Bitcoin contribution may be reasonable for someone with stable income, no high-interest debt, a complete emergency fund, and a diversified base portfolio. The same contribution may be reckless for someone who is using short-term cash, carrying expensive debt, or still building basic savings.

| Investor profile | What the model suggests | Better action |

|---|---|---|

| Stable income, strong savings, diversified portfolio | A $1,000/month Bitcoin DCA plan can be tested as a satellite strategy. | Model allocation caps, drawdowns, and rebalancing rules. |

| Good income but limited emergency fund | The contribution may be too high until cash reserves improve. | Split the amount between emergency savings and smaller crypto DCA. |

| High-interest debt or unstable cash flow | The plan adds risk before the foundation is ready. | Prioritize debt, emergency savings, and budget stability first. |

| Beginner investor | The historical result can be misleading if risk is not understood. | Start with a smaller contribution and learn through simulation. |

This section is the bridge between curiosity and action. If the plan is affordable, simulate it. If the plan is emotionally exciting but financially tight, reduce it. If the plan only works when Bitcoin goes up quickly, it is not a robust plan. A serious strategy should still make sense during a bear market, a sideways market, and a delayed recovery.

For most users, the best path is staged. First, use the free Investment Simulator to understand the historical behavior. Then use a simpler DCA calculator to test contribution discipline. Finally, move to a premium comparison workflow when the amount is large enough that saved scenarios, fees, exports, and side-by-side assumptions can improve decisions.

Use the right WhatIfInvested tool for the next decision

A case study is useful, but the next decision should use your own assumptions. Change the contribution, start date, asset mix, fees, and time horizon. Then compare whether the plan still makes sense under stress.

Investment Simulator

Best for testing historical asset paths and seeing how recurring investing behaved over time.

DCA Calculator

Best for understanding recurring contribution mechanics and simple forward-looking scenarios.

Premium tools

Best for advanced comparisons, saved scenarios, fees, reports, and multi-scenario planning.

Common mistakes in a Bitcoin DCA simulation

Looking only at the ending value

The ending value may look impressive, but the investor still had to live through drawdowns, uncertainty, and long periods where the strategy felt wrong.

Ignoring position size

A $1,000/month Bitcoin plan can become a large allocation quickly. Define the maximum percentage of the portfolio before the position grows.

Forgetting fees and taxes

Fees, spreads, tax lots, and capital gains rules can change real-world outcomes. Backtests should be treated as educational approximations.

Using money needed soon

Bitcoin is too volatile for money needed for rent, emergency reserves, near-term debt, or short-term goals.

Assuming the past will repeat

The historical path from 2017 onward was extraordinary. Future returns can be lower, more volatile, or negative for long periods.

Frequently asked questions

What is a Bitcoin DCA simulation?

A Bitcoin DCA simulation models recurring Bitcoin purchases over time. It shows how fixed contributions would have accumulated BTC and changed portfolio value across different market conditions.

Would investing $1,000/month in Bitcoin since 2017 have worked?

Under the original model assumptions, the result was very strong because Bitcoin appreciated significantly and the plan kept buying through downturns. That does not guarantee future results.

Is Bitcoin DCA safer than lump sum investing?

DCA can reduce entry-date risk and make execution easier, but it does not remove Bitcoin volatility, custody risk, tax complexity, or the possibility of large losses.

How much should I DCA into Bitcoin each month?

The amount should fit your income, emergency fund, debt, risk tolerance, and total portfolio allocation. A $1,000/month plan is serious and should be tested against downside scenarios.

Should I use Bitcoin DCA for money I need soon?

No. Money needed for rent, emergency savings, taxes, debt payments, or short-term goals should not rely on a volatile asset like Bitcoin.

How is this different from the $100/month Bitcoin case study?

The $100/month case study is mainly about habit and accessibility. The $1,000/month case study is about meaningful allocation, drawdown risk, and serious portfolio impact.

What tool should I use after reading this article?

Start with the Investment Simulator to test historical scenarios. Use Premium tools if you need advanced comparisons, saved scenarios, fees, and export-ready reports.

Is this article financial advice?

No. It is educational content. Bitcoin is volatile and speculative, and investment decisions should consider personal risk tolerance, financial situation, taxes, and professional advice when needed.

The real lesson is discipline plus risk control

This Bitcoin DCA simulation shows how powerful recurring investing can look when an asset rises dramatically over time. But the deeper lesson is not just the return. It is the discipline required to continue through crashes, the importance of contribution size, and the need to decide how much Bitcoin belongs in the total portfolio.

If you are considering a high monthly Bitcoin contribution, do not copy the case study blindly. Simulate your own dates, amounts, and downside scenarios. Then decide whether the plan fits your budget, emergency fund, tax situation, custody process, and risk tolerance.

Educational content only. This article is not financial, tax, legal, or investment advice. Bitcoin is volatile and speculative. Backtests are based on historical assumptions and do not predict future returns.