Bitcoin DCA: 7 Powerful Lessons From Investing $100 Every Month Since 2015

A practical Bitcoin DCA guide for understanding what a simple $100/month plan teaches about volatility, timing risk, lump sum comparison, taxes, portfolio fit, and how to test your own scenario.

It spreads purchases across many prices instead of forcing one perfect entry date.

Bitcoin DCA can smooth entry, but it does not remove drawdowns, custody risk, or tax complexity.

The plan only works if the investor can keep following it during both euphoria and panic.

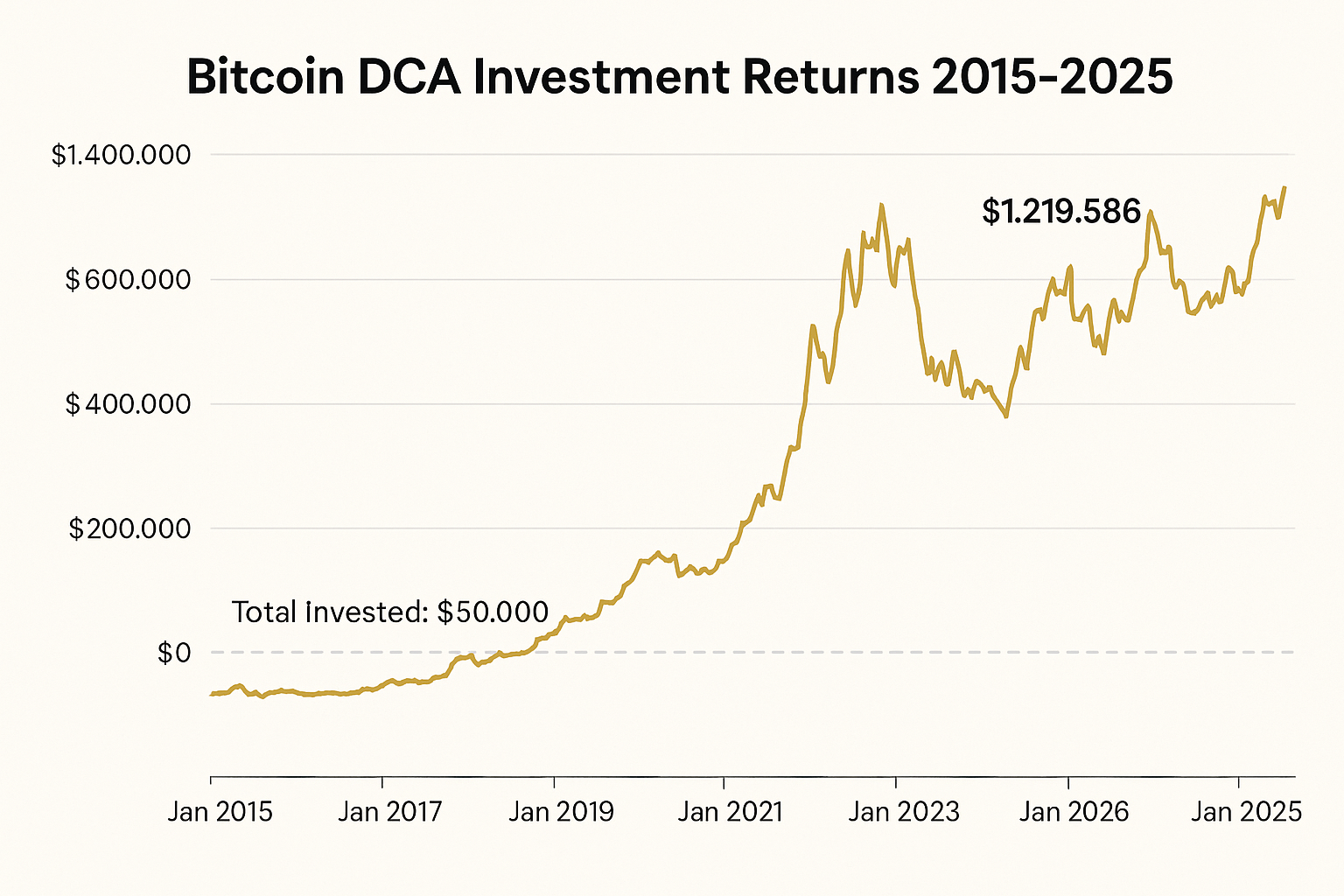

Quick Verdict: What a Bitcoin DCA Since 2015 Really Shows

A Bitcoin DCA plan since 2015 would have rewarded consistency, but the result should be studied as a behavior lesson, not a promise of future returns. The strategy would have bought through deep crashes, euphoric rallies, long periods of doubt, and several moments where stopping felt emotionally easier than continuing.

The most useful takeaway is simple: dollar-cost averaging can make a volatile asset easier to approach, but it does not make the asset safe. A Bitcoin DCA schedule manages entry timing. It does not manage position size, tax reporting, custody decisions, or the investor's ability to tolerate large drawdowns.

What Is Bitcoin DCA?

Bitcoin DCA means investing a fixed amount into Bitcoin on a recurring schedule, such as weekly or monthly, regardless of whether the price is high, low, exciting, or frightening. In this article, the example is $100 per month. The investor is not trying to guess the perfect bottom. The investor is following a rule.

This matters because Bitcoin trades 24/7 and can move sharply in both directions. Without a rule, investors can easily chase rallies, panic during crashes, or delay forever while waiting for the perfect entry. A recurring plan does not solve every problem, but it gives the investor a structure.

The original Bitcoin white paper explains the technical idea behind the network. It does not tell anyone whether Bitcoin is a good investment, but it is the most useful primary source for understanding what Bitcoin was designed to be. You can read the official Bitcoin white paper.

| Element | What it means | Why it matters |

|---|---|---|

| Fixed amount | The investor contributes the same dollar amount each period. | It makes the plan easier to automate and connect to a budget. |

| Recurring schedule | Purchases happen monthly, weekly, or another chosen rhythm. | It reduces the need to make a new emotional decision every time. |

| Volatile asset | Bitcoin can move sharply across cycles. | The strategy still requires risk tolerance and position sizing. |

| Long horizon | The investor studies outcomes across years, not days. | DCA is more meaningful when the holding period is long enough to include multiple regimes. |

Bitcoin DCA Simulation Setup

This case study uses a simple recurring investment rule: invest $100 into Bitcoin once per month, starting in 2015, and keep investing through the full period. Exact results depend on the purchase date each month, exchange data, trading fees, spreads, tax assumptions, and the current Bitcoin price.

The purpose is not to freeze one perfect final number. The purpose is to understand how recurring investing behaves across very different market conditions. That is why the setup is intentionally simple: it isolates the contribution habit and makes the tradeoff easier to see.

| Input | Assumption | Planning implication |

|---|---|---|

| Contribution | $100 per month | Accessible enough for a beginner or budget-based investor. |

| Asset | Bitcoin | High upside history, high volatility, and meaningful downside risk. |

| Start year | 2015 | Captures multiple cycles instead of only one bull market. |

| Frequency | Monthly | Easy to connect to income and savings rhythm. |

| Costs | Not included in the simplified explanation | Real investors should include fees, spreads, and taxes before making decisions. |

How the Bitcoin DCA Journey Changes by Market Phase

A long Bitcoin DCA plan does not feel the same in every period. The same $100 monthly contribution can feel exciting near new highs, foolish during crashes, boring in sideways markets, and obvious only after recovery. This is why a phase-by-phase view is more useful than one final dollar number.

The investor who started in 2015 did not know what would happen next. They had to keep buying while the story changed. That is what makes the case study useful. It reveals how a recurring plan behaves when confidence is unstable.

| Period | Investor experience | DCA effect | Lesson |

|---|---|---|---|

| 2015 to 2017 | Low prices followed by a major bull market. | Early contributions bought more Bitcoin per dollar. | Small recurring contributions can matter when made before adoption expands. |

| 2018 to 2020 | Crash, skepticism, and rebuilding. | DCA bought through lower prices and reduced entry-date regret. | The hardest months to keep investing can become important later. |

| 2021 to 2022 | New highs followed by a painful decline. | New purchases at higher prices faced drawdown. | DCA reduces timing pressure, but not market risk. |

| 2023 to 2025 | Recovery, infrastructure growth, and renewed attention. | Accumulated units benefited from recovery. | Consistency matters most when paired with a long horizon. |

The final result may look smooth in hindsight, but the lived experience would have been rough. That is why this article treats Bitcoin DCA as a rule-based strategy, not a magic formula.

7 Powerful Lessons From Investing $100/Month in Bitcoin

The seven lessons below are the heart of the article. They help turn the historical scenario into a usable decision framework.

1. The amount can be small, but the habit must be durable

A $100 monthly Bitcoin DCA is realistic for many readers, but the plan only works if it survives rent increases, job changes, market fear, and daily noise. A smaller plan that continues for years can be more useful than an aggressive plan that stops after one crash.

2. DCA reduces timing pressure, not risk

DCA spreads purchases across many prices. It can reduce regret if Bitcoin falls after you start. But the investor still owns Bitcoin, and Bitcoin can still decline sharply. Position sizing and risk limits remain necessary.

3. Bear market purchases are emotionally difficult

Buying during pessimism can feel pointless. Yet those lower-price purchases can shape the average cost. The investor needs a rule before the crash arrives, because emotions are unreliable during the crash.

4. Lump sum can win mathematically

If an asset rises strongly after the initial investment, lump sum can outperform. Bitcoin DCA may still be better behaviorally for investors who do not have a lump sum or cannot tolerate investing everything at once.

5. Fees and taxes quietly matter

A monthly Bitcoin plan creates many purchases. Spreads, trading fees, and tax lots should be tracked. A high-fee platform can reduce the effectiveness of small recurring contributions.

6. The plan needs a portfolio rule

If Bitcoin appreciates, it can become a larger share of net worth than intended. Decide whether you will let the allocation grow, rebalance, pause contributions, or cap exposure.

Bitcoin DCA vs Lump Sum: Which Approach Is Better?

The better method depends on the investor, timing, and emotional tolerance. If someone invested a lump sum near a major Bitcoin low, the result can look extraordinary. But that outcome is easier to admire after the fact than execute in real time. Most investors do not know when the major low is happening.

Bitcoin DCA is usually more practical for people investing from monthly income. It turns the decision into a habit. Instead of asking whether today is the perfect day to buy Bitcoin, the investor asks whether the recurring allocation still fits the broader plan.

| Approach | Best fit | Main risk |

|---|---|---|

| Bitcoin DCA | Investors using monthly income, beginners, and people who want less entry-date regret. | Can underperform lump sum in a strong rising market. |

| Lump sum | Investors with cash already allocated to risk assets and high drawdown tolerance. | Bad timing can create immediate large losses. |

| Hybrid | Investors who want some exposure now and some risk spreading over time. | Still requires a written schedule to avoid improvising. |

For a deeper strategic comparison, read DCA vs Lump Sum and test your own assumptions in the simulator.

Bitcoin DCA Risk Rules Before You Start

A strong historical Bitcoin DCA result can make the strategy look obvious. It was not obvious while it was happening. A recurring strategy should never be treated as a guarantee, and crypto exposure should be sized so the investor can survive large drawdowns without panic.

Rules to define first

- Maximum monthly contribution.

- Maximum Bitcoin allocation as a share of portfolio.

- Review frequency for rebalancing.

- Custody method and account security.

- Tax record keeping process.

Risks to respect

- Large market drawdowns.

- Exchange or custody problems.

- Regulatory and tax changes.

- Behavioral errors during volatility.

- Portfolio concentration after strong gains.

How Bitcoin DCA Fits Into a Broader Investment Plan

A Bitcoin DCA should not be evaluated in isolation. The same $100/month could be used for an emergency fund, debt repayment, a retirement account, broad-market ETFs, education savings, or a different investment. The right choice depends on the investor's goals and financial stability.

A useful framework is to separate financial foundation from growth experiments. The foundation includes emergency savings, high-interest debt management, insurance, and core long-term investing. Growth experiments are smaller allocations where the investor seeks upside and accepts higher volatility. For many people, Bitcoin belongs in the second category.

| Financial layer | Role | Bitcoin DCA implication |

|---|---|---|

| Emergency savings | Protects against short-term shocks. | Usually comes before high-volatility investing. |

| Core investing | Builds diversified long-term wealth. | Bitcoin should not automatically replace diversified exposure. |

| Satellite allocation | Adds higher-risk upside potential. | A Bitcoin DCA may fit here if sized carefully. |

| Scenario planning | Tests what happens under different assumptions. | Use tools before increasing contributions. |

If you are unsure whether there is room in your monthly budget for recurring investing, start with the WhatIfBudget Planner. Then test investment scenarios after identifying a sustainable surplus.

How to Choose a Monthly Bitcoin DCA Amount

The right Bitcoin DCA amount is not the biggest number that looks exciting in a backtest. It is the amount you can keep contributing without creating stress in your actual life. This is especially important with Bitcoin because volatility can make a plan feel easy during rallies and uncomfortable during drawdowns. If the contribution is too large, the investor may stop exactly when consistency matters most.

A practical method is to start from monthly cash flow. First cover essentials, minimum debt payments, emergency savings, and core investing. Then decide what portion of the remaining surplus can reasonably go toward a high-volatility satellite asset. This keeps the Bitcoin plan connected to the household budget rather than detached from it.

| Monthly surplus | Conservative test amount | Aggressive test amount | Planning note |

|---|---|---|---|

| $100 | $10 to $25 | $50 | Keep most surplus flexible until savings are stable. |

| $300 | $25 to $50 | $100 | A $100/month Bitcoin DCA may fit only if essentials are already covered. |

| $750 | $50 to $100 | $150 to $250 | Compare Bitcoin with ETFs, retirement contributions, and debt goals. |

| $1,500+ | $100 to $250 | Custom percentage | Use portfolio caps and rebalancing rules before scaling up. |

Tools to Test Your Own Bitcoin DCA Plan

This article uses $100/month because the number is easy to understand. Your real plan may be $25, $50, $250, or a percentage of income. Your start date, frequency, asset mix, and risk limits may be different.

The most useful workflow is to move from budget to simulation. First find the amount you can actually invest. Then test how that amount behaves historically. Finally, compare DCA with lump sum or multiple scenarios if the decision is serious.

Common Mistakes When Copying a Bitcoin DCA Case Study

Historical case studies are powerful, but they can also create false confidence. The investor who started in 2015 did not know the future. A reader today has hindsight, but not certainty. The goal is to learn the discipline, not blindly copy the result.

- Assuming the same return will repeat: Bitcoin is larger and more mature than it was in 2015. Future returns may be lower, higher, or completely different.

- Ignoring drawdowns: a high final value does not remove the emotional pain of large losses along the way.

- Using money needed soon: volatile assets are poorly suited for short-term obligations.

- Skipping tax records: many small purchases create many tax lots.

- Letting the allocation grow without a rule: strong gains can change the portfolio risk profile.

- Confusing DCA with diversification: buying the same asset every month is still exposure to one asset.

Bottom Line

A Bitcoin DCA plan since 2015 is a powerful case study because it shows how a modest recurring habit can create meaningful exposure over time. But the strategy is not a shortcut around risk. It requires position sizing, patience, clean records, custody awareness, and the ability to keep following the rule when the market feels uncomfortable.

For beginners, the best conclusion is not "put everything into Bitcoin." The better conclusion is that recurring investing can be effective when it is connected to a realistic budget, a long horizon, and a clear risk rule. Test your own version before making the plan larger.

Frequently Asked Questions

Is Bitcoin DCA a good strategy for beginners?

Bitcoin DCA can be beginner-friendly because it turns investing into a repeatable rule, but Bitcoin itself is still highly volatile. Beginners should use a contribution amount they can afford, understand custody and tax basics, and avoid treating historical returns as a guarantee.

How much would $100/month in Bitcoin since 2015 be worth?

The exact value depends on the purchase date each month, exchange prices, fees, taxes, and the current Bitcoin price. The more important lesson is that steady monthly investing would have accumulated Bitcoin across several major cycles instead of relying on one perfect entry point.

Does Bitcoin DCA always beat lump sum investing?

No. Lump sum investing can outperform when the asset rises strongly after the initial investment. Bitcoin DCA is usually more useful for reducing timing regret, spreading entry prices, and helping investors stay disciplined when they invest from monthly income.

What is the best Bitcoin DCA frequency?

Monthly DCA is easy to connect to a budget, weekly DCA smooths purchases a little more, and daily DCA creates many small transactions. The best frequency is usually the one you can automate with low fees and clean record keeping.

Should I put all of my savings into a Bitcoin DCA plan?

Usually no. Bitcoin is a high-volatility asset. Many investors treat it as a smaller satellite allocation inside a broader plan that includes emergency savings, debt management, retirement investing, and diversified assets.

Can I use a Bitcoin DCA strategy with ETFs or stocks?

Yes. Dollar cost averaging can be used with ETFs, stocks, crypto, and other assets. The behavior is different depending on volatility, expected return, and risk. Use the Investment Simulator to compare assets before deciding.

Do fees matter for a $100 monthly Bitcoin DCA?

Yes. Small recurring purchases can be hurt by high fixed fees or wide spreads. Investors should compare platforms, understand transaction costs, and keep records for tax reporting.

What should I do after reading this Bitcoin DCA case study?

Run your own scenario. Test different contribution amounts, start dates, frequencies, and comparison assets. Then decide whether the plan fits your budget, risk tolerance, and broader investment strategy.