Lump Sum vs DCA: Which Investment Strategy Should You Use?

Compare investing everything at once with spreading your money over time. Learn when lump sum tends to have the edge, when dollar-cost averaging can be easier to stick with, and how to test both strategies with historical market data.

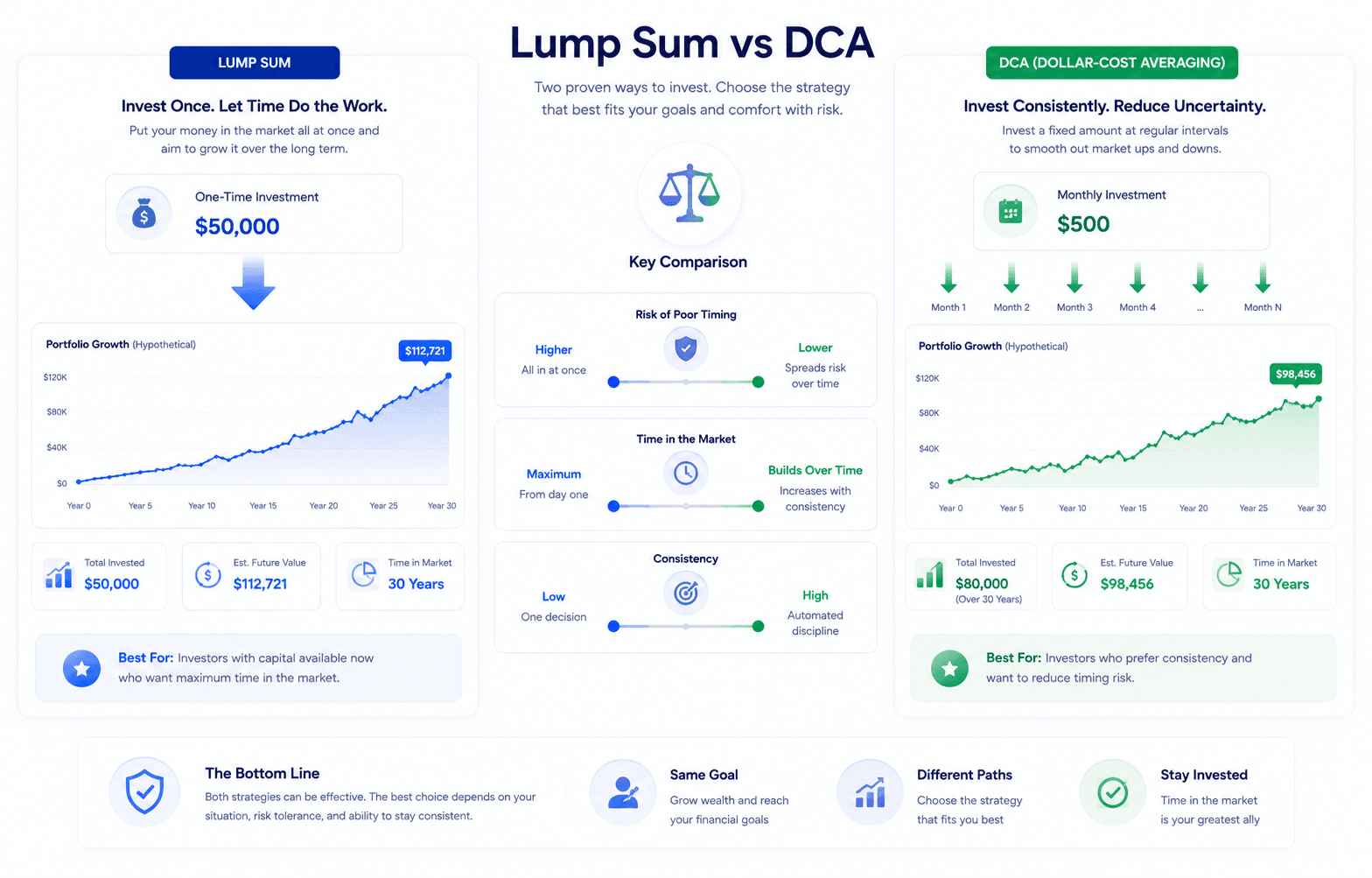

What do lump sum investing and DCA mean?

Lump sum investing means investing your available money immediately. If you receive a bonus, inheritance, tax refund, or cash from selling another asset, you put the full amount into the market at once.

Dollar-cost averaging, often shortened to DCA, means dividing that money into scheduled purchases. Instead of investing $12,000 today, you might invest $1,000 per month for 12 months.

Lump sum investing

Maximizes time in the market. It can benefit more when prices rise soon after you invest, but it exposes the full amount to an immediate drawdown if the market falls.

Dollar-cost averaging

Spreads entry points across time. It can reduce emotional pressure and soften the impact of buying right before a decline, but some cash may sit out during rising markets.

Lump Sum vs DCA comparison table

The better choice depends on market direction, time horizon, risk tolerance, and investor behavior. The table below separates return logic from emotional and practical considerations.

| Factor | Lump Sum | DCA | What it means |

|---|---|---|---|

| Market exposure | Full exposure immediately | Gradual exposure over time | Lump sum benefits more from early gains; DCA reduces immediate timing risk. |

| Behavioral comfort | Can feel stressful after a large purchase | Usually easier emotionally | DCA may help investors avoid panic after short-term losses. |

| Best environment | Rising or undervalued markets | Volatile, uncertain, or overextended markets | Market regime matters more than the label of the strategy. |

| Cash drag | Low, because cash is invested | Higher, because cash waits on the sidelines | DCA can underperform if markets rise during the entry period. |

| Transaction count | One main purchase | Multiple purchases | DCA may create more transactions, tax lots, and fees depending on the platform. |

| Beginner friendliness | Simple, but psychologically harder | Simple and habit-forming | DCA often works well for people building discipline. |

When lump sum investing tends to work better

Lump sum investing tends to perform well when the market rises during the period when DCA would still be waiting to invest. Because markets have historically trended upward over long periods, getting money invested earlier can be powerful.

You have a long time horizon

If your investment horizon is measured in decades, short-term entry timing matters less than staying invested through multiple cycles.

You have high conviction

If your asset allocation is already chosen and you accept volatility, lump sum avoids unnecessary delay.

Cash is losing value

Holding cash too long can create opportunity cost, especially when inflation or rising markets reduce the value of waiting.

The main risk is psychological. If a large lump sum investment drops shortly after you buy, you need enough conviction to avoid selling emotionally. The strategy can be mathematically sound and still fail if it causes behavior you cannot maintain.

When DCA can be the better practical strategy

DCA is not only about maximizing return. It is also about reducing timing regret, building habits, and making investing easier to continue when markets feel uncertain.

You feel uncertain

If investing the full amount today would make you anxious, DCA can make the plan easier to follow.

The market is volatile

Gradual entries can reduce the pain of buying immediately before a sharp decline.

You invest from income

Most people naturally DCA through paychecks, retirement contributions, and monthly investing plans.

DCA can underperform in strong bull markets because part of the money remains uninvested while prices rise. But if DCA keeps you consistent and prevents panic, it may produce better real-world outcomes than a theoretically superior plan you abandon.

A simple decision framework

Instead of asking which strategy is always better, ask which strategy is better for your situation. The strongest plan is the one you can execute through volatility.

| Your situation | Strategy to consider | Why |

|---|---|---|

| You have a long horizon and high risk tolerance | Lump sum | More time in the market may matter more than short-term entry timing. |

| You are nervous about investing all at once | DCA | A gradual plan may help you stay invested instead of freezing or selling. |

| You think markets are overextended | DCA or hybrid | Spreading purchases can reduce the damage of a poor starting point. |

| You received a windfall but want balance | Hybrid | Invest part now and DCA the rest over several months. |

| You invest monthly from salary | DCA | Your cash flow already supports recurring investing naturally. |

Example scenarios to test

The best way to understand the tradeoff is to test both strategies across different assets and start dates. These are useful scenarios to run in the Investment Simulator.

Strong bull market

Test whether lump sum benefits from immediate exposure when prices climb soon after the start date.

Market crash before recovery

Test whether DCA buys more units during the decline and recovers with less regret.

Sideways market

Test whether gradual purchases help smooth entry prices when markets chop around for months.

Use the right WhatIfInvested tool

This page explains the strategy. The tools help you test the numbers, compare realistic assumptions, and turn the decision into a repeatable workflow.

Costs, taxes, and account placement

Strategy comparisons often focus only on final value, but real investors also need to think about transaction costs, bid-ask spreads, taxes, and account type. These details rarely change the core idea, but they can change which strategy feels easier to manage.

Transaction costs

Lump sum usually creates fewer trades. DCA creates more transactions, which may matter if your broker charges commissions or if you buy assets with wider spreads.

Tax lots

DCA creates multiple purchase dates and cost bases. That can be useful for tracking, but it can also add recordkeeping work in taxable accounts.

Registered accounts

For Canadian investors, TFSA, RRSP, and FHSA choices may matter as much as timing. Account placement can affect taxation and withdrawal flexibility.

If you are investing inside a registered account, compare strategy timing with account strategy. A lump sum into the wrong account may be less useful than a consistent DCA plan into the account that fits your tax situation. For deeper account planning, read TFSA vs RRSP vs FHSA.

Common mistakes when comparing Lump Sum and DCA

The biggest mistakes are usually not mathematical. They come from using unrealistic assumptions or choosing a strategy that does not match your behavior.

Comparing different investment amounts

A fair comparison must use the same total amount. If lump sum invests $12,000 today, the DCA scenario should also deploy $12,000 over the selected schedule.

Ignoring cash drag

DCA leaves some cash uninvested. If markets rise while cash waits, that delay can reduce returns. The waiting cash should be part of the analysis.

Choosing too long of a DCA window

Spreading entries over several years may reduce anxiety, but it can also turn an investment decision into prolonged market timing.

Ignoring your own behavior

A plan that causes panic selling is not a good plan. If DCA keeps you invested, it may be better for your real outcome even if lump sum has stronger expected returns.

Want a more advanced comparison?

The free tools are useful for simple decisions. Premium is designed for investors who want to compare multiple portfolios, apply fees, export reports, save scenarios, and analyze a strategy in more detail.

Free simulator

Best for quick historical DCA vs lump sum backtests.

Premium DCA

Best for weighted portfolios, rebalancing, fees, exports, and deeper scenario work.

Pricing

Compare plans and unlock Premium tools when you need advanced analysis.

Frequently asked questions

Is lump sum better than DCA?

Not always. Lump sum often has higher expected returns when markets rise because the full amount is invested earlier. DCA can be better for behavior, regret control, and volatile entry periods.

How long should I DCA?

Many investors use 3, 6, or 12 months. Shorter periods reduce cash drag. Longer periods reduce timing anxiety but may miss gains if markets rise.

Can I combine lump sum and DCA?

Yes. A hybrid approach is often practical: invest part immediately and spread the rest over time. This balances market exposure with emotional comfort.

Is DCA the same as monthly investing?

Monthly investing from income is a form of DCA. The main difference is that windfall DCA is a choice to spread existing cash, while paycheck investing happens naturally as income arrives.

Which tool should I use?

Use the Investment Simulator to compare historical lump sum and DCA scenarios. Use the DCA Calculator for a focused recurring-investment projection.

Bottom line

Lump sum is usually the more aggressive strategy because it maximizes time in the market. DCA is usually the more comfortable strategy because it reduces the pressure of choosing the perfect entry point. For many investors, the best answer is not purely mathematical. It is the strategy they can follow consistently.

Educational simulation only. Historical performance does not guarantee future results. This page is not financial advice.