DCA vs Lump Sum: Which Investment Strategy Wins?

The honest answer is not simply “lump sum wins” or “DCA is safer.” The better answer depends on your cash source, investing horizon, emotional tolerance, market risk, and whether you can stay invested when the first months feel uncomfortable.

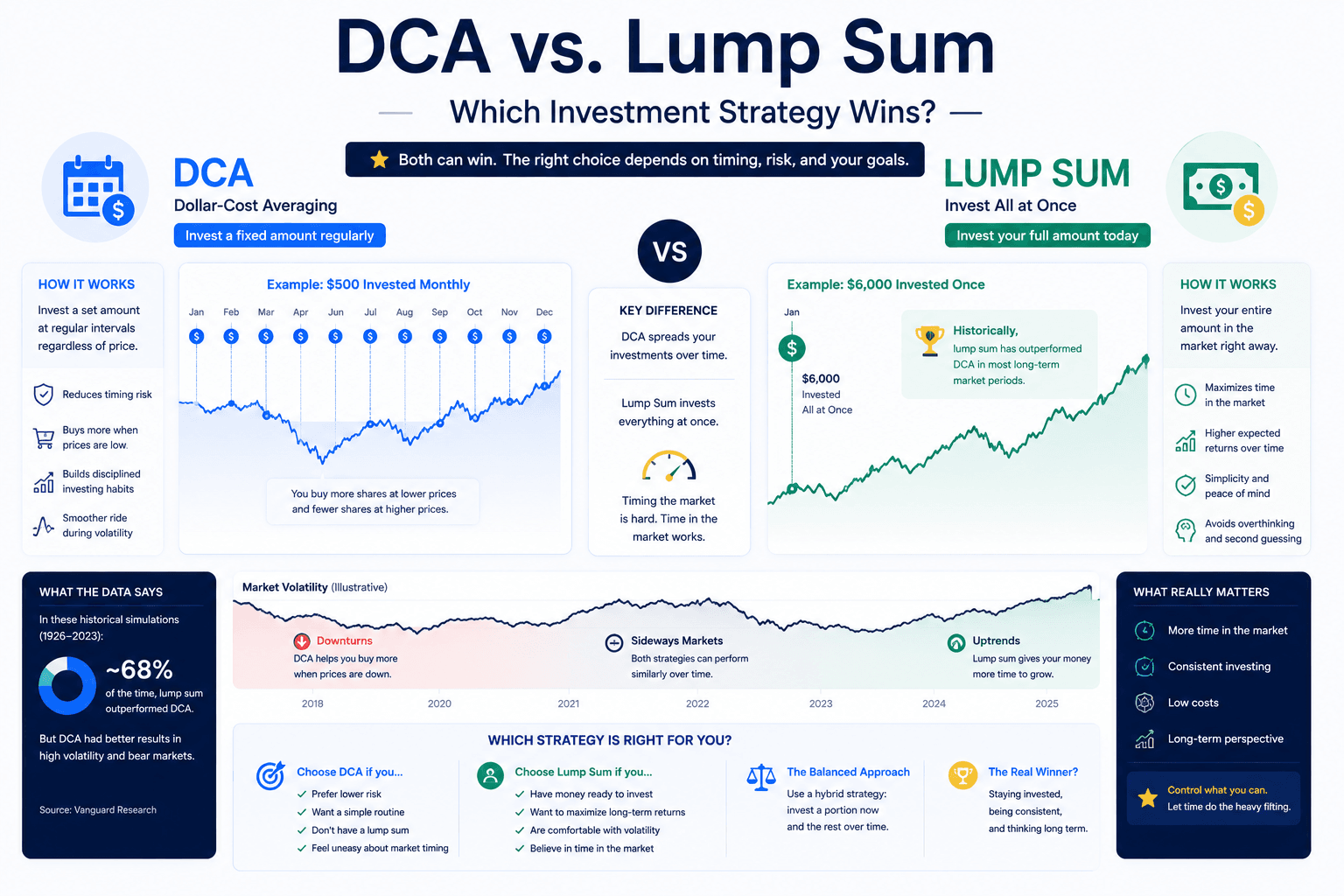

Quick answer: lump sum usually wins on expected return, but DCA often wins on execution

If you already have cash available and your goal is to maximize expected long-term returns, lump sum investing usually has the mathematical advantage because your money is exposed to the market sooner. That is especially true in markets with a positive long-term return expectation, such as broad stock indexes over long periods.

But investing is not only math. Dollar-cost averaging, or DCA, can be the better real-world strategy when the alternative is hesitation, panic, endless market timing, or abandoning the plan after an early drawdown. The strategy that looks best in a spreadsheet can fail if the investor cannot emotionally hold it.

You have cash now and a long horizon

Best for investors who can tolerate short-term losses and want maximum time in the market.

You need a smoother entry

Best when regret risk, volatility fear, or uncertainty would otherwise keep you uninvested.

You want exposure and comfort

Invest part now, then schedule the rest over several months with a clear rule.

The cleanest decision rule: if the money is already available and the horizon is long, invest a meaningful portion immediately. If the amount feels emotionally large, use a hybrid plan instead of waiting for the “perfect” entry point.

What DCA and lump sum investing actually mean

The DCA vs lump sum debate is often confusing because people use the terms in two different ways. Sometimes DCA means investing part of a windfall over time. Other times it simply means investing from every paycheck. Those are related, but they are not the same decision.

Investing gradually

DCA means investing a fixed amount at regular intervals, such as $500 every month. If prices fall, the same contribution buys more shares. If prices rise, it buys fewer shares. The goal is consistency, not perfect timing.

Investing immediately

Lump sum investing means putting available capital into the market right away. If you receive $20,000 and invest it today, you give the full amount more time to compound.

For normal workers investing from salary, DCA is often not a “strategy choice” at all. It is simply the natural result of receiving income monthly or biweekly. The real choice appears when you already have a sum of cash: a bonus, inheritance, home sale proceeds, business distribution, or cash sitting on the sidelines.

That is where this article focuses: should you invest all available cash now, spread it across time, or use a hybrid?

When each strategy tends to win

Both strategies can be intelligent. The mistake is treating one as universally superior. A strong investing plan considers the market math and the investor’s behavior at the same time.

| Situation | Likely Better Fit | Why | What to watch |

|---|---|---|---|

| Large cash amount, long horizon, high discipline | Lump sum | More money compounds sooner. | Short-term drawdown risk immediately after investing. |

| New investor with high anxiety | DCA | Gradual entry lowers regret and makes the process easier to follow. | Can underperform if markets rise while cash waits. |

| Markets feel expensive but you cannot predict a correction | Hybrid | Gets invested now while reserving part of the cash for scheduled entry. | Must follow the schedule instead of endlessly delaying. |

| Paycheck-based investing | DCA | Automatic recurring contributions match how income arrives. | Increase contributions as income rises instead of waiting. |

| Short horizon or uncertain cash need | Neither blindly | Money needed soon should not be forced into volatile assets. | Liquidity, emergency fund, and risk capacity matter first. |

The math: why lump sum often has the edge

The mathematical case for lump sum investing is straightforward: if markets tend to rise over time, having more dollars invested earlier gives those dollars more time to participate. DCA keeps some cash on the sidelines, which reduces immediate risk but also reduces immediate exposure.

Research from major investment firms generally points in the same direction. Vanguard’s research on cost averaging argues that, when investors already have a lump sum available, investing sooner has historically beaten many staged-entry approaches more often than not. Charles Schwab also frames the issue around the cost of waiting and notes that investing promptly has tended to beat delayed strategies over long horizons. Morgan Stanley has published analysis showing lump sum investing produced slightly higher annualized returns than DCA in more than half of historical seven-year periods.

Those conclusions do not mean lump sum wins every time. They mean lump sum has the expected-return advantage when the market’s long-term return expectation is positive. DCA can still win in specific periods, especially if the market falls after the first investment date.

Earlier exposure

If the market rises, waiting cash misses gains. The opportunity cost becomes visible quickly in strong bull markets.

Better entry during declines

If prices fall while you are averaging in, later purchases occur at lower prices and may improve your average cost.

Staying invested

The best theoretical result is useless if the strategy causes panic selling or permanent hesitation.

For a deeper historical angle, compare this article with DCA vs Lump Sum: Which Strategy Wins Over Time?. That article focuses more directly on long-run historical outcomes, while this guide focuses on the decision framework.

Risk, regret, and the real reason investors choose DCA

The reason DCA remains popular is not because it always maximizes return. It is because it solves a human problem. Investing a large amount today and watching it drop 12% next month feels painful, even if the strategy is rational over a 10-year horizon.

DCA transforms one large emotional decision into a series of smaller operational decisions. Instead of asking “Is today the perfect day to invest everything?” you ask “Is my scheduled plan still running?” That can be a powerful advantage for investors who know they are sensitive to regret.

Regret risk is not imaginary. Many investors who intend to invest a lump sum end up waiting for a dip. Then the market rises. They wait for a pullback. The pullback comes, but they fear it will get worse. They wait again. Months or years can pass while the cash quietly loses purchasing power to inflation.

DCA is not a magic return enhancer. It is a behavior-management tool. It can reduce timing regret, but it can also reduce expected return if markets rise while cash remains uninvested.

The more honest question is not “Which strategy is best in a backtest?” It is “Which strategy will I actually execute without sabotaging myself?”

Investor scenarios: which one sounds like you?

The same strategy can be right for one investor and wrong for another. Below are practical examples to make the choice more concrete.

You received a bonus

You have $10,000 available, no urgent cash need, and a 15-year horizon. Lump sum or a mostly lump-sum hybrid often makes sense. Example: invest 70% now and DCA the remaining 30% over six months.

You are just starting

You can invest $250 each month from your paycheck. DCA is natural here. The key is automation, not deciding every month whether the market is attractive.

You are worried about a crash

If investing everything today would make you check your account daily, use a written DCA schedule. A slightly lower expected return may be worth it if it keeps you invested.

Example: $12,000 available today

Imagine you have $12,000 to invest. A lump sum strategy puts all $12,000 into the market immediately. A 12-month DCA strategy invests $1,000 each month. A hybrid might invest $8,000 now and $1,000 per month for the next four months.

If the market rises steadily, lump sum likely wins because all $12,000 participated from the beginning. If the market falls sharply in the first few months, DCA may look better because later contributions buy at lower prices. If the market moves sideways, the difference may be modest, and the most important factor becomes whether you actually followed the plan.

Three practical examples: how the same money can lead to different decisions

Examples make the decision clearer because they separate the theoretical strategy from the real-life investor. The same $25,000 can be handled differently depending on who owns it and what job that money needs to do.

Example 1: the long-horizon investor

A 32-year-old investor receives a $25,000 work bonus. They already have an emergency fund, no short-term need for the money, and a 20-year horizon. In this case, the strongest default is usually lump sum or a return-tilted hybrid. The investor could invest the full amount into a diversified ETF portfolio immediately, or invest 80% now and the remaining 20% over three months. The reason is simple: a long horizon gives the portfolio time to recover from normal volatility, and the investor does not need the cash soon.

Example 2: the anxious new investor

A new investor receives the same $25,000, but they have never invested during a market decline. They know they would feel awful if the market fell immediately after investing. For this person, a pure lump sum may be mathematically attractive but behaviorally fragile. A balanced hybrid, such as 50% now and the rest over six months, may be a better plan. It reduces the risk of never starting while making the first drawdown easier to tolerate.

Example 3: the near-retirement investor

A 61-year-old investor receives $25,000 and expects to retire in four years. Their portfolio already has meaningful market exposure, and they may need part of the money for planned expenses. Here the DCA vs lump sum question should not be answered in isolation. The first question is asset allocation. Some of the money may belong in cash or short-term bonds. The portion intended for long-term growth could be invested gradually or with a modest lump sum, but the investor should not treat retirement spending money the same way a 30-year-old treats growth capital.

The point: the best investment strategy is not only a market forecast. It is a match between the money, the timeline, the investor, and the consequences of being wrong.

The hybrid strategy: a practical compromise for real people

Many investors do not need a pure answer. A hybrid strategy can preserve much of the expected-return advantage of lump sum while reducing the emotional shock of investing everything at once.

A common hybrid structure is:

- Invest 50% to 80% of the available cash immediately.

- Invest the remaining amount over 3 to 12 months.

- Set dates in advance and follow them automatically.

- Avoid changing the plan based on headlines.

The hybrid approach is especially useful when the cash amount is large relative to your net worth. Investing $5,000 may feel easy. Investing $100,000 may feel completely different. The decision should respect both math and emotional capacity.

| Hybrid style | Example | Best for |

|---|---|---|

| Conservative hybrid | 40% now, 60% over 12 months | Very nervous investors or unusually large cash events. |

| Balanced hybrid | 60% now, 40% over 6 months | Investors who want exposure but still want emotional protection. |

| Return-tilted hybrid | 80% now, 20% over 3 months | Long-horizon investors who mostly accept the lump sum logic. |

DCA vs lump sum across different market regimes

One reason the DCA vs lump sum debate never disappears is that each strategy feels brilliant in one market regime and frustrating in another. If you only look at a single period, the conclusion can become misleading. The market environment at the start date matters a lot, especially over shorter horizons.

In a strong bull market, lump sum usually looks obvious in hindsight. The investor who deployed capital early captured the rise immediately. DCA investors kept buying, but part of their capital waited in cash while prices climbed. This is where DCA can feel too conservative.

In a sharp bear market, the opposite can happen. A lump sum investor may experience a large immediate drawdown. A DCA investor gradually buys lower prices, which may reduce regret and improve the average entry price. This does not eliminate risk, but it can make the path easier to hold.

In sideways markets, the answer is often less dramatic. Lump sum may still benefit from dividends and small movements, while DCA may benefit from volatility. The difference can be smaller than investors expect, which means behavior, fees, and simplicity become more important.

| Market regime | What lump sum feels like | What DCA feels like | Practical lesson |

|---|---|---|---|

| Fast bull market | Rewarding because capital participates immediately. | Frustrating because later purchases happen at higher prices. | Waiting has an opportunity cost. |

| Early bear market | Painful because the full position declines quickly. | Comforting because new purchases occur at lower prices. | Risk tolerance matters as much as expected return. |

| Sideways market | Acceptable if dividends and patience matter. | Acceptable if volatility creates lower entry points. | Execution discipline can matter more than the entry method. |

| Highly volatile crypto cycle | Can produce spectacular gains or brutal early losses. | Can smooth the entry path but still exposes investors to deep drawdowns. | Position sizing matters more than the DCA label. |

This is why a single backtest cannot answer every investor’s question. A backtest is a learning tool. It should help you understand ranges of outcomes, not convince you that one strategy is always perfect. If you want to compare specific assets and dates, use the Investment Simulator and test your own start date rather than relying on one generic chart.

DCA into ETFs, stocks, and crypto: the asset matters

DCA and lump sum do not behave identically across all assets. A broad diversified ETF, a single stock, and Bitcoin have different volatility profiles, different return drivers, and different emotional demands. The higher the volatility and uncertainty, the more valuable DCA can feel psychologically.

Broad index ETFs

For broad index ETFs, lump sum often has a strong case when the horizon is long. Diversification reduces company-specific risk, and the long-term expected return is usually positive. That does not mean the first year will be smooth, but the core logic of early exposure is easier to defend with diversified assets than with a speculative single position.

Individual stocks

With individual stocks, the choice becomes more complex. A stock can permanently underperform because of business deterioration, valuation compression, competition, regulation, or management mistakes. DCA can reduce entry timing risk, but it cannot fix a weak investment thesis. If you are averaging into a single stock, you need a clear reason beyond “the price is down.”

Crypto assets

With crypto, DCA often plays a different role. It helps investors avoid placing a large amount at a cycle peak, and it creates a rule-based way to participate in a highly volatile asset. But the risk remains high. DCA into a volatile asset is still volatile investing. The contribution schedule does not make the asset safer; it only changes the entry path.

Important distinction: DCA manages timing risk. It does not replace diversification, valuation discipline, emergency savings, or position sizing.

How to implement the strategy without overthinking it

The biggest advantage of a written investment rule is that it turns an emotional decision into an operational process. Once the rule exists, the job is no longer to forecast headlines. The job is to execute the plan you already chose.

For lump sum investing, implementation is simple but emotionally demanding. Choose the allocation, confirm the cash is not needed for short-term obligations, invest, and avoid judging the decision after only a few weeks. A bad first month does not automatically mean the decision was wrong. It only means markets are volatile.

For DCA, implementation requires more structure. Decide the amount, frequency, end date, asset allocation, and what happens if markets rise or fall. If you do not define these details, DCA can become disguised procrastination. You may tell yourself you are being disciplined while constantly delaying the next purchase.

Specific and automatic

“Invest $1,000 on the first Monday of each month for 12 months into a diversified ETF portfolio.” This is clear, measurable, and easy to follow.

Flexible in the wrong way

“I will invest when the market looks better.” This is not DCA. It is market timing with no accountability.

Write your rule before investing

Your rule should answer four questions: how much, how often, into what, and when the plan ends. If you are using a hybrid approach, write the immediate investment percentage and the schedule for the remaining cash. The more precise the rule, the less room you leave for emotional improvisation.

Automate what you can

Automation is one of the strongest tools for recurring investing. Scheduled deposits, recurring ETF purchases where available, calendar reminders, and written allocation targets all reduce friction. If you have to manually decide every month, you are creating twelve chances per year to second-guess the plan.

Review, but do not constantly redesign

Reviewing your plan quarterly or semi-annually is reasonable. Redesigning it every time the market moves is usually harmful. A good DCA or lump sum plan should survive normal volatility. If every dip forces a new strategy, the issue is not the strategy; it is the lack of a stable investment policy.

How this choice connects to retirement investing

Retirement investing adds another layer to the DCA vs lump sum decision. Most retirement savers naturally use DCA because contributions come from paychecks. They invest every two weeks or every month for decades. In that context, DCA is not a temporary entry strategy; it is the structure of the accumulation phase.

But lump sum decisions still appear in retirement planning. You might roll over an old retirement account, receive a bonus, sell a business, inherit money, or move cash from a savings account into a long-term portfolio. When that happens, the same framework applies: horizon, risk tolerance, cash need, tax account, and emotional capacity.

For a younger investor with decades before retirement, delaying investment for too long can be expensive. For someone near retirement, sequence-of-return risk becomes more important. A large lump sum invested just before withdrawals begin may create more stress than the same investment made by a 30-year-old. Age does not decide the strategy by itself, but it changes the risk context.

If your goal is retirement planning, pair this article with How to Simulate a Retirement Plan with DCA. That guide focuses more directly on long-term contribution plans and retirement-style scenarios.

Common mistakes in the DCA vs lump sum decision

The strategy choice is important, but most damage comes from avoidable mistakes around execution. The following errors appear again and again.

Confusing DCA with waiting

DCA has a schedule. Waiting has excuses. If there is no amount, interval, and end date, the plan is not truly dollar-cost averaging.

Judging too quickly

A strategy can look bad after three months and still be reasonable over ten years. Short-term outcomes are noisy.

Ignoring cash needs

Do not invest emergency funds or near-term spending money just because lump sum has a higher expected return.

Over-optimizing frequency

Daily, weekly, and monthly schedules can produce different paths, but the bigger decision is whether you invest consistently at all.

Another mistake is letting the strategy become your identity. Some investors defend lump sum because it sounds more rational. Others defend DCA because it feels safer. A strong investor can use either method when the situation calls for it.

What external research suggests

Research on lump sum vs dollar-cost averaging usually reaches a balanced conclusion: investing sooner often improves expected return, but DCA can help manage regret and behavior. This is why high-quality guidance rarely says “always do one thing.” It usually explains the tradeoff.

Vanguard’s research on cost averaging emphasizes that staged investing often means taking market risk later. In other words, DCA can feel safer because some cash remains out of the market, but that safety comes with a potential opportunity cost. If markets rise while cash waits, the staged investor may trail the lump sum investor.

Charles Schwab’s investor education makes a similar point from a practical angle: waiting for the perfect moment is difficult, and investing promptly has historically been hard to beat over long periods. Schwab also recognizes that DCA can be useful when the investor is prone to regret after a large investment drops in value.

Morgan Stanley’s published analysis is also useful because it avoids absolutism. Their review of many historical periods found lump sum generated slightly higher annualized returns in more than half of cases, but not all cases. That is exactly the nuance investors need: the expected-return edge is real, but the outcome is not guaranteed in every time window.

| Source | Useful takeaway | How to apply it |

|---|---|---|

| Vanguard research | Cost averaging often delays market risk rather than removing it. | Use DCA intentionally, not as a permanent way to avoid decisions. |

| Charles Schwab | DCA can help investors who are vulnerable to timing regret. | Use DCA when it improves follow-through and prevents panic. |

| Morgan Stanley | Lump sum has often produced higher annualized returns, but not universally. | Respect the probability edge without pretending outcomes are certain. |

For WhatIfInvested readers, the practical conclusion is this: use research to understand the baseline odds, then use your own simulation to understand your chosen asset, start date, contribution schedule, and downside risk. Evidence gives direction. Your plan gives execution.

That is why this article treats DCA vs lump sum as a planning decision rather than a slogan. A useful answer should help you act today, stay consistent next month, and avoid rewriting the strategy every time the market moves.

Test the decision with your own numbers

The best DCA vs lump sum answer is personal. Your starting amount, monthly contribution, asset choice, date range, fees, and risk tolerance can change the conclusion.

Investment Simulator

Backtest DCA and lump sum scenarios with historical data and compare outcomes.

DCA Calculator

Model recurring contributions, compounding, and future portfolio growth.

Premium DCA

Compare multiple portfolios, fees, rebalancing, withdrawals, saved scenarios, and exports.

Fees, taxes, and cash drag can change the result

A clean DCA vs lump sum comparison assumes low fees and a simple taxable situation. Real investors may face commissions, bid-ask spreads, management fees, currency conversion costs, and taxes. These details matter more when the expected difference between strategies is small.

If every trade has a fixed fee, very frequent DCA can become inefficient. Monthly investing may be reasonable; daily investing may be unnecessary. If you invest through low-cost ETFs with no commission, the friction is much lower.

Taxes also matter. In registered accounts such as a TFSA, RRSP, IRA, or 401(k), tax friction may be reduced or deferred depending on your country and account type. In taxable accounts, rebalancing and selling can trigger consequences. This is one reason a written plan matters: it reduces unnecessary tinkering.

Cash drag is another hidden cost. Money waiting in cash may earn interest, but it may still trail long-term equity returns. If you DCA slowly over 24 months, you are not only reducing timing risk; you are also choosing to delay risk exposure for a long period. That may be appropriate, but it should be intentional.

Decision checklist before you choose

Before choosing DCA or lump sum, answer these questions honestly. The right strategy usually becomes obvious once the constraints are clear.

- Is the money already available? If yes, lump sum or hybrid is a real choice. If no, paycheck-based DCA is natural.

- What is the time horizon? Longer horizons generally support earlier market exposure.

- How large is the cash amount relative to your net worth? The larger it feels, the more useful a hybrid plan may be.

- Would a 20% early drop make you sell? If yes, pure lump sum may be emotionally unrealistic.

- Are fees low enough for repeated purchases? If not, use fewer scheduled purchases.

- Do you have an emergency fund? Do not force short-term safety money into a volatile investing strategy.

- Will you automate the plan? Automation reduces second-guessing and improves follow-through.

Related guides and tools

Use these resources to deepen the decision without mixing up the intent of each page.

Which wins over time?

Use this when you want the long-run historical comparison between DCA and lump sum.

When one clearly wins

Use this when you want examples where the market environment strongly favors one strategy.

Strategy comparison page

Use this page to connect the concept with the free simulator and Premium workflow.

For broader planning, pair this guide with WhatIfBudget to identify investable monthly cash flow, then use the DCA Calculator to model recurring contributions.

Frequently asked questions

Is DCA better than lump sum investing?

Not usually on expected return when the cash is already available and the investment horizon is long. Lump sum often has the mathematical edge because money enters the market sooner. DCA can be better for investors who need emotional discipline or who would otherwise delay investing.

When does DCA beat lump sum?

DCA tends to look better when markets fall after the first investment date. In that case, later scheduled purchases buy at lower prices. DCA can also “win” behaviorally if it prevents panic selling or helps a hesitant investor begin.

Should beginners use DCA?

Many beginners benefit from DCA because it is simple, automatic, and emotionally easier. If a beginner receives a large windfall, a hybrid plan may be a better compromise than either investing everything immediately or waiting indefinitely.

How long should a DCA schedule last?

For a lump sum that you are intentionally averaging into the market, common schedules range from three to twelve months. Longer schedules reduce entry risk but increase cash drag. The best schedule is one you can follow without constantly changing it.

Can I combine DCA and lump sum?

Yes. A hybrid approach is often practical. For example, invest 60% immediately and DCA the remaining 40% over six months. This keeps you exposed while reducing the emotional pressure of a single entry point.

Does DCA guarantee profit?

No. DCA does not guarantee profits or protect against losses. It only spreads entry points over time. The underlying asset can still fall, and investors still need diversification, risk controls, and an appropriate time horizon.

Educational simulation only. Historical performance does not guarantee future results. This article is for educational purposes and is not personal financial advice.