Retirement DCA Simulation: How to Model Monthly Investing for Retirement

A retirement DCA simulation helps you turn a vague retirement goal into a testable contribution plan. Instead of guessing whether monthly investing is enough, you can compare scenarios, stress test assumptions, and see how DCA, inflation, fees, withdrawals, and market timing can shape your future retirement range.

Quick answer: how a retirement DCA simulation should work

A retirement DCA simulation should start with your current portfolio balance, monthly contribution, expected retirement age, time horizon, return assumptions, inflation estimate, fees, tax context, and future withdrawal needs. Then it should compare several paths instead of pretending that one projection is the future. A useful model answers three practical questions: how much you might accumulate, how sensitive the result is to assumptions, and whether the plan can survive weaker returns or a bad market near retirement.

The most important point is that DCA is not only a return strategy. It is a behavior system. It turns retirement investing into a repeatable process: contribute, stay invested, review periodically, and increase the contribution when cash flow improves. Over a 20, 30, or 40 year period, this habit can matter more than finding a perfect entry price.

A retirement DCA simulation is strongest when it separates accumulation from retirement spending. During the accumulation phase, the investor is adding money. During the withdrawal phase, the investor may be taking money out. The same market return can feel very different depending on whether you are buying more shares or selling shares to fund living expenses. That is why a serious retirement model should not stop at the final balance. It should also consider income needs, inflation, withdrawal timing, and sequence-of-returns risk.

1. Define the goal

Choose the retirement age, target spending, time horizon, and account context before adjusting return assumptions.

2. Model contributions

Test monthly DCA, annual contribution increases, bonus contributions, and different contribution frequencies.

3. Stress test the plan

Compare conservative, moderate, and optimistic cases so the plan does not depend on one perfect market path.

Practical takeaway: use the DCA Calculator for a quick recurring contribution model, the Investment Simulator for historical return windows, and the Premium DCA Calculator when you need weighted portfolios, fees, rebalancing, drawdown views, saved scenarios, and export-ready planning.

Retirement DCA simulation is about ranges, not one magic number

The right visual mindset is a range of possible outcomes. Your base case may show a comfortable retirement balance, but the useful question is what happens when return, inflation, fees, contribution growth, or retirement timing changes. The stronger the plan, the less it depends on one optimistic assumption.

This is also where WhatIfInvested fits the user journey: simulate the simple case, compare historical paths, then understand whether the plan needs a premium workflow with multiple portfolios, saved scenarios, fees, and reports.

What is a retirement DCA simulation?

A retirement DCA simulation is a projection that models how recurring investments may grow over time. DCA stands for dollar-cost averaging. In retirement planning, it usually means investing a fixed amount every week, month, or pay period instead of waiting for the perfect time to invest. The investor contributes through bull markets, bear markets, recessions, and recoveries.

The core advantage is structure. A DCA plan removes some of the emotional negotiation around timing. You do not need to decide every month whether the market looks cheap or expensive. You decide once that a certain amount will be invested on a schedule, then you review the plan at planned intervals. This is especially useful for retirement because retirement investing is long-term, repetitive, and easy to disrupt when headlines become stressful.

However, DCA is not magic. If a large lump sum is already available and markets rise for years, lump sum investing may outperform because more money was invested earlier. A retirement DCA simulation should therefore be honest about the tradeoff. DCA can reduce regret, automate behavior, and fit paycheck investing. It does not guarantee higher returns in every market environment.

The simulation becomes valuable because it lets you test those tradeoffs before they become emotional. You can compare monthly investing against lump sum investing, test different time horizons, include inflation, and see how a contribution increase changes the long-term result. For general investor education, Investor.gov's retirement toolkit is a useful official reference for thinking about retirement preparation and investor protection.

| Planning question | What the simulation tests | Why it matters |

|---|---|---|

| How much might I have? | Projected portfolio value at retirement. | Creates a baseline estimate for long-term planning. |

| How much should I contribute? | Monthly contribution needed to approach the target. | Turns a large future goal into a monthly action. |

| What if returns are lower? | Conservative market assumptions and weak historical windows. | Shows whether the plan depends on optimism. |

| What if I retire during a downturn? | Sequence-of-returns risk and withdrawal timing. | Helps avoid overconfidence near retirement. |

Inputs you need before running a retirement DCA simulation

The quality of a retirement simulation depends on the quality of the inputs. If the inputs are unrealistic, the output will look precise but be misleading. It is better to use ranges than to rely on one single assumption. Retirement planning is not a single number. It is a set of possible paths.

Current portfolio balance

Your current balance is the starting point. A person beginning with $0 and a person beginning with $100,000 can have very different retirement paths even if they contribute the same monthly amount. The early balance gets more years to compound, which means a small head start can become meaningful over decades.

Monthly contribution

This is the engine of a retirement DCA simulation. Contributions matter most in the early and middle years because they increase the capital available to compound. Later, investment returns may become a larger driver than new contributions, but the base is built through repeated deposits.

Time horizon

Time is one of the most powerful variables. A 25 year horizon and a 40 year horizon can produce dramatically different outcomes. This is why starting early is valuable even when the monthly contribution is modest. Time gives both contributions and returns more room to work.

Expected return

Expected return should be treated carefully. A high assumed return can make almost any plan look easy. A conservative return can reveal whether the plan still works under less favorable conditions. The best practice is to run several assumptions, such as low, moderate, and high growth cases.

Contribution increases

Many investors increase contributions as income rises. A retirement DCA simulation becomes more realistic when it includes annual contribution growth. Even small increases can make a large difference over decades because every raise gives the plan more capital to compound.

Fees, taxes, and account rules

Fees reduce compounding. Taxes can reduce usable wealth. Account rules can affect contribution limits, withdrawals, penalties, and flexibility. A basic calculator may ignore these details, but a serious retirement plan should at least estimate them. Fees matter more over long horizons because every dollar lost to fees is also a dollar that cannot compound.

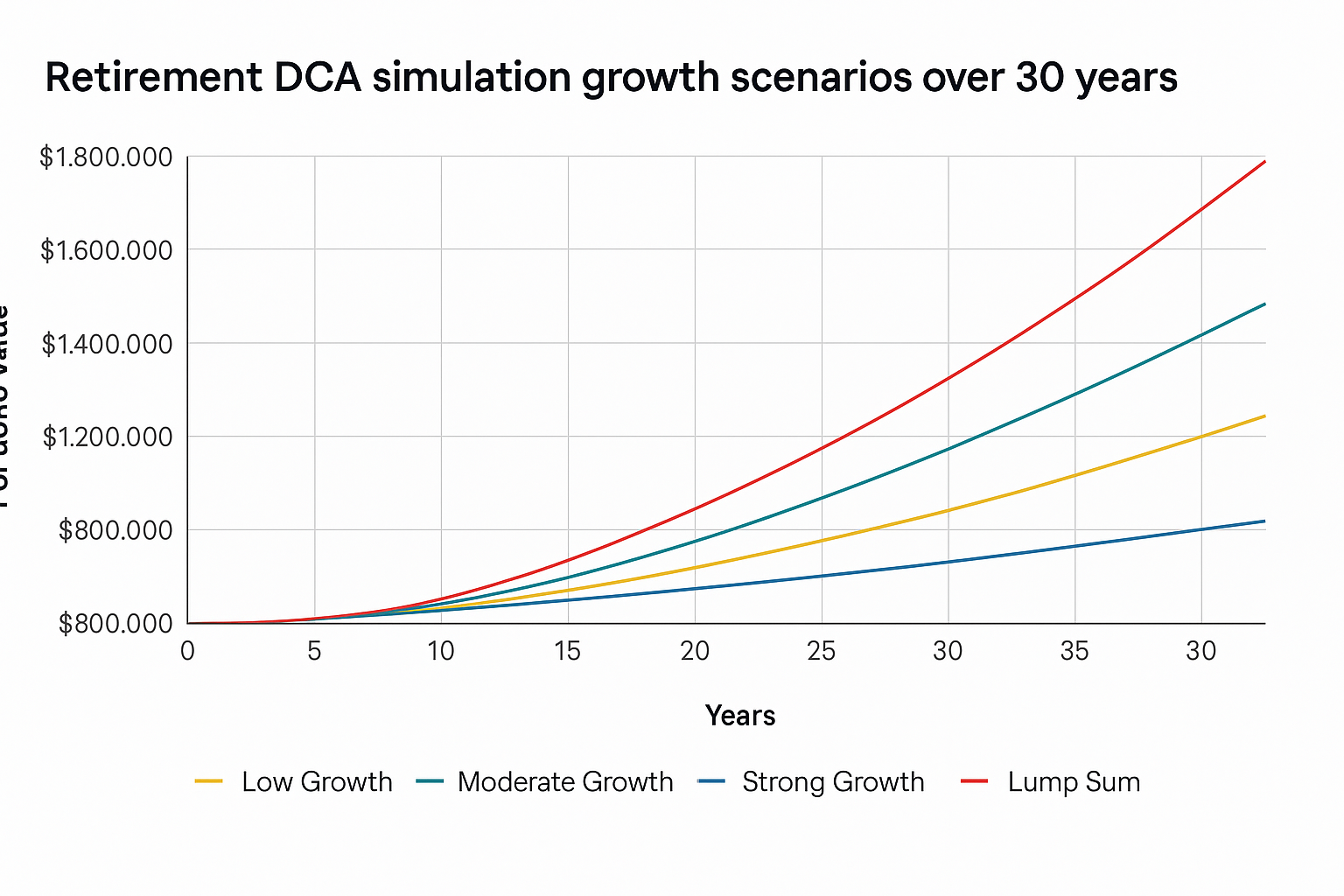

Retirement DCA scenario examples worth testing

The purpose of scenarios is not to predict the future. It is to understand sensitivity. If a plan only works in the optimistic case, it is fragile. If it still works in a moderate or conservative case, it is stronger. A retirement DCA simulation should always include more than one path.

Start with a base case that feels realistic. Then change one assumption at a time. Lower expected return. Raise inflation. Add fees. Delay retirement by two years. Increase contributions by 3% per year. Add a bear market before retirement. This process helps you learn which variables matter most.

| Scenario | Assumption style | What it tells you |

|---|---|---|

| Base case | Moderate return, current contribution, expected retirement age. | Shows the plan you are most likely to reference. |

| Conservative case | Lower return, higher inflation, same contribution. | Reveals whether the plan is too dependent on market strength. |

| Contribution growth case | Monthly contribution rises with income. | Shows the power of increasing savings over time. |

| Late start case | Shorter horizon with higher required contribution. | Shows the cost of waiting and the gap that must be closed. |

| Near-retirement downturn | Weak returns before or just after retirement. | Highlights sequence risk and the need for flexibility. |

The most useful comparison is often not optimistic versus pessimistic. It is current behavior versus improved behavior. For example, what happens if you invest $500 per month today, then raise it to $650 next year and $800 after the next promotion? That type of simulation connects the retirement plan to real cash flow instead of abstract market forecasts.

Inflation and fees can change the retirement answer

A future balance can look impressive until inflation is included. If a retirement DCA simulation says you may have $1,000,000 in 30 years, that does not mean the future portfolio will buy what $1,000,000 buys today. Inflation reduces purchasing power. This is why serious retirement planning should distinguish nominal dollars from real dollars.

Fees also matter. A difference that looks small each year can become large over decades. A 0.20% annual fee and a 1.00% annual fee may not feel dramatically different in the first year, but the gap compounds. The longer the time horizon, the more fee drag matters.

Taxes and account type can also change the usable result. A tax-advantaged retirement account, taxable brokerage account, TFSA, RRSP, 401(k), IRA, Roth IRA, or other account may treat contributions and withdrawals differently. The simulation should not pretend those rules are identical. When the plan becomes serious, account structure is part of the strategy.

Nominal value

The projected dollar amount before adjusting for purchasing power.

Real value

The projected value after considering inflation and future spending power.

Net value

The value after fees, taxes, and other frictions that reduce usable wealth.

Asset allocation and account choice in a retirement DCA plan

A retirement DCA simulation is incomplete if it ignores what you are buying. A monthly contribution into a broad diversified portfolio is different from a monthly contribution into one speculative asset. The contribution schedule is only one part of the plan. Asset allocation determines how much growth, volatility, drawdown, and recovery risk the investor may experience.

Younger investors often have more time to recover from drawdowns, so they may accept more equity exposure. Investors closer to retirement may care more about volatility, income, and sequence risk. That does not mean every older investor should avoid growth assets. It means the allocation should match the time horizon, income needs, risk tolerance, and emotional ability to stay invested.

Account choice matters too. For U.S. investors, the plan may involve a 401(k), IRA, Roth IRA, taxable brokerage account, or employer plan. For Canadian investors, it may involve a TFSA, RRSP, FHSA, taxable account, or workplace plan. Each account can have different tax treatment, contribution rules, and withdrawal rules. A simulation is more useful when the account context is clear.

| Decision | Why it matters | Simulation implication |

|---|---|---|

| Equity allocation | Higher growth potential but larger drawdowns. | Test both strong and weak market paths. |

| Bond or cash allocation | May reduce volatility near retirement. | Can lower expected return but improve stability. |

| Account type | Taxes and withdrawal rules affect usable income. | Separate pre-tax, after-tax, and taxable assumptions. |

| Rebalancing | Keeps risk from drifting too far from the plan. | Premium modeling may be useful for multi-asset portfolios. |

Withdrawals and sequence-of-returns risk

Accumulation is only the first part of retirement planning. Eventually the question changes from how much to invest to how much can be withdrawn. This is where sequence-of-returns risk matters. If markets fall early in retirement while withdrawals are being made, the portfolio may have less capital available to recover. The same average return can produce very different results depending on the order of returns.

A retirement DCA simulation should therefore connect the accumulation plan to a withdrawal plan. The investor may need to model an annual withdrawal amount, inflation-adjusted withdrawals, a flexible spending rule, or a cash reserve. The goal is not to create false certainty. The goal is to understand how vulnerable the plan is if retirement begins during a weak market period.

This is one of the strongest reasons to move from a simple free calculator to a premium workflow. A basic DCA calculator can show contribution growth. A more advanced planning tool can compare scenarios, include portfolio weights, adjust assumptions, save versions, and export reports. Retirement planning is rarely a one-screen decision once withdrawals enter the picture.

Accumulation risk

The risk that contributions, returns, or time horizon are not enough to reach the target balance.

Withdrawal risk

The risk that early losses, inflation, or spending needs reduce the portfolio faster than expected.

Common mistakes in retirement DCA simulations

Using one optimistic return number

The most common mistake is choosing a high expected return and treating the output as a plan. A retirement model should include lower-return scenarios. If the plan fails when returns are modest, the investor needs to know that early.

Ignoring inflation

A large future balance can be misleading if it is shown only in nominal dollars. Retirement is about purchasing power. The simulation should help the user understand what the money may buy, not just what number appears on a screen.

Forgetting contribution growth

Some investors model the same monthly contribution forever even though their income may rise. Others assume contribution increases that are too aggressive. The best approach is to test a realistic increase rule and compare it with the current contribution.

Confusing a projection with a guarantee

A simulation is a decision tool, not a promise. Markets will not follow the exact path in the model. The value comes from learning how the plan reacts when assumptions change.

Stopping at the retirement date

The retirement date is not the finish line. It is the start of a new phase. The plan should eventually include withdrawals, inflation-adjusted spending, and risk management after retirement begins.

A practical retirement DCA simulation framework

A useful framework keeps the plan simple enough to follow but detailed enough to reveal risk. Start with the current reality. What do you have today? What can you contribute monthly without breaking your budget? What is the time horizon? What account are you using? What asset mix are you modeling?

Then build three versions. The base case should be reasonable. The conservative case should be uncomfortable but plausible. The improved case should show what happens if behavior gets better, such as increasing contributions or reducing fees. This approach is more useful than trying to identify the single correct return assumption.

- Set the retirement target. Choose the age, income need, and planning horizon.

- Enter current assets. Include existing investment balances and account types.

- Model monthly DCA. Add contribution amount, frequency, and annual increases.

- Choose return ranges. Test conservative, moderate, and optimistic assumptions.

- Add realism. Include inflation, fees, taxes, and account constraints where possible.

- Stress test timing. Compare weak markets before retirement and early retirement drawdowns.

- Review the gap. Decide whether to raise contributions, extend time, adjust allocation, or lower spending assumptions.

The final step is action. If the simulation shows a gap, the goal is not to feel discouraged. The goal is to identify the lever with the highest impact. Sometimes the lever is contribution growth. Sometimes it is time. Sometimes it is reducing fees. Sometimes it is using a better workflow to compare scenarios instead of guessing.

Connect your monthly budget to your retirement DCA simulation

A retirement plan becomes much more useful when it is connected to real monthly cash flow. Many investors start with a big retirement target, then feel stuck because the number is too large. A better approach is to work backward from the monthly surplus. If your budget shows that you can invest $300, $500, or $1,000 per month, that amount becomes the first version of your retirement DCA simulation.

This is where the free and premium tools should work together. WhatIfBudget helps identify the investable surplus. The DCA Calculator shows how that surplus could compound if invested regularly. The Investment Simulator can test how similar monthly contributions behaved during historical market periods. Premium DCA becomes useful when the question expands into multiple portfolios, weighted allocations, fees, rebalancing, saved scenarios, or exportable planning reports.

The key is to avoid modeling a contribution that does not match real life. A $1,500 monthly contribution may look great in a calculator, but it is not useful if the household can only sustain $600 without stress. The better plan is the one the investor can actually follow through market cycles and life changes. A realistic retirement DCA simulation should therefore begin with what the budget can support today, then test how the plan improves when income rises or expenses fall.

Small changes can be powerful when they become automatic. An investor who starts at $400 per month and raises the contribution by $50 after each raise may build a stronger long-term plan than someone who waits until they can invest a perfect amount. Retirement planning rewards repeatable behavior. The simulation should make that behavior visible by showing how contribution increases, bonus investments, and lower fees change the long-term range.

| Budget insight | Simulation action | Why it improves the plan |

|---|---|---|

| Monthly surplus is stable. | Use it as the baseline DCA contribution. | The plan starts from real cash flow instead of wishful thinking. |

| Expenses can be reduced. | Run a second case with the saved amount invested monthly. | Shows the retirement value of budget decisions. |

| Income may rise. | Add annual contribution growth. | Models a realistic path where savings rate improves over time. |

| Surplus is inconsistent. | Use a lower automatic base plus occasional bonus contributions. | Keeps the plan resilient when income or expenses vary. |

Use the right WhatIfInvested tool for each retirement question

Retirement planning should move from simple to advanced. Start with the easiest model that answers the immediate question, then upgrade the workflow when the decision becomes more detailed. This keeps the free experience useful while making the Premium path feel natural.

DCA Calculator

Best for quick recurring contribution projections and simple monthly investing assumptions.

Investment Simulator

Best for historical windows, backtests, and understanding how market timing changed the path.

Premium DCA Calculator

Best for weighted portfolios, fees, rebalancing, benchmarks, saved scenarios, and export-ready analysis.

Frequently asked questions

What is a retirement DCA simulation?

A retirement DCA simulation models how recurring investments may grow over time for retirement. It can include current balance, monthly contributions, return assumptions, inflation, fees, and retirement timing.

Is DCA good for retirement investing?

DCA can be useful for retirement because it turns investing into a consistent habit. It does not guarantee better returns than lump sum investing, but it can reduce timing pressure and support long-term discipline.

What inputs should I use for a retirement DCA simulation?

Use current portfolio balance, contribution amount, contribution frequency, time horizon, expected return range, inflation estimate, fees, account type, and future withdrawal assumptions.

Should I include inflation in a retirement simulation?

Yes. Inflation affects future purchasing power. A retirement projection should show or at least consider the difference between nominal future dollars and real spending value.

How often should I contribute to a retirement DCA plan?

Monthly contributions are practical for many investors because they match paychecks and budgeting cycles. Weekly or biweekly investing can also work if it fits your cash flow and account setup.

Can I simulate withdrawals after retirement?

A basic DCA calculator may focus on accumulation, but a serious retirement workflow should eventually model withdrawals, inflation-adjusted spending, and sequence-of-returns risk.

What is sequence-of-returns risk?

Sequence-of-returns risk is the risk that poor market returns early in retirement hurt the portfolio more because withdrawals are happening while the portfolio is down.

When should I use Premium DCA for retirement planning?

Use Premium DCA when you need to compare weighted portfolios, fees, benchmarks, rebalancing, saved scenarios, exports, or more detailed planning than a simple free calculator can provide.

Final thoughts on retirement DCA simulation

A retirement DCA simulation is useful because it converts uncertainty into decisions. It cannot tell you exactly what the market will do. It can show how your plan responds to contribution changes, lower returns, inflation, fees, account choices, and withdrawal timing. That is enough to make better decisions than guessing.

The best retirement simulation is not the one with the most optimistic ending balance. It is the one that helps you act. If the plan looks weak, increase the contribution, reduce fees, extend the timeline, adjust the allocation, or compare more scenarios. If the plan looks strong, keep investing and review periodically. The purpose is not to predict the future. The purpose is to build a retirement process you can follow.

Start simple with the free tools, then move into Premium when the decision requires deeper comparison. That path keeps the user experience clean while supporting the real WhatIfInvested promise: simulate, compare, and understand before you commit to a long-term investment plan.

Educational simulation only. This article is not financial, tax, or investment advice. Historical returns, assumptions, fees, taxes, and inflation can materially change results. Consider a qualified professional for personal retirement planning decisions.