SPY Crash Recovery: What If You Invested During Every Market Crash?

Every market crash feels like the end of the story while it is happening. But SPY crash recovery history shows a different lesson: the investor who survives the drawdown, keeps cash needs separate, and continues buying quality exposure often has a much better chance than the investor waiting for perfect certainty.

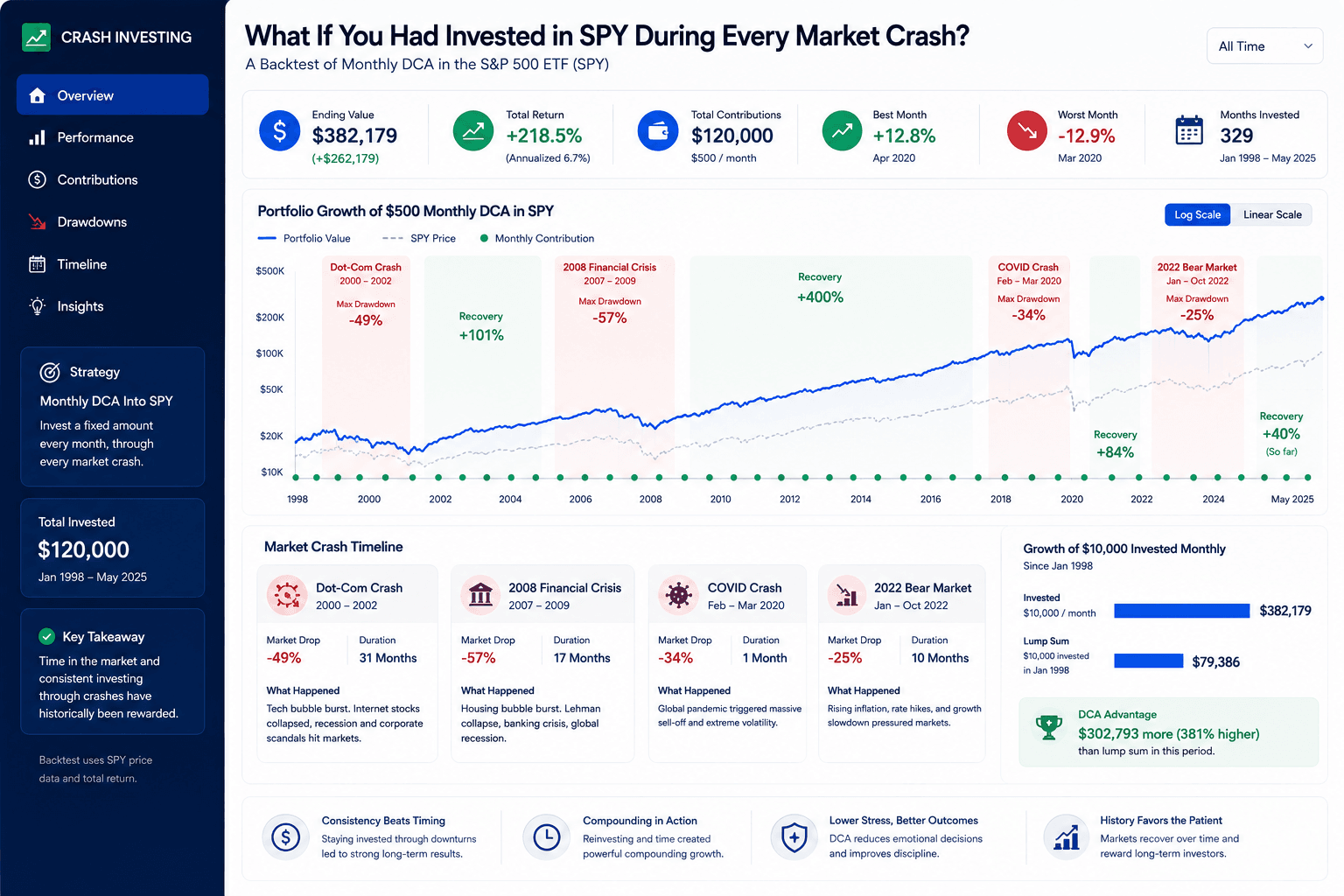

Core answer: SPY recovered from major crashes, but the path was never easy

SPY crash recovery is one of the most useful topics for long-term investors because it turns a vague fear into a concrete planning problem. The real question is not simply whether SPY recovered after past crashes. Historically, broad US equity exposure did recover from major bear markets, although the speed varied dramatically. The better question is whether an investor could hold through the drawdown, keep contributing, and avoid selling at the worst possible moment.

SPY is the SPDR S&P 500 ETF Trust, one of the most widely used funds for tracking large-cap US stocks. Because it follows the S&P 500, it gives investors exposure to a diversified basket of major US companies. That diversification has historically helped the fund participate in recoveries after recessions, valuation resets, policy shocks, and liquidity panics. But diversification does not prevent losses. During severe market crashes, SPY can fall hard enough to test even experienced investors.

This article looks at what would have happened if you invested in SPY during major market crashes, including the dot-com bust, the 2008 financial crisis, the COVID crash, and the 2022 bear market. The goal is not to pretend the future will copy the past. The goal is to understand recovery timelines, drawdown pain, dollar-cost averaging behavior, lump sum risk, and the rules that make a crash plan survivable for real investors making real decisions.

The bottom is obvious only later

In real time, market bottoms usually arrive with bad headlines and low confidence.

Systems beat courage

Automatic contributions can buy during panic when manual investors hesitate.

Survival comes first

Cash reserves and realistic allocation help investors avoid forced selling.

Practical takeaway: the best crash strategy is not “buy the exact bottom.” It is having a written process for continuing, rebalancing, and adding risk only when your personal finances can handle it.

SPY crash timeline: four different recoveries, four different investor tests

Market crashes are not identical. Some are slow valuation resets. Some are financial-system events. Some are sudden shocks. Some are inflation and rate-driven repricings. That matters because the investor experience is different in each case. A fast crash can feel terrifying but may recover quickly. A slow bear market can feel less dramatic day by day but more exhausting over time, which is why every SPY crash recovery review needs context.

When reviewing SPY crash recovery, focus on three dimensions: depth, duration, and behavior. Depth is how much the investment fell from peak to trough. Duration is how long it took to recover. Behavior is what the investor did while the portfolio was underwater. The last dimension is often the most important, because selling near the bottom can turn a temporary decline into a permanent loss that compounds negatively.

A long, grinding decline after a technology valuation bubble. Recovery required patience because the market did not bounce back immediately.

A deep drawdown tied to credit stress, bank failures, recession fears, and broad investor panic. The emotional pressure was extreme.

A very fast decline followed by an unusually fast rebound. Investors who waited for clarity could easily miss much of the recovery.

A bear market driven by rising rates, inflation pressure, and valuation compression. Recovery was tied to earnings resilience and changing rate expectations.

What counts as a market crash for SPY?

Investors often use rough thresholds. A correction is commonly described as a decline of about 10% from a recent high. A bear market usually means a decline of 20% or more. A crash is less formally defined, but people typically use the word when the decline is sharp, emotional, and confidence-damaging. For SPY crash recovery planning, the label matters less than the size of the drawdown and the investor’s ability to keep following the plan.

For SPY investors, crashes are also portfolio stress tests. They show whether your equity allocation is realistic, whether you have enough cash outside the portfolio, and whether your contribution plan can continue under pressure. If a 25% decline makes you abandon the strategy, then the strategy was too aggressive for your real temperament, even if it looked mathematically reasonable.

| Decline type | Common threshold | Investor feeling | Planning response |

|---|---|---|---|

| Pullback | Less than 10% | Annoying, but usually manageable | Keep contributions running and avoid overreacting. |

| Correction | Around 10% or more | Uncomfortable and headline-driven | Review allocation, but do not rewrite the plan emotionally. |

| Bear market | Around 20% or more | Fear, regret, and second-guessing | Use written DCA, rebalancing, and cash-buffer rules. |

| Severe crash | 30%+ or rapid panic decline | System-level fear | Survival first: no forced selling, no emergency-cash investing. |

The dot-com bust: the recovery test that required patience

The dot-com bust is one of the best reminders that not all recoveries are fast. After the late-1990s technology bubble, investors faced a long decline and a slow rebuilding period. For SPY investors, the pain was not only the size of the drawdown. It was the duration. A fast crash can be frightening, but a long bear market can slowly wear down discipline.

If you had invested a lump sum near the peak, the early experience would have felt brutal. Your account could be underwater for a long time. That is the hardest environment for investors who believed that diversified equity exposure “always comes back quickly.” SPY crash recovery may happen eventually, but the path can require years of patience.

DCA behaves differently in this kind of environment. A recurring contribution plan keeps buying at lower prices as the bear market unfolds. That does not make the portfolio immune to losses, but it can improve the average purchase price and reduce the emotional pressure of needing one perfect entry point. For investors adding from paychecks, a long bear market can become a period of accumulation rather than only a period of pain.

Long frustration

Slow bear markets test patience more than bravery. The question becomes whether the investor can keep going while progress feels invisible.

Lower purchase points

Recurring contributions can accumulate more shares while prices are depressed.

Giving up too early

Investors often abandon equities after several bad years, just before future returns improve.

The 2008 financial crisis: when SPY recovery required emotional strength

The 2008 financial crisis was different from the dot-com bust because the fear centered on the financial system itself. Bank failures, credit stress, housing losses, recession risk, and job insecurity made the market decline feel existential. In that environment, investors were not merely looking at a chart. They were wondering whether the financial system would function normally again.

For SPY investors, this period showed why crash plans need to be written before the crash. It is easy to say “I will buy when everyone is scared” when markets are calm. It is much harder when the headlines are full of layoffs, bailouts, falling home prices, and warnings about systemic risk. Many investors who wanted to buy the dip froze when the dip finally arrived.

A disciplined investor with a DCA plan had a clearer action: keep investing on schedule. A disciplined investor with rebalancing rules had another clear action: bring the portfolio back toward target weights if equities had fallen below the plan. Those actions still felt uncomfortable, but they were not invented in the moment. That matters because the less you need to improvise during panic, the better your odds of following through.

2008 lesson: the best crash strategy is the one that survives bad news. A mathematically perfect plan is useless if the investor cannot execute it under pressure.

The COVID crash: when recovery happened faster than confidence

The 2020 COVID crash was unusually fast. Markets fell quickly as the world faced shutdowns, economic uncertainty, and a public-health shock. Then the rebound was also unusually fast, supported by aggressive policy response, liquidity, and the market’s expectation that the economy would eventually reopen. This created a difficult SPY crash recovery lesson for market timers: if you wait until the news feels safe, the recovery may already be underway.

For DCA investors, the COVID crash demonstrated the value of automation. If contributions continued automatically, the investor bought through panic without needing to call the bottom. The buying window was short, but powerful. The investor who stopped contributions until “things became clear” may have missed some of the strongest rebound period.

This does not mean every future crash will recover quickly. That would be the wrong lesson. The better lesson is that recovery speed is unknowable in advance. Some crashes heal over years; others rebound in months. Because the path is uncertain, the plan should not depend on predicting the recovery date.

The panic was obvious

Prices moved quickly and headlines were frightening, which made manual decisions harder.

The rebound punished hesitation

Waiting for total certainty could mean missing a major part of the recovery.

DCA vs lump sum during SPY crashes

The DCA vs lump sum debate changes when the starting point is a crash. Lump sum investing can perform very well if deployed near a deep bottom and held through recovery. The challenge is that the bottom is not labeled in real time. Investors only know it was the bottom later. During the decline, every bounce can fail and every new low can feel like the beginning of something worse. A realistic SPY crash recovery plan should compare both entry styles before the next selloff arrives.

DCA reduces the pressure of choosing one entry point. Instead of asking, “Is today the bottom?” the investor asks, “Is my plan still running?” That difference is enormous during market stress. A DCA investor may not capture the exact best price, but they are less likely to keep all cash on the sidelines waiting for a moment that feels safe.

Lump sum has a strong mathematical argument when the cash is truly long-term and the investor can tolerate volatility. But during crashes, the behavioral argument for DCA can be just as important. If lump sum investing causes panic selling, the theoretical edge disappears. If DCA keeps the investor participating, it can be the better real-world choice.

| Strategy | Crash advantage | Crash weakness | Best fit |

|---|---|---|---|

| Lump sum before crash | Maximum exposure if markets keep rising | High regret if a crash follows soon after | Long horizon, high tolerance, strong cash buffer |

| Lump sum during crash | Can produce strong returns if recovery begins | Very hard to execute emotionally | Disciplined investors with written rules |

| Monthly DCA | Reduces timing pressure and keeps buying | May lag if rebound is extremely fast | Most investors building from income |

| Hybrid plan | Combines base DCA with extra drawdown buys | Requires rule clarity and available cash | Investors who want flexibility without guessing |

Use the DCA Calculator for recurring contribution math. Use the Investment Simulator to backtest historical periods. For multi-portfolio scenarios, fees, saved reports, rebalancing, and advanced assumptions, review Premium access.

What drives SPY recovery after a crash?

SPY crash recovery is driven by a mix of earnings recovery, policy support, valuation resets, interest rates, investor confidence, and sector leadership. A crash usually lowers prices because investors expect worse future conditions. Recovery begins when expectations stop getting worse, liquidity improves, earnings stabilize, or investors decide that future returns now look attractive enough.

One reason SPY has historically recovered is that the S&P 500 is not a single company. Weak businesses can fall out of the index over time while stronger companies gain weight. This does not eliminate risk, but it means the index evolves. The companies driving recovery after one crash may not be the same companies that led before the crash.

Dividends also matter. Price charts can understate the investor experience if they ignore distributions. A long-term investor who reinvests dividends may recover faster on a total-return basis than a price-only chart suggests. That is one reason backtests should be clear about whether they use price return or total return.

Earnings

Markets recover more easily when profits stabilize or investors believe future earnings will improve.

Rates

Interest-rate expectations affect valuations and investor willingness to own equities.

Policy

Fiscal and monetary responses can influence liquidity, confidence, and recovery speed.

Leadership

Sector rotation and index composition can change which companies pull the market forward.

How to backtest SPY crash recovery without fooling yourself

A SPY crash recovery backtest can be extremely useful, but only if it is built honestly. The most common mistake is choosing the exact crash bottom as the starting date and then acting as if the result proves a strategy. Of course buying the bottom looks excellent. The real investor question is different: what would have happened if you invested before the crash, during the crash, after the first rebound, or through monthly contributions while the news was still uncertain?

A better SPY crash recovery backtest uses multiple entry points. Test the peak before the decline, the first 10% drawdown, the first 20% drawdown, the worst month, and the first recovery period. Then compare lump sum, monthly DCA, and hybrid drawdown-buying rules. This gives a more realistic view of what investors actually face.

You should also distinguish between price return and total return. SPY distributes dividends, and reinvested dividends can change long-term outcomes. A price-only chart is useful for visual drawdown stress, but a total-return approach is often closer to what a disciplined long-term investor experiences if distributions are reinvested.

| Backtest choice | Why it matters | Better practice |

|---|---|---|

| Start date | One start date can make any strategy look better or worse. | Test several start dates around each crash. |

| Contribution schedule | DCA results depend on frequency and contribution size. | Use realistic monthly amounts based on your actual surplus. |

| Dividends | Ignoring distributions can understate long-term recovery. | Use total return where possible or document assumptions clearly. |

| Behavior | A strategy that looks good but is impossible to follow is not useful. | Include drawdown pain and time underwater in the review. |

When you use the Investment Simulator, do not stop at final value. Look at the worst drawdown, how long the portfolio stayed underwater, whether contributions were still affordable, and whether the strategy required emotional strength you may not actually have. A backtest should make your plan more realistic, not just more exciting.

Risk rules before investing during a market crash

Investing during a crash can be rewarding, but only if the money is truly available for long-term risk. The biggest mistake is using emergency cash or near-term money because prices look attractive. A market can fall further than expected, and personal financial stress can arrive at the same time as market stress. That is how investors are forced to sell low.

A good SPY crash recovery plan starts with household resilience. Keep emergency savings separate. Know your essential expenses. Avoid investing money needed for taxes, rent, tuition, down payments, or other short-term commitments. Then decide how much risk your portfolio can take without causing panic. If a 40% decline would make you sell everything, your allocation should not assume you can calmly hold through a 40% decline.

Cash buffer first

Do not use emergency reserves for market-crash investing.

Drawdown rule

Define what you will do at -10%, -20%, and -30% before the decline happens.

Contribution limit

Extra buying should not create debt, stress, or forced selling risk.

For practical planning, use WhatIfBudget to confirm how much monthly surplus you can invest without weakening your household. Then use historical testing to see whether your investing plan survives ugly periods.

The behavioral lesson: SPY recovery only helps investors who stay invested

SPY can recover and an investor can still fail. That happens when the investor sells during the drawdown, stops contributing at the wrong time, or waits too long to re-enter. SPY crash recovery is not automatically portfolio recovery if the investor interrupts the process.

This is why behavior is central to crash investing. The best historical backtest assumes the investor stayed invested. Real people face fear, job uncertainty, family pressure, account balances falling, and social media noise. The lower prices go, the harder the plan becomes emotionally. A plan that depends on perfect calm is not a real plan.

One helpful approach is to create an investment policy statement. It does not need to be complicated. It can simply state your target allocation, monthly contribution, emergency fund rule, rebalancing rule, and what you will do during major drawdowns. The goal is to give your future stressed self fewer decisions to make.

Panic selling

The investor locks in losses and misses the recovery that would have repaired the portfolio.

Stopping contributions

The investor avoids buying lower prices, weakening the main advantage of DCA.

Pre-written rules

The investor follows a plan that was created before fear took over.

Which SPY crash recovery plan fits different investors?

The same SPY crash can mean different things for different investors. A young investor contributing from salary may see lower prices as a chance to accumulate more shares. A retiree withdrawing from a portfolio may experience the same crash as sequence-of-returns risk. Someone with stable employment may be able to increase contributions. Someone worried about layoffs should prioritize liquidity. That is why SPY crash recovery planning should start with the investor profile, not only the market chart.

This is why “buy the dip” is incomplete advice. It ignores household context. The right move depends on time horizon, income stability, emergency fund strength, portfolio allocation, and whether the investor is adding or withdrawing money.

| Investor profile | Crash opportunity | Main risk | Suggested process |

|---|---|---|---|

| Beginner investing monthly | Lower prices can improve long-term accumulation. | Stopping contributions after seeing losses. | Automate a simple monthly DCA plan. |

| Investor with cash lump sum | Deploying after a large decline can improve future expected returns. | Waiting forever for a better bottom. | Use a staged entry or hybrid schedule. |

| Near-retiree | Rebalancing can help if cash and bonds are available. | Sequence risk and forced withdrawals. | Keep spending reserves separate from equity risk. |

| High-income saver | Can add extra contributions during drawdowns. | Overconfidence and overconcentration. | Use predefined drawdown boosts with maximum limits. |

A strong plan should feel almost boring when markets are normal. During a crash, boring becomes valuable. You do not want to invent your risk tolerance while your portfolio is falling. You want a plan that already tells you what to do.

Common mistakes when investing in SPY during crashes

SPY crash recovery history can inspire confidence, but it can also create overconfidence. Investors sometimes look at a long-term chart and conclude that every decline is automatically easy to buy. In reality, the hard part is not reading the chart after the fact. The hard part is living through the decline while your account balance is lower and the future feels uncertain.

Assuming the next crash will recover quickly

The COVID rebound was unusually fast. A future bear market could take much longer, especially if valuations, earnings, and interest rates move against investors at the same time.

Using emergency cash to buy the dip

A market crash can happen alongside job uncertainty. Investing emergency reserves may force you to sell later if life becomes expensive.

Changing the plan after every headline

If the rule changes every week, it is not a rule. It is emotional reaction dressed up as analysis.

Ignoring taxes, fees, and account type

Backtests often look clean, but real accounts include tax rules, contribution limits, spreads, and personal cash-flow constraints.

The cleanest correction is to simplify. Define the contribution amount, the account, the asset, the drawdown rule, and the maximum extra cash you are willing to deploy. If a crash plan cannot fit on one page, it may be too complicated to follow under pressure. Simple plans are easier to automate, explain, and repeat.

How to build a SPY crash recovery plan

A crash plan should be simple enough to follow. If it requires daily interpretation, complex macro forecasts, or perfect emotional control, it may fail when you need it most. A practical plan can use a base contribution plus optional drawdown rules.

For example, an investor might contribute $500 per month into a broad ETF strategy. If SPY falls 15% from a recent high, they add an extra $250 that month. If it falls 25%, they add an extra $500. If it falls 35%, they rebalance from bonds or cash reserves only if their emergency fund is still healthy. This is not a forecast. It is a rules-based response to volatility.

| Rule | Example | Why it helps |

|---|---|---|

| Base DCA | Invest $500 monthly no matter what. | Keeps participation consistent. |

| Drawdown boost | Add $250 after a 15% decline and $500 after a 25% decline. | Turns fear into a predefined buying opportunity. |

| Rebalancing | Return to target allocation once per quarter or year. | Forces disciplined buying and selling across asset classes. |

| Cash protection | Never invest emergency savings. | Reduces forced selling risk. |

The exact numbers should match your finances. A high-income investor with stable employment may be able to add more during drawdowns. A beginner with a small emergency fund should keep the rule modest. The goal is not to impress a spreadsheet. The goal is to create a SPY crash recovery process that survives real life.

Use tools to test SPY crash recovery instead of guessing

Historical SPY crash recovery analysis becomes more useful when you test your own assumptions. Change the start date, contribution amount, lump sum amount, frequency, and time horizon. Then ask what would have happened if you kept investing through the crash instead of waiting for confidence to return.

For a deeper downside lens, compare recovery time and drawdown so the crash review includes both the size of the decline and the patience required to get back to a prior high.

Investment Simulator

Backtest SPY and other assets across different start dates, market crashes, and contribution paths.

DCA Calculator

Model recurring contributions and long-term growth when you want a simpler projection.

Premium planning

Compare multiple portfolios, benchmarks, fees, rebalancing, withdrawals, saved scenarios, and export reports.

Related guides and next steps

This SPY crash recovery guide connects to several deeper WhatIfInvested resources. Use them to build a complete process instead of treating market crashes as one-off decisions.

SPY vs average investor

Compare benchmark discipline with the timing and behavior drag many investors experience.

For investor behavior, read The Psychology of Long-Term Investing. For contribution planning, use WhatIfBudget. For the tools hub, visit Calculators.

External references

For broader educational context, these external resources can help investors understand bear markets, SPY, and long-term index investing:

Final takeaways from SPY crash recovery history

The strongest lesson from SPY crash recovery history is not that investors should become fearless. Fear is normal. A large drawdown should feel uncomfortable because real money is involved. The lesson is that fear needs structure. Without structure, investors tend to improvise at exactly the moment when judgment is under the most pressure.

SPY’s historical recoveries show why long-term investors often benefit from staying invested, reinvesting distributions, and continuing contributions. But the same history also shows that recoveries can take very different shapes. A fast rebound like 2020 can punish hesitation. A long bear market like the dot-com period can punish impatience. A financial crisis can punish investors who use money they may need soon. The correct response is not one universal trade. It is a resilient process.

For most investors, that SPY crash recovery process starts with a realistic monthly contribution, a diversified core, and a written rule for volatility. The rule does not need to predict the next bottom. It only needs to prevent the most damaging behaviors: panic selling, stopping contributions, using emergency cash, and waiting forever for a perfect entry point.

Contribution discipline

Recurring investing turns crash periods into planned accumulation rather than emotional guessing.

Drawdown tolerance

If you cannot sleep during a decline, your allocation may need adjustment before the next crash.

Emergency cash

Cash outside the portfolio helps you avoid selling investments when life becomes stressful.

All-or-nothing timing

Waiting for the perfect bottom can leave an investor uninvested while recovery begins.

If you want to act on this article, do it in order. First, confirm your emergency fund. Second, decide your base contribution. Third, test your SPY or S&P 500 strategy with the Investment Simulator. Fourth, compare DCA and lump sum choices using the DCA vs Lump Sum guide. If you need deeper portfolio testing with fees, benchmarks, saved scenarios, and reports, then compare Premium access. The investor who prepares before volatility arrives has a much better chance of treating a crash as a planned stress test instead of a personal emergency.

Bottom line: SPY crash recovery rewards investors who survive the uncomfortable middle. The plan does not need to be perfect. It needs to be clear enough to follow when the chart looks ugly, the headlines feel heavy, and the easiest emotional choice is to stop investing.

Frequently asked questions

How long does SPY usually take to recover from a crash?

Recovery time varies widely. Some crashes recover in months, while prolonged bear markets can take years. Investors should plan for uncertainty rather than assume every decline will recover quickly.

Is SPY a good investment during market crashes?

SPY can be a useful broad-market vehicle for long-term investors, but buying during a crash still involves risk. The decision should depend on time horizon, cash reserves, allocation, and the ability to hold through volatility.

Is DCA better than lump sum during SPY crashes?

DCA is not always mathematically better, but it can be easier to execute during stress. Lump sum can perform strongly if invested near a bottom, but the bottom is only obvious in hindsight.

Should I increase contributions when SPY falls?

Only if your emergency fund, income, and risk tolerance support it. A predefined drawdown boost rule can help, but extra contributions should not use money needed for near-term expenses.

What is the biggest mistake investors make during crashes?

The biggest mistake is usually panic selling or stopping contributions at the worst moment. SPY recovery only helps investors who remain invested or continue following a disciplined plan.

How can I test SPY crash recovery with my own numbers?

Use the WhatIfInvested Investment Simulator to test start dates, contribution schedules, and historical windows. Use the DCA Calculator for simpler recurring contribution projections.

Educational simulation only. Historical performance does not guarantee future results. This article is educational content, not personal financial advice.