XBB vs VAB vs ZAG: Best Canadian Bond ETF in 2026?

XBB vs VAB vs ZAG is a practical comparison for Canadian investors who want broad bond exposure without overcomplicating the fixed-income side of a portfolio. The three ETFs look similar, but fees, duration, yield, liquidity, index methodology and portfolio role can still change the decision.

Which Canadian bond ETF fits best?

For many Canadian investors comparing XBB vs VAB vs ZAG in 2026, all three funds can serve as a broad core bond ETF. They generally provide exposure to investment-grade Canadian bonds across federal, provincial and corporate issuers. They pay monthly distributions and are commonly used as the fixed-income portion of a diversified portfolio.

The practical difference is often small. If your goal is simple Canadian aggregate bond exposure, any of the three may be reasonable. The tie-breakers are cost, tracking, liquidity, provider preference, index methodology and how the ETF behaves in your broader asset allocation.

XBB may fit if...

You already use iShares products, value its large fund ecosystem and want FTSE Canada Universe exposure.

VAB may fit if...

You prefer Vanguard, want a low-cost aggregate bond ETF and like its float-adjusted index approach.

ZAG may fit if...

You use BMO ETFs, want low-cost aggregate bond exposure and value strong Canadian ETF liquidity.

In practical terms, XBB vs VAB vs ZAG is less about finding a dramatic winner and more about choosing a low-cost Canadian bond ETF that fits your account, time horizon and rebalancing process.

The better decision is usually made at the portfolio level. A bond ETF should support the role you need: lower volatility, monthly income, rebalancing flexibility, or a calmer path beside equities. If XBB, VAB and ZAG are all close on cost and exposure, the next question is whether your bond allocation is the right size for your risk tolerance, tax location and investment horizon.

XBB vs VAB vs ZAG: ETF Profiles

These funds are built for similar jobs: broad exposure to the Canadian investment-grade bond market. They usually hold hundreds or thousands of bonds, including federal government bonds, provincial bonds and corporate bonds. That diversification reduces single-issuer risk compared with buying one individual bond.

| ETF | Provider | Typical role | Index approach | Distribution style |

|---|---|---|---|---|

| XBB | iShares / BlackRock | Core Canadian bond allocation | FTSE Canada Universe Bond Index exposure | Monthly distributions |

| VAB | Vanguard Canada | Core Canadian bond allocation | Bloomberg Global Aggregate Canadian Float Adjusted Bond Index exposure | Monthly distributions |

| ZAG | BMO ETFs | Core Canadian bond allocation | FTSE Canada Universe Bond Index exposure | Monthly distributions |

XBB and ZAG are often very close because they track the same broad FTSE Canada Universe bond benchmark. VAB uses a different benchmark methodology, so its weights can differ slightly. In practice, these differences may be modest, but they explain why returns and risk are not always perfectly identical.

Official sources to verify current figures: iShares XBB, Vanguard VAB, and BMO ZAG.

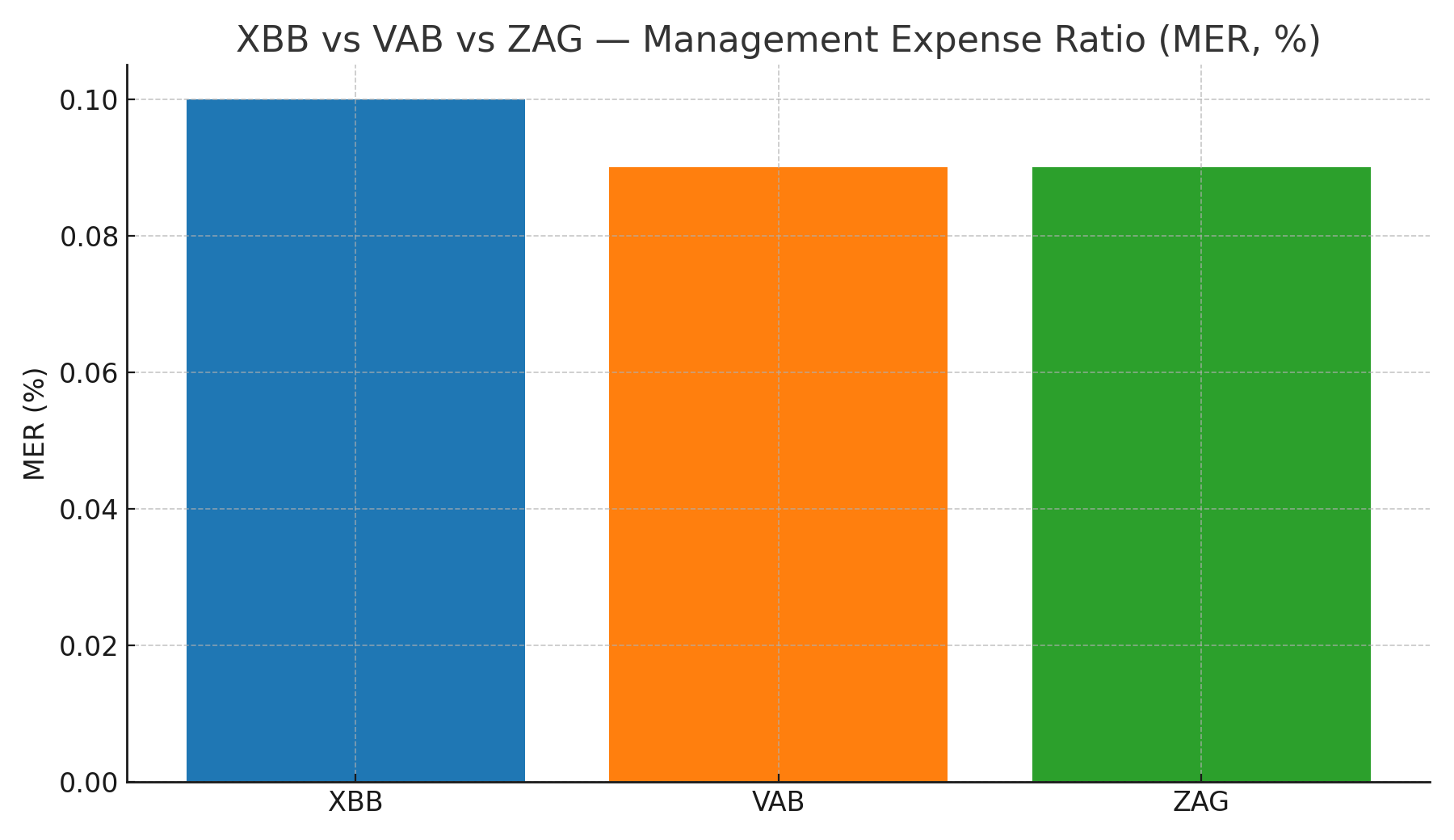

Fees: Why Small MER Differences Still Matter

Bond ETF returns are usually lower than equity ETF returns, so fees matter. A difference of a few basis points may look tiny, but in fixed income the margin between options can be narrow. If two ETFs provide nearly the same exposure, the lower-cost product has a small structural advantage.

That said, MER is not the only cost. Investors should also consider bid-ask spreads, tracking difference, liquidity, tax treatment and how easily the ETF trades on their brokerage platform. For long-term investors making small monthly purchases, the MER may matter more than spreads. For larger trades, liquidity and execution can become more important.

Look beyond headline MER

- Tracking difference versus benchmark

- Bid-ask spread

- Trading volume and liquidity

- Tax location and account type

When MER matters most

- Long holding periods

- Large fixed-income balances

- Similar benchmark exposure

- Low expected return environment

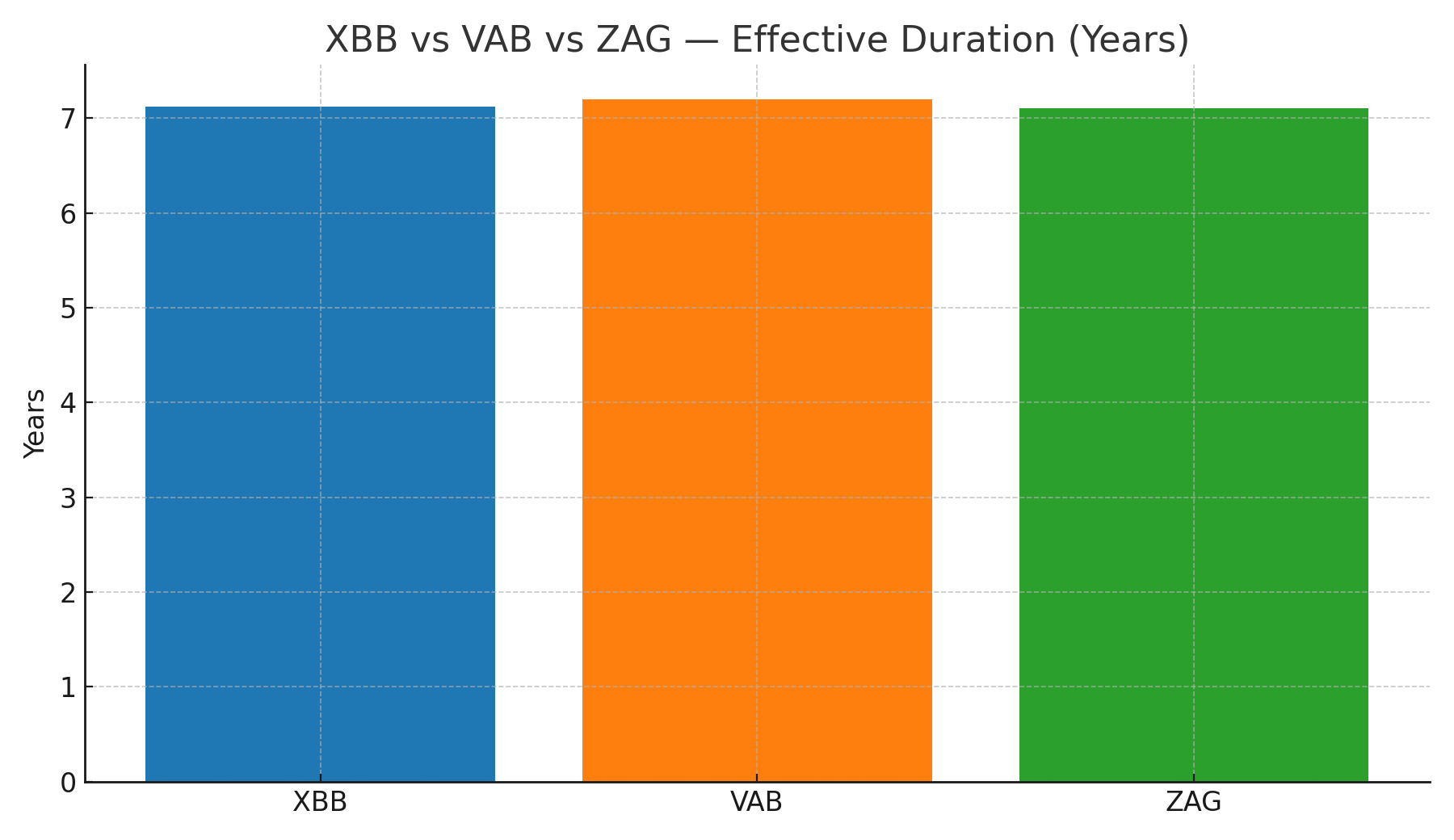

Duration: The Biggest Risk Many Bond ETF Buyers Miss

Duration measures a bond ETF's sensitivity to interest-rate changes. A fund with a duration near seven years can decline meaningfully when interest rates rise, and can rise when rates fall. This is why bond ETFs are not the same as cash. They can be safer than equities in many scenarios, but they still carry interest-rate risk.

Aggregate bond ETFs like XBB, VAB and ZAG usually sit in an intermediate duration range. That makes them useful as broad fixed-income holdings, but not ideal for every short-term savings goal. If you need money in one or two years, a money market fund, high-interest savings ETF, GIC ladder or short-term bond ETF may be more appropriate.

| Rate scenario | What tends to happen | Investor takeaway |

|---|---|---|

| Rates rise quickly | Bond prices usually fall | Aggregate bond ETFs can experience drawdowns |

| Rates fall | Bond prices usually rise | Intermediate bond ETFs may benefit |

| Rates stay stable | Income becomes a larger driver of return | Yield and fees matter more |

| Inflation surprises higher | Longer-duration bonds may struggle | Shorter duration can reduce sensitivity |

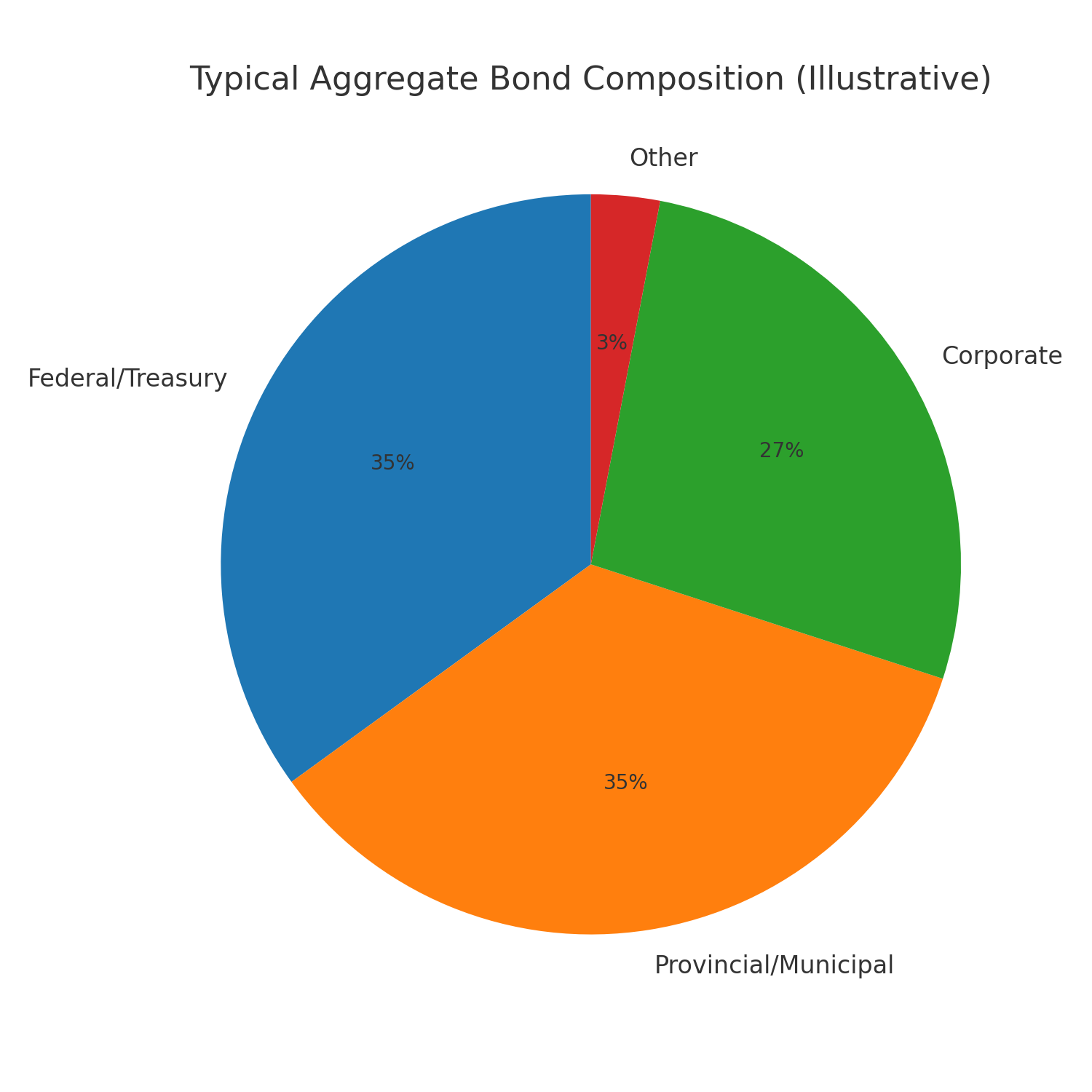

Composition and Credit Quality

XBB, VAB and ZAG are generally investment-grade bond ETFs. They do not exist to maximize yield at all costs. Their job is to provide broad fixed-income exposure with diversification across issuers and maturities. This makes them different from high-yield bond ETFs, preferred share ETFs or narrow corporate bond funds.

The main holdings categories typically include Government of Canada bonds, provincial bonds, municipal or agency exposure and investment-grade corporate bonds. Government bonds tend to offer more defensive characteristics. Corporate bonds may add yield but bring more credit sensitivity. The mix matters because fixed income can play different roles: income, diversification, stability or liability matching.

Government bonds

Usually more defensive and sensitive to rates.

Corporate bonds

Can add yield but may behave more like risk assets during stress.

Provincial bonds

Often sit between federal and corporate risk profiles.

Portfolio Role: Why Own Canadian Bond ETFs?

Canadian aggregate bond ETFs are usually not purchased to beat the stock market. They are purchased to reduce volatility, provide income, create rebalancing opportunities and support a smoother portfolio journey. In a balanced portfolio, bonds can help investors stay invested in equities by making drawdowns less emotionally severe.

The right bond allocation depends on goals. A younger investor with stable income may hold little or no bonds. A retiree drawing income may want more fixed income to reduce sequence-of-returns risk. A homebuyer saving for a near-term down payment may need safer instruments than intermediate aggregate bond ETFs.

| Investor situation | Bond ETF role | Important caution |

|---|---|---|

| Young long-term investor | Optional stabilizer | Too many bonds can reduce growth |

| Balanced investor | Volatility reduction and rebalancing | Duration risk still exists |

| Near retirement | Drawdown control and income planning | Match duration to spending needs |

| Short-term savings | Usually not ideal as sole cash substitute | Bond ETF prices can decline |

For a broader allocation view, compare this article with All-in-One ETF Canada Comparison, the Canadian ETF comparison tool, VEQT vs XEQT, VFV vs VOO for Canadians, and TFSA vs RRSP vs FHSA.

DCA, Lump Sum and Rebalancing for Bond ETFs

Dollar-cost averaging into bond ETFs can make sense when contributions come from monthly cash flow. It is simple, repeatable and removes the pressure of choosing a perfect entry point. However, for investors with a lump sum, the choice depends on risk tolerance, interest-rate views and how the bond allocation fits the rest of the portfolio.

Rebalancing is often more important than the choice between XBB, VAB and ZAG. If equities fall sharply and bonds hold up better, selling a small portion of bonds to buy equities can restore the target allocation. If equities surge, new contributions can rebuild the bond sleeve. This is the real value of fixed income in many portfolios: it provides dry powder and emotional stability.

Use DCA when...

- You invest from monthly income

- You want a simple habit

- You dislike entry-point regret

- You are building an allocation gradually

Use rebalancing when...

- Portfolio weights drift

- Equities rise or fall sharply

- Your risk profile changes

- You want process-based decisions

Test different contribution and rebalancing choices with the Investment Simulator and the DCA Calculator.

Understanding Bond ETF Returns: Price Return vs Total Return

One common mistake with bond ETFs is looking only at the price chart. Bond ETFs distribute income, so a simple price chart can understate the investor experience. Total return includes both price movement and reinvested distributions. This matters especially for XBB, VAB and ZAG because a meaningful portion of expected return comes from interest income.

When interest rates rise, the market price of existing bonds usually falls because newer bonds offer higher yields. That can make a bond ETF look weak in price terms. But over time, the ETF also reinvests into higher-yielding bonds as the portfolio rolls over. The initial price decline can be painful, but future income may improve. This is why bond ETF analysis requires patience and a total-return lens.

The opposite can happen when interest rates fall. Existing bonds with higher coupons become more valuable, and bond ETF prices can rise. But future reinvestment yields may become lower. A good investor understands both sides: bond ETFs can benefit from falling rates in the short run, but long-term income depends on the yield environment going forward.

| Return component | What it means | Why it matters for XBB, VAB and ZAG |

|---|---|---|

| Price return | Change in ETF market price | Moves with rates, spreads and bond prices |

| Distribution income | Monthly interest distributions paid by the ETF | Can be a major part of total return |

| Total return | Price return plus reinvested distributions | Best way to compare long-term outcomes |

| Yield to maturity | Approximate forward-looking bond portfolio yield before costs and changes | Useful but not a guaranteed return |

If you are comparing these ETFs, focus on total return and risk together. A slightly higher yield is not always better if it comes with more duration risk, more credit risk or worse tracking.

Tax Location: Where Should Canadian Investors Hold Bond ETFs?

Tax location can matter as much as fund selection. Bond ETF distributions are generally less tax-efficient than Canadian eligible dividends or capital gains when held in a taxable account. For that reason, many investors prefer to hold fixed income in registered accounts when possible, such as an RRSP, TFSA or FHSA depending on the goal and available contribution room.

This is not a universal rule. The best location depends on your total portfolio, income level, account room, withdrawal timeline and tax bracket. A retiree may prioritize cash flow and withdrawal flexibility. A younger investor may prioritize growth assets inside a TFSA. A high-income earner may value RRSP deductions. The ETF choice and account choice should be considered together.

RRSP

Often useful for interest-bearing assets because tax is deferred until withdrawal. Also relevant for retirement planning.

TFSA

Can shelter bond income from tax, but some investors prefer to reserve TFSA room for higher-growth assets.

Taxable account

Works when registered room is full, but interest distributions can be tax-inefficient compared with capital gains.

There is no perfect asset-location answer for everyone. If you are building a simple portfolio, start with the right asset allocation first. Then optimize account placement when the portfolio becomes large enough for the tax difference to matter.

When Aggregate Bond ETFs Are Not the Right Tool

XBB, VAB and ZAG are useful, but they are not universal solutions. A Canadian aggregate bond ETF is an intermediate-duration fixed-income product. That means it can be appropriate for long-term portfolio diversification, but less appropriate for money you absolutely need soon.

If your goal is a down payment next year, emergency savings or short-term tuition cash, price stability may matter more than yield. In that case, cash-like products, high-interest savings ETFs, money market funds, GICs or short-term bond ETFs may be better aligned. The problem is not that XBB, VAB or ZAG are bad products. The problem is using them for the wrong time horizon.

| Goal | Better fit | Why aggregate bond ETFs may be less ideal |

|---|---|---|

| Emergency fund | Cash, HISA, money market | Need high liquidity and very low volatility |

| Home purchase in 1-2 years | HISA, GIC ladder, short-term instruments | Intermediate duration can create price declines |

| Retirement portfolio | Aggregate bond ETF may fit | Can diversify equities and support rebalancing |

| Long-term balanced portfolio | XBB, VAB or ZAG may fit | Broad exposure and monthly distributions can be useful |

Good investing is not only about choosing strong products. It is about matching each product to the correct job.

Scenario Analysis: How These ETFs May Behave

Bond ETFs react to interest rates, inflation expectations, credit spreads and investor demand for safety. XBB, VAB and ZAG are diversified, but they cannot escape the basic mechanics of bonds. Understanding scenarios helps investors avoid surprise.

Scenario 1: Rates fall

If Canadian interest rates decline, existing bonds with higher coupons generally become more valuable. Intermediate-duration bond ETFs can benefit from that repricing. In this environment, XBB, VAB and ZAG may deliver positive price returns in addition to distributions. However, future yields may gradually fall as the fund reinvests into lower-yielding bonds.

Scenario 2: Rates rise again

If rates rise, bond ETF prices may decline. This is the classic duration risk. The silver lining is that future reinvestment yields may improve over time, but the short-term mark-to-market loss can still be uncomfortable. Investors who understand duration are less likely to panic when bond ETFs temporarily fall.

Scenario 3: Credit spreads widen

During economic stress, corporate bonds can underperform government bonds because investors demand more compensation for credit risk. Aggregate bond ETFs hold both government and corporate exposure, so composition matters. The government-bond sleeve may provide ballast, while corporate exposure can add income but also risk.

Scenario 4: Inflation stays sticky

If inflation remains higher than expected, bond yields may stay elevated and longer-duration bonds may struggle. In that environment, investors may prefer shorter-duration products or a bond ladder. Aggregate ETFs can still play a role, but expectations should be realistic.

Common Mistakes When Comparing XBB, VAB and ZAG

Mistake 1: Choosing only by yield

A higher yield can come from duration, credit exposure or market conditions. Always ask what risk created the yield.

Mistake 2: Ignoring duration

Duration explains why bond ETFs can fall when rates rise. It should be checked before buying.

Mistake 3: Treating bond ETFs as cash

Aggregate bond ETFs can lose value over short periods. Emergency money should usually be more stable.

Mistake 4: Over-optimizing tiny fee gaps

Fees matter, but savings rate, allocation, account choice and behavior often matter more.

The best choice is not always the ETF with the most attractive single metric. It is the fund that fits the portfolio role, trades efficiently, has low costs and can be held through changing rate environments.

How to Make the Final Decision

If you are stuck between XBB, VAB and ZAG, simplify the decision. First decide whether an aggregate Canadian bond ETF is the right category for your goal. If yes, compare MER, duration, holdings, benchmark, liquidity and provider preference. Then choose one and focus on keeping the overall plan consistent.

For most long-term investors, the difference between holding one of these ETFs consistently and constantly switching between them is probably larger than the difference between the ETFs themselves. Switching can create transaction costs, tax consequences and unnecessary complexity. Unless there is a clear reason to change, consistency is usually enough.

| Decision step | Question | Why it matters |

|---|---|---|

| 1 | Do I need intermediate Canadian bonds? | Confirms the asset class before the product |

| 2 | What is my time horizon? | Short horizons may need lower volatility |

| 3 | How much duration risk can I accept? | Prevents surprise during rate changes |

| 4 | Which provider and account setup is easiest? | Simplicity improves follow-through |

| 5 | How will I rebalance? | Turns bonds into a portfolio process |

A good bond ETF should make your plan calmer, not more confusing. If the comparison becomes too technical, return to the purpose: stability, diversification, income and rebalancing support.

Which ETF Should You Choose?

If you already use one provider's ETFs and your brokerage supports it cleanly, there may be little reason to switch between XBB, VAB and ZAG purely for tiny differences. The funds are close enough that investor behavior, allocation size and account structure often matter more than the product choice.

Choose XBB if you prefer iShares and want a large, established Canadian universe bond ETF. Choose VAB if you prefer Vanguard's structure and low-cost philosophy. Choose ZAG if you prefer BMO ETFs, want a very common aggregate bond product and like its low fee profile. In many portfolios, the best choice is the one you will hold consistently.

Related Tools and Next Reads

Frequently Asked Questions

Are XBB, VAB and ZAG basically the same?

They are similar because they all provide broad Canadian investment-grade bond exposure, but they are not perfectly identical. Index methodology, fees, holdings, duration and tracking can differ slightly.

Which has the lowest MER?

MERs can change, so verify the current factsheets. Historically, the differences have been small, which means cost is important but not the only decision factor.

Can XBB, VAB or ZAG lose money?

Yes. Bond ETFs can decline when interest rates rise, credit spreads widen or markets reprice fixed income. They are generally less volatile than equities, but they are not cash.

Are these ETFs good for short-term savings?

They may not be ideal for very short-term savings because aggregate bond ETFs have duration risk. Short-term bond ETFs, cash ETFs, high-interest savings accounts or GICs may fit short horizons better.

Should I hold Canadian bonds in a TFSA or RRSP?

That depends on your overall tax situation, account room and asset location strategy. Interest income is usually less tax-efficient in taxable accounts, so registered accounts are often worth considering.

Final Takeaway

XBB, VAB and ZAG are all credible Canadian aggregate bond ETFs. The biggest decision is usually not which one is perfect, but whether your fixed-income allocation matches your time horizon, risk tolerance and portfolio purpose.