Timing the Market vs DCA: Which Strategy Works Better?

Market timing promises a better entry point. Dollar-cost averaging promises a repeatable system. The real question is not which sounds smarter, but which one gives investors a better chance of acting, staying invested, and avoiding costly behavior mistakes.

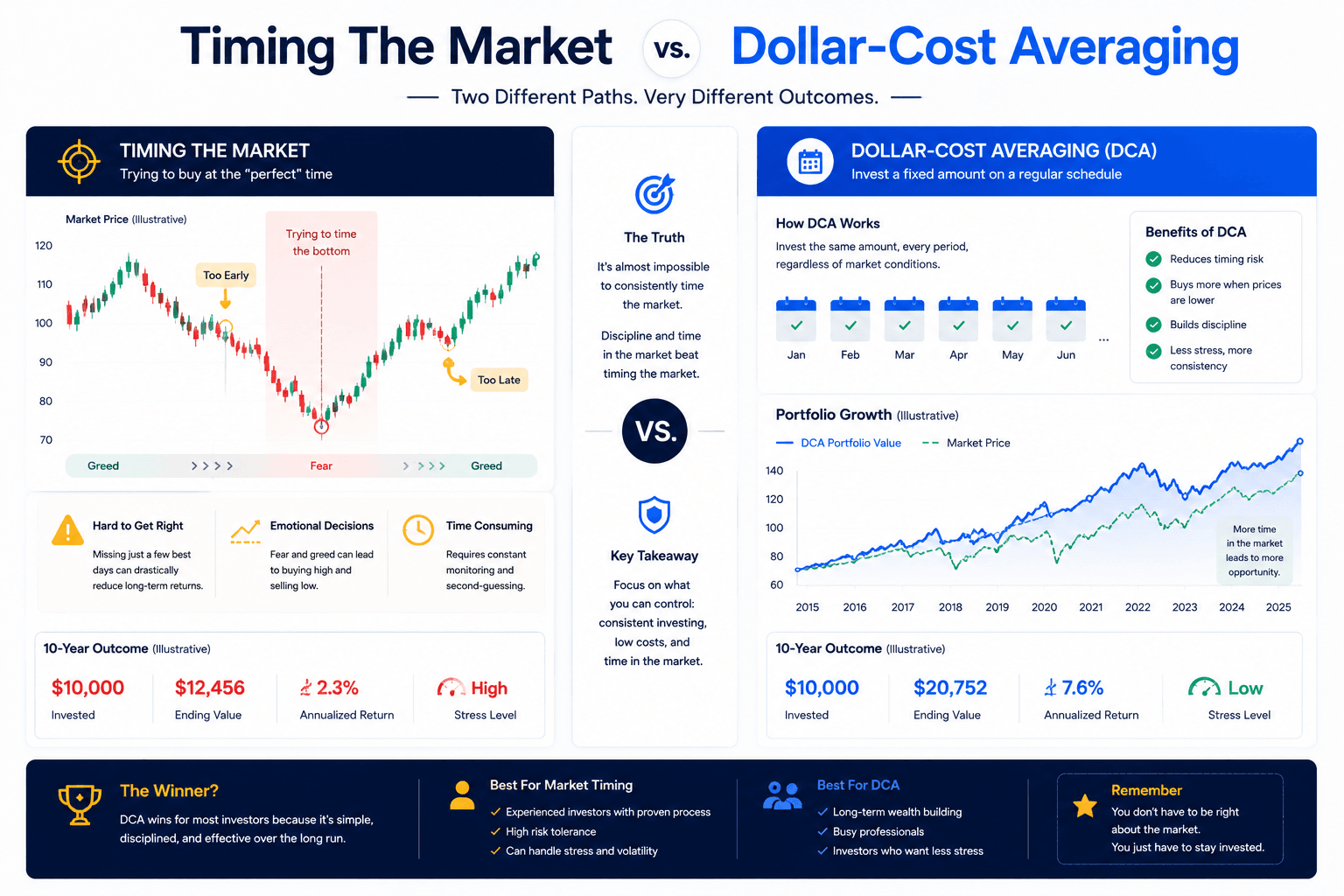

Quick answer: market timing can beat DCA, but only if you are right early and disciplined enough to act

Timing the market vs DCA is not a fair fight if we assume perfect foresight. If an investor could reliably buy near bottoms and avoid major declines, market timing would beat dollar-cost averaging. The problem is that most investors do not have that skill, and even many professionals struggle to do it consistently.

Dollar-cost averaging, or DCA, usually wins as a real-world process because it removes the need to guess the perfect date. Instead of waiting for a bottom that may never arrive, you invest on a schedule. That does not guarantee higher returns, but it often improves follow-through.

You identify turning points

Timing works when you buy before rebounds, avoid long declines, and actually deploy cash when fear is high.

You need consistency

DCA helps when uncertainty would otherwise keep you stuck in cash or cause you to overreact to headlines.

You want rules and flexibility

A hybrid plan can invest regularly while adding extra contributions after defined declines.

The practical answer: use DCA as the default system, then add limited timing rules only if they are written, measurable, and easy to execute.

What market timing and DCA actually mean

Before judging which strategy is better, it helps to define the terms carefully. Many people say they are “timing the market” when they are really just hesitating. Others say they use DCA when they simply invest from paychecks because that is when money arrives.

Trying to choose better entry and exit points

Market timing means adjusting when you invest based on expected future market movement. A timer might wait for a correction, invest after a technical signal, reduce exposure before a recession, or buy aggressively after a crash.

Investing on a fixed schedule

DCA means investing a fixed amount at regular intervals, regardless of whether the market feels cheap or expensive. The strategy favors process over prediction.

These strategies solve different problems. Market timing tries to improve price. DCA tries to improve behavior. Timing asks, “Is now a good moment?” DCA asks, “Is my plan still running?”

That distinction matters because many investors fail not because they picked the wrong ETF, but because they never actually invested the cash. They wait for clarity, then wait for confirmation, then wait for a pullback. By the time they act, the original opportunity may be gone.

When market timing really can beat DCA

It would be dishonest to say market timing never works. Timing can beat DCA in certain environments. If you invest right after a major drawdown, avoid buying before a large decline, or increase contributions near a market bottom, the result can be excellent.

Timing also matters more for highly volatile assets. Buying a broad index fund after a 5% dip is different from buying Bitcoin after a 70% crash. In very volatile assets, entry point can strongly affect future returns. But volatility also makes the signal harder to interpret. A 30% crypto decline might be the beginning of a recovery, or only the first leg of a deeper drawdown.

The strongest case for timing is not day trading. It is rule-based valuation or risk management. For example, an investor might keep normal monthly DCA contributions running, but add extra capital when the market falls by 20% from its high. That is still a timing element, but it is predefined instead of emotional.

| Timing approach | Can work when | Main risk |

|---|---|---|

| Buying after large drawdowns | Investor has cash, courage, and a clear rule. | The drawdown keeps getting worse. |

| Valuation-aware investing | Expected returns are meaningfully different across asset classes. | Valuations can stay stretched for years. |

| Trend-following rules | The rule is systematic and tested. | Whipsaws and missed rebounds. |

| Emotional waiting | Almost never as a repeatable strategy. | Cash sits idle while markets recover. |

Why market timing usually fails in real life

Market timing fails because it requires more than one correct decision. You need to know when to wait, when to buy, when to stop waiting, when to hold through volatility, and when to ignore new fear. Missing any one of those steps can destroy the benefit of getting another step right.

The most common timing mistake is waiting for a correction and then failing to buy during the correction. Investors imagine they will be brave when prices fall, but market bottoms rarely feel comfortable. They usually arrive with bad headlines, recession fears, layoffs, banking stress, geopolitical risk, or collapsing sentiment.

Another issue is that markets often rebound before the news improves. By the time investors feel safe, prices may already be much higher. Timing requires buying when the environment still feels uncertain. That is psychologically difficult.

Waiting too long

Cash earns comfort, but it may miss compounding when markets rise.

Moving the goalposts

The investor waits for a 10% drop, gets it, then waits for 20% because fear has increased.

Re-entering late

The recovery begins before confidence returns, so the investor buys after much of the rebound.

Even if market timing sounds logical, the process is hard to repeat. That is why many long-term investors prefer a system they can execute during normal months and stressful months alike.

The real edge of DCA is not prediction. It is execution.

DCA works because it makes investing boring. That may sound unexciting, but boring is powerful. A recurring investment schedule turns market participation into a habit rather than a monthly debate.

When you invest every month, you buy during good news, bad news, expensive markets, cheap markets, and everything in between. You stop asking whether this week is perfect and start asking whether your savings rate is strong enough. That shift is valuable.

Less decision fatigue

You do not need to make a fresh market call every contribution date.

Better behavior

You are less likely to freeze in cash because the next contribution is already scheduled.

Consistent participation

Your portfolio benefits from long-term exposure even when the news cycle is noisy.

DCA is not perfect. It can underperform lump sum or well-executed timing when markets rise quickly. But for many investors, the benefit is not maximum theoretical return. The benefit is building a plan they can actually follow.

What research says about time in the market

Investment research usually favors staying invested over trying to jump in and out. This does not mean timing can never work. It means timing is difficult enough that most investors should be cautious before making it the center of their strategy.

Charles Schwab’s market timing analysis compares different investing behaviors and highlights how hard it is to beat consistent investing by waiting for perfect moments. Their broader message is that early and consistent investing usually matters more than perfect entry.

Vanguard’s research on cost averaging explains that staged investing can reduce immediate market exposure, but it also delays risk-taking. If markets rise while cash waits, the investor pays an opportunity cost.

Fidelity’s investor education on volatility also emphasizes having a plan and staying disciplined rather than reacting to short-term market moves. The most useful lesson is not that volatility disappears, but that investors need rules before volatility arrives.

Bottom line from the evidence: timing can improve returns in hindsight, but systematic investing is easier to execute in real life. For most investors, a reliable system beats a fragile forecast.

Decision map: should you use timing, DCA, or a hybrid?

A good strategy starts with self-awareness. If you can honestly follow a timing rule, you may use one. If you tend to freeze when markets fall, a simple DCA plan may be better. If you want some flexibility without becoming a full market timer, use a hybrid.

| Your situation | Suggested approach | Why |

|---|---|---|

| You invest from every paycheck | DCA | Income arrives gradually, so recurring investing is natural and simple. |

| You have cash available but fear investing at a peak | Hybrid | Invest part now and schedule the rest to reduce regret risk. |

| You have a tested rule for buying after major declines | Rule-based timing | Timing can be useful when it is predefined and not emotional. |

| You keep waiting for “a better time” | DCA | The main problem is hesitation; a schedule solves that better than more analysis. |

| You need the money in the next 12-24 months | Avoid forcing risk | Short-term cash needs should not be decided by DCA vs timing alone. |

The best compromise: DCA with timing rules

A hybrid strategy can combine the best parts of both approaches. You keep a normal recurring DCA plan running, but you also define specific rules for adding extra money during major declines.

For example, an investor might invest $500 every month no matter what. Then they add an extra $1,000 if the market falls 15% from its high, and another $1,000 if it falls 25%. This is not emotional timing because the rule exists before the crash. The investor is not guessing based on headlines; they are following a prewritten plan.

Invest every month

Keep the core habit running so you are never fully dependent on calling bottoms.

Add during drawdowns

Use clear thresholds such as -15%, -25%, or -35% instead of vague feelings.

Keep emergency cash separate

Never use money needed for near-term expenses just because the market is down.

This hybrid method gives the investor something to do during downturns without turning the entire plan into a guessing game. It is especially useful for people who like the idea of buying dips but do not want their whole strategy to depend on timing.

What a serious timing rule should look like

The biggest difference between disciplined timing and emotional timing is documentation. A disciplined timing rule can be written down before the market moves. It has a trigger, an action, a funding source, a reset rule, and a maximum amount of cash that can be held back. Emotional timing is vague. It sounds like “I will wait until things look better” or “I will buy after the crash.” Those sentences feel reasonable, but they are not investment rules.

A real timing rule should be boring enough that another person could follow it without reading your mind. If your plan depends on interpreting headlines, guessing Federal Reserve language, or deciding whether investor sentiment “feels too optimistic,” it may be too subjective for most long-term investors. Subjective systems can work for skilled professionals, but they are difficult for everyday investors to repeat consistently.

The purpose of a rule is not to predict perfectly. The purpose is to prevent paralysis. When volatility arrives, your future self should not need to invent a plan while stressed. The rule should already say what happens next.

| Rule component | Good example | Weak example |

|---|---|---|

| Trigger | Invest an extra $1,000 if the chosen index falls 15% from its recent high. | Invest when the market looks cheap. |

| Action | Buy the same ETF already used in the long-term portfolio. | Search for whatever asset is trending that week. |

| Cash limit | Keep no more than 25% of investable cash reserved for drawdown rules. | Hold most cash until the perfect entry arrives. |

| Reset rule | After the extra buy, return to normal monthly DCA unless another threshold triggers. | Keep watching and decide later. |

| Failure rule | If no trigger happens within 6 months, invest the reserve over the next 3 months. | Let cash sit indefinitely because the plan never forced a decision. |

This is where many investors discover that they do not actually want market timing. They want a sense of control. A written system gives that control without requiring a constant forecast. If you cannot define the rule in advance, DCA may be the better default.

The hidden cost of missing strong market days

One reason timing the market is difficult is that strong market days often cluster near stressful periods. Major rebounds can happen during bear markets, recessions, banking scares, inflation shocks, and periods when the news still feels terrible. An investor who waits for comfort may miss the early recovery because comfort usually arrives late.

This does not mean every investor must be fully invested at all times. Cash has a role. Emergency funds, short-term goals, tax bills, home down payments, and near-term spending should not be forced into risky assets. But long-term investment cash is different. If the money is meant for a 10-year, 20-year, or retirement horizon, sitting out of the market can create an opportunity cost.

The problem is not one missed day in isolation. The problem is that market timing often creates repeated delays. The investor waits before investing, waits during the decline, waits during the rebound, and then waits again because prices now feel too high. A DCA plan avoids this loop by making participation the default.

Cash drag

Money that waits for a better entry does not compound if markets rise while it sits aside.

Decision delay

The more conditions required before investing, the easier it is to keep postponing action.

Re-entry stress

After a rally, the investor may feel even more pressure because the original entry is gone.

For this reason, a timing plan should always answer a simple question: if the market does not give me the dip I want, when will I invest anyway? Without that answer, timing becomes an open-ended excuse to delay.

How to backtest timing vs DCA without fooling yourself

Backtesting can help compare timing the market vs DCA, but it can also create false confidence. The danger is building a strategy that looks brilliant because it was designed around what already happened. A rule that perfectly buys the last crash may fail in the next one because the next cycle will have different timing, depth, and emotional context.

A useful backtest should test multiple start dates, not only the one that proves your preferred argument. For example, if you compare investing before a major crash, DCA may look attractive because it avoids deploying all cash at the peak. If you compare investing before a long bull market, lump sum or immediate investing may look better because waiting delays exposure. Both results can be true depending on the start date.

When using the Investment Simulator, avoid asking only, “Which strategy won in this one period?” Ask better questions: How often did each strategy win? How large were the differences? How bad were the drawdowns? Would I have stuck with the plan while it was underperforming? Did the rule require actions I could realistically take?

Multiple start dates

Do not judge the strategy from one cherry-picked cycle.

Final value and drawdown

A higher ending value may come with more emotional stress.

Cash deployment

A timing rule should not leave money idle for years.

Behavioral realism

If you would not follow the rule in real life, the backtest is not useful.

Premium-style scenario work becomes useful when you want to compare multiple portfolios, apply fees, model rebalancing, save scenarios, or export reports. That is why the free tools are good for quick decisions, while Premium access fits deeper planning.

Which strategy fits different investor profiles?

There is no universal answer because the best strategy depends on the investor. The same market environment can produce different correct decisions for different people. A 25-year-old investing from paychecks has a different problem than a 60-year-old deciding what to do with a large cash balance. A new investor fighting hesitation needs a different system than a disciplined investor with a written rebalancing process.

| Investor profile | Best starting point | Reason | Useful next tool |

|---|---|---|---|

| Beginner investing from salary | DCA | The main goal is building the habit and avoiding overthinking. | DCA Calculator |

| Investor with a large cash lump sum | Hybrid | Investing part now and staging the rest can reduce regret risk. | Lump Sum vs DCA page |

| Long-term investor with strong discipline | Immediate investing plus rules | If cash is long-term and the plan is clear, delaying can create opportunity cost. | Investment Simulator |

| Investor prone to panic selling | DCA with automation | A simple automatic plan reduces the number of emotional decisions. | Start with $50/month |

| Advanced investor comparing portfolios | Rule-based hybrid | Multiple assumptions, fees, benchmarks, and rebalancing need deeper scenario testing. | Premium access |

The most important question is not “What strategy sounds optimal?” It is “What strategy will I follow when prices are falling, news is scary, and the perfect answer is unavailable?” If the answer is unclear, choose the simpler process.

Checklist before you try to time the market

Before adding market timing to your investing plan, use this checklist. If several answers are unclear, keep the plan simple and use DCA as the foundation.

Can you write the rule in one sentence?

If the trigger cannot be stated clearly, it will be hard to execute under stress.

Do you have a deadline for idle cash?

A timing reserve should not become a permanent excuse to avoid risk.

Is emergency money separate?

Market drawdowns should not push you to invest money needed for bills or short-term goals.

Will you buy when the signal feels uncomfortable?

The best timing opportunities often happen when confidence is low.

Simple rule of thumb: if timing makes you invest more consistently and with clearer rules, it may help. If timing makes you wait, second-guess, and avoid action, it is hurting the plan.

Does the answer change for ETFs, stocks, crypto, or cash?

The timing the market vs DCA debate changes depending on the asset. A diversified ETF is not the same as a single stock. Bitcoin is not the same as a broad stock market fund. A high-interest savings account is not the same as long-term retirement money. The more volatile and concentrated the asset, the more entry price can matter. But higher volatility also makes timing harder because price moves become more extreme and emotionally charged.

For broad ETFs, DCA is often a strong default because the investment thesis is usually long-term market participation. The investor is not trying to guess the next product cycle or the next earnings report. They are trying to own a broad basket of businesses over many years. In that context, delaying too long can be costly because long-term expected returns come from being invested.

For individual stocks, timing and valuation can matter more. Buying a strong business at an unreasonable price can lead to years of weak returns. But individual stock timing is also harder because company-specific risks matter: earnings, competition, margins, management, regulation, debt, and investor expectations. If you use DCA into single stocks, position sizing becomes important because recurring contributions can accidentally create too much concentration.

For crypto, the tradeoff is sharper. DCA can reduce the emotional stress of entering a volatile asset, but it does not remove crypto-specific risk. A recurring Bitcoin or Ethereum plan may help investors avoid buying only after hype cycles, but the investor still needs a clear allocation limit. DCA into a volatile asset without a maximum allocation can become risky if the portfolio becomes too concentrated.

| Asset type | DCA fit | Timing relevance | Main caution |

|---|---|---|---|

| Broad market ETF | Strong | Moderate | Waiting too long can create cash drag. |

| Sector ETF | Good, but monitor allocation | Higher | Sector cycles can create long underperformance periods. |

| Individual stock | Depends on conviction and valuation | High | Company-specific risk can dominate the strategy. |

| Bitcoin or crypto | Useful for behavior control | Very high | Volatility and concentration need strict allocation limits. |

| Short-term cash goal | Usually not the right question | Low | Money needed soon should prioritize safety and liquidity. |

This is also why portfolio context matters. An investor with 95% of their wealth in a diversified portfolio can treat a small crypto DCA plan differently than someone putting most of their savings into one volatile asset. Strategy quality depends on the whole financial picture, not only the chart of one ticker.

How to turn the decision into a monthly investing plan

Once you decide whether DCA, timing, or a hybrid approach fits you, the next step is turning the idea into a repeatable monthly plan. This is where many investors lose momentum. They read comparisons, agree with the logic, and then never define the actual contribution amount, asset list, schedule, or review process.

A good monthly plan should answer five questions. First, how much money can you invest without weakening your emergency fund? Second, what assets will receive the contributions? Third, how often will contributions happen? Fourth, what rule applies during large market declines? Fifth, when will you review the plan without constantly tinkering?

Set the base contribution

Choose a number that can survive normal life: bills, rent, food, emergencies, and irregular expenses.

Choose the asset mix

Keep the portfolio simple enough that you understand what each asset is supposed to do.

Write the drawdown rule

If you want a timing element, define it before volatility arrives.

For example, a beginner might invest $300 monthly into a broad ETF, review the plan twice per year, and avoid timing entirely. A more advanced investor might invest $800 monthly, keep 15% of new cash available for drawdown rules, and add extra contributions only after predefined declines. Both can be reasonable. The difference is that both are written plans, not emotional reactions.

To make this concrete, use WhatIfBudget to identify a realistic monthly surplus, then use the DCA Calculator to model recurring contributions. If you want to compare historical periods or stress-test start dates, use the Investment Simulator. That workflow turns a broad strategy debate into a specific plan.

Examples: how the same investor can behave differently with rules

Consider two investors with $12,000 available to invest over the next year. Investor A wants to time the market. Investor B uses a written DCA plan.

Investor A waits for a 10% correction. The market rises 8% instead. Investor A becomes frustrated and keeps waiting. Then a 7% decline happens, but it does not meet the 10% rule, so they continue waiting. By the time a larger drop arrives, headlines are negative, and they hesitate again.

Investor B invests $1,000 each month automatically. They buy at higher prices during rallies and lower prices during pullbacks. They do not get the perfect entry, but they keep moving. After twelve months, the full amount is invested and the plan did not require prediction.

Now imagine Investor C uses a hybrid. They invest $6,000 immediately, then $500 per month for 12 months, with an extra contribution rule after large drawdowns. This investor gets early exposure, maintains consistency, and still has a plan for volatility. In many real-world situations, Investor C may have the most balanced process.

Use tools to test the strategy instead of guessing

The best way to understand market timing vs DCA is to test your own assumptions. Choose a starting date, an asset, a contribution amount, and a time horizon. Then compare what would have happened with different rules.

Investment Simulator

Backtest historical strategies and compare how different start dates changed outcomes.

DCA Calculator

Model recurring contributions, growth assumptions, and long-term portfolio value.

Premium workflow

Compare multiple portfolios, benchmarks, fees, rebalancing, withdrawals, and exports.

Common mistakes when comparing timing and DCA

The timing vs DCA debate creates several traps. Avoiding these mistakes can matter more than the strategy label itself.

Calling hesitation “timing”

If there is no written rule, no trigger, and no deadline, the investor is not timing the market. They are avoiding a decision.

Using hindsight charts as proof

It is easy to point to past bottoms. It is much harder to identify them in real time when fear is high.

Stopping DCA during bad markets

The most valuable DCA purchases often happen when prices feel uncomfortable. Stopping during declines weakens the whole strategy.

Ignoring cash drag

Cash feels safe, but waiting too long can quietly reduce long-term growth if markets rise.

Another subtle mistake is over-optimizing contribution frequency. Monthly, biweekly, and weekly investing can produce slightly different outcomes, but the major driver is consistency. An investor who contributes every month for years usually has a stronger foundation than one who keeps redesigning a perfect timing system.

Related guides and next steps

This article sits inside the broader DCA and investing strategy cluster. Use these guides to go deeper:

DCA vs Lump Sum

Compare DCA, lump sum, and hybrid investing through a practical decision framework.

Which strategy wins over time?

Review the broader historical comparison between DCA and lump sum investing.

Start with $50/month

Use a small recurring contribution to build the habit before optimizing everything.

For cash-flow planning, start with WhatIfBudget. For recurring contribution math, use the DCA Calculator. For historical testing, use the Investment Simulator.

Frequently asked questions

Is timing the market better than DCA?

Market timing can be better if the investor correctly identifies attractive entry points and actually invests when the rule triggers. For most investors, DCA is easier to execute because it does not require predicting short-term market movements.

Why does market timing usually fail?

It usually fails because investors must make multiple correct decisions: when to wait, when to buy, when to stop waiting, and when to hold through fear. Many investors wait for a dip, then hesitate when the dip arrives.

Does DCA guarantee better returns?

No. DCA does not guarantee higher returns. It spreads purchases over time and can reduce regret, but it can underperform if markets rise while cash is waiting to be invested.

Can I combine market timing and DCA?

Yes. A practical hybrid is to keep a normal DCA plan running while adding predefined extra contributions after large drawdowns. The key is writing the rules before the market becomes stressful.

Is DCA good for beginners?

DCA is often beginner-friendly because it is simple, automatic, and less emotionally intense than trying to pick the perfect entry point. It helps new investors build consistent habits.

What is the biggest risk of waiting for a better entry point?

The biggest risk is cash drag. Markets can rise while the investor waits, and the “better” entry point may never arrive. Waiting can feel safe but still be costly over long periods.

Educational simulation only. Historical performance does not guarantee future results. This article is educational content, not personal financial advice.