How to Budget a $2,000 Salary and Save $400/Month

Learning how to budget 2000 salary income is not about squeezing every dollar until life feels impossible. It is about giving rent, food, bills, savings, debt, and investing a clear order so a small paycheck can still create progress.

Quick answer: how to budget a $2,000 salary

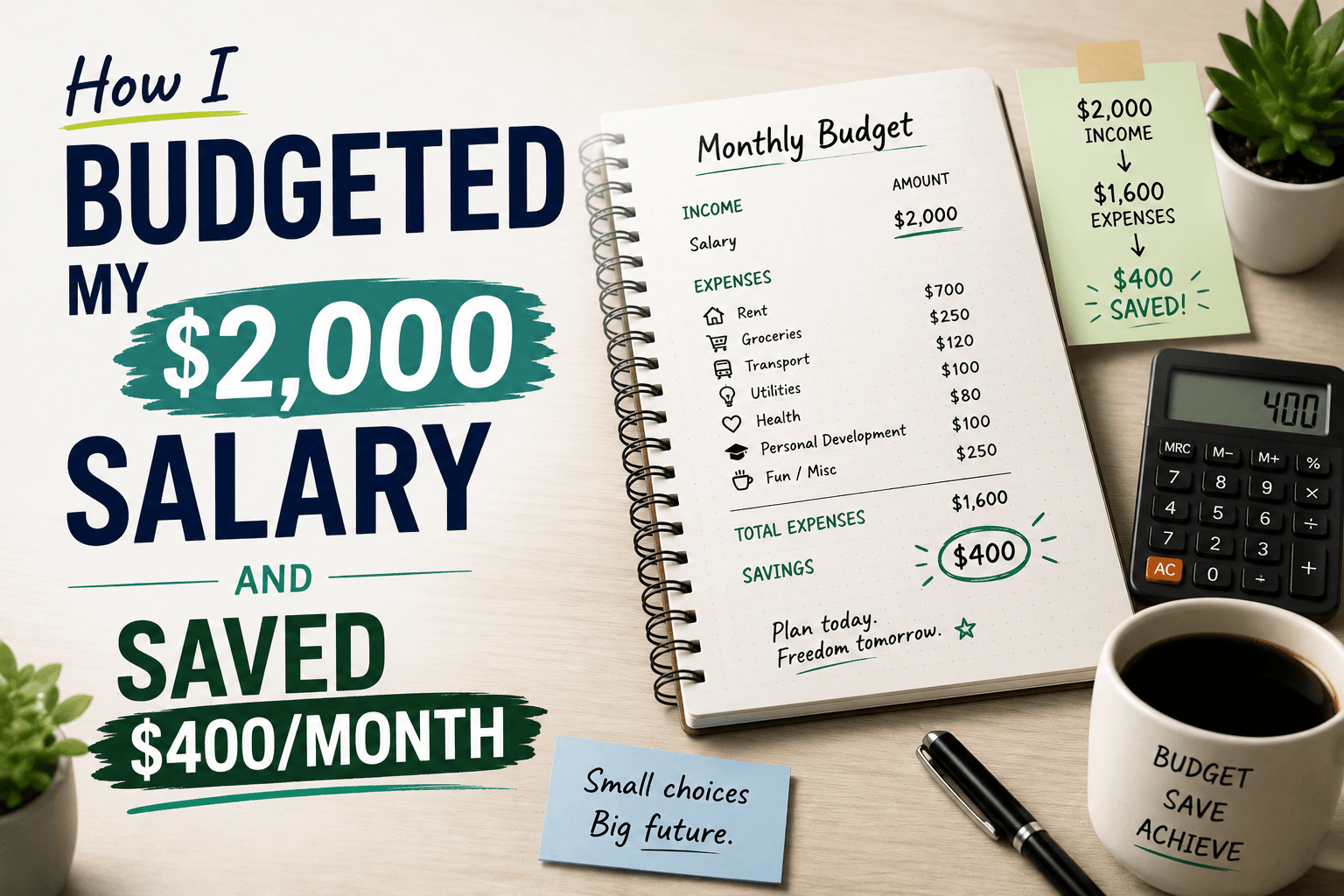

A realistic $2,000 monthly budget starts with essentials, protects a small emergency fund, then automates savings before discretionary spending expands. If your take-home pay is $2,000, saving $400 per month means saving 20%. That is possible for some people, but only if fixed costs are controlled and the transfer happens automatically.

The clean version is simple: cap needs around $1,200, cap flexible spending around $400, and reserve $400 for savings, debt payoff, or investing. If rent is high, the first version may be $200 saved and $200 recovered through lower bills, side income, or a slower transition. The point is not to pretend every $2,000 budget looks the same. The point is to build a system that survives real bills.

Use the budget as a decision tool, not a guilt tool. If the numbers do not fit, the budget is showing you the constraint: housing is too high, debt is heavy, income is low, or spending categories need tighter limits. Once the constraint is visible, the next move becomes easier.

| Category | Target amount | Why it matters | Adjustment if tight |

|---|---|---|---|

| Housing and utilities | $700-$850 | Usually the largest fixed cost. | Roommate, renegotiation, smaller space, or slower savings target. |

| Food and household | $280-$360 | Flexible but not optional. | Meal plan, store brands, batch cooking, weekly cap. |

| Transport, phone, insurance | $250-$400 | Recurring costs can quietly dominate a small budget. | Transit, lower phone plan, quote insurance, reduce subscriptions. |

| Debt minimums | Varies | Must be paid before aggressive investing. | Use avalanche or snowball after a starter emergency fund. |

| Savings and investing | $200-$400 | Creates emergency protection and long-term options. | Start lower, then increase after one bill or debt payment is reduced. |

Practical next step: open WhatIfBudget, enter your income and recurring expenses, then send the monthly surplus to the Compound Interest Calculator or DCA Calculator once savings are stable.

A $2,000 monthly budget template that can save $400

The easiest way to make a $400 savings target realistic is to separate fixed bills from weekly choices. Fixed bills should be planned first because they are hard to change mid-month. Weekly choices should be capped because they are where small leaks usually happen. Savings should be automatic because leftover savings rarely survives.

| Line item | Monthly amount | Notes |

|---|---|---|

| Rent or shared housing | $750 | Best case for a $2,000 budget is moderate rent or shared costs. |

| Utilities and internet | $120 | Average bills across the month. |

| Groceries and household | $320 | Works better with a weekly plan than daily improvisation. |

| Transport | $180 | Transit, gas, parking, or basic car costs. |

| Phone, insurance, subscriptions | $170 | Review every recurring charge quarterly. |

| Debt minimums | $160 | Minimums first, extra payoff after starter savings. |

| Personal and flexible spending | $300 | About $75 per week. |

| Savings, debt payoff, investing | $400 | Automated near payday. |

This template is not the only correct answer. It is a working model. If rent is $1,100, saving $400 may require a roommate, cheaper transport, lower debt payments, side income, or a temporary $150-$250 savings target. If rent is $600, saving $400 may be easier, and the extra margin can go toward emergency savings or investing.

When you budget a $2,000 salary, the numbers need to be honest. Do not hide irregular costs like annual fees, clothing, gifts, repairs, school costs, medical expenses, or family support. Put them into sinking funds, which are small monthly amounts saved before the expense arrives.

Lower the big fixed costs before cutting every small joy

On a $2,000 salary, fixed costs decide whether the budget breathes. A person with $700 rent has a different life than a person with $1,200 rent. A person with no car payment has more flexibility than a person with a loan, gas, insurance, repairs, and parking. This is why the biggest budget improvements often come from boring recurring decisions.

Housing

If housing is above 45% of take-home pay, the savings target may need to start lower unless income rises or housing changes.

Transport

A car can silently turn a manageable budget into a fragile one. Count insurance, fuel, maintenance, parking, and registration.

Recurring bills

Phone plans, subscriptions, insurance, bank fees, and unused apps are small alone but powerful together.

A useful exercise is to list every recurring charge and mark each one as keep, reduce, pause, or cancel. The goal is not to eliminate joy. It is to stop paying for things that no longer match your priorities. A $20 recurring charge does not sound like much, but five similar charges can equal $100 per month, which is one quarter of a $400 savings goal.

For official budgeting worksheets and money-management tools, the CFPB's Your Money, Your Goals resources are a useful starting point because they focus on cash flow, debt, goals, and practical household decisions.

Use weekly spending limits to protect the monthly plan

Monthly budgets fail because the month is too long to feel real. Weekly limits are easier to manage. If flexible spending is $300 per month, that is about $75 per week. If groceries are $320, that is about $80 per week. Weekly caps turn the budget into a set of small decisions instead of one vague hope.

The strongest method is to create a weekly allowance for groceries, eating out, personal spending, and small entertainment. Once the weekly money is gone, pause until the next week. This protects the savings transfer because the transfer already happened near payday.

| Weekly category | Example cap | Control rule |

|---|---|---|

| Groceries | $70-$85 | Plan meals before shopping and use one main store. |

| Personal spending | $25-$50 | Use a separate card, envelope, or account. |

| Eating out | $15-$30 | Choose intentionally instead of accidental daily spending. |

| Transport extras | $10-$25 | Track rideshare, parking, and fuel top-ups. |

If you overspend one week, do not abandon the plan. Reduce the next week slightly or adjust the target. Consistency matters more than perfection. A budget that recovers from small misses is more useful than a rigid plan that collapses.

Use a payday routine to make the budget automatic

The biggest improvement for anyone learning how to budget 2000 salary income is to stop making the same decision every day. A small income budget works better when the important transfers happen before the money mixes with daily spending. That means payday should have a short routine: bills, savings, debt, weekly spending, then optional extras.

If you are paid twice per month, a $400 savings target can become two $200 transfers. If that is too aggressive, start with two $75 or $100 transfers and raise the amount later. The exact number matters less than the order. The savings transfer should happen before the weekend, before shopping, and before subscriptions or small purchases blur the budget.

| Payday step | Action | Example on $2,000/month | Purpose |

|---|---|---|---|

| 1 | Confirm income received | $1,000 if paid twice monthly | Start from real cash, not expected cash. |

| 2 | Move rent and fixed bills | $500-$650 per paycheck | Protect essentials first. |

| 3 | Automate savings | $100-$200 per paycheck | Make progress before discretionary spending. |

| 4 | Set weekly spending caps | $75-$125 per week | Prevent mid-month leakage. |

| 5 | Review one category | Food, transport, subscriptions, or debt | Improve the system gradually. |

This routine also removes emotional budgeting. Instead of asking whether you feel motivated, you follow the same sequence. Bills are protected. Savings happens. Weekly spending is clear. If something breaks, you know exactly which category needs adjustment.

A simple checking account setup can help. One account handles bills. One account handles spending. One account holds savings. Some people use separate savings buckets for emergency fund, annual bills, car repairs, gifts, or future investing. The more precise the buckets, the less likely you are to spend money that had a different job.

Handle debt before aggressive investing

Debt changes the budget order. If you have high-interest credit card debt, the best return may be paying it down. If debt interest is low and payments are manageable, you may be able to save, pay debt, and invest in small amounts at the same time. The right order depends on interest rates and emergency savings.

A practical order is to build a starter emergency fund first, pay minimums on all debt, then send extra money to the highest-interest balance. Some people prefer the snowball method, where the smallest balance is paid first for motivation. Others prefer the avalanche method, where the highest interest rate is paid first to reduce total interest.

Avalanche method

Best when you want the mathematically efficient path. Pay extra on the highest interest rate while keeping all other payments current.

Snowball method

Best when motivation matters most. Pay extra on the smallest balance first, then roll that payment into the next debt.

On a $2,000 salary, the debt plan should not starve the emergency fund. Without a small cash buffer, one surprise expense can restart the debt cycle. A balanced version might send $100 to starter savings, $200 to extra debt payoff, and $100 to longer-term savings until the first buffer is complete.

Build a starter emergency fund before chasing the perfect plan

A starter emergency fund is the first layer of budget protection. It does not need to be huge. It needs to exist. For a $2,000 monthly income, a $500 to $1,000 starter fund can stop small emergencies from becoming credit card debt. After that, work toward one to three months of essential expenses.

If your goal is saving $400 per month, the first two or three months could go entirely toward emergency savings. Once the starter buffer is in place, the $400 can be split. For example, $150 to emergency savings, $150 to debt payoff, and $100 to investing. The split can change as your situation improves.

Emergency money should usually stay in a safe, accessible account. It is not the money to use for volatile investments. The purpose is stability, not maximum return. Once the emergency fund is stable, investing becomes easier because you are less likely to sell during a bad month.

Three examples of how to budget 2000 salary income

There is no single perfect $2,000 budget because living costs vary. The same income can create very different outcomes depending on rent, transport, debt, and support from family or roommates. These examples show how the budget changes while the logic stays the same.

Shared housing, low debt

Rent and utilities are $750, transport is $120, and debt minimums are low. This person may be able to save $400 per month quickly. The best move is to automate the full transfer, build a starter emergency fund, then split new savings between cash and investing.

Solo renter, tight city budget

Rent and utilities are $1,050, transport is $180, and groceries are rising. A $400 savings target may not fit at first. A better starting point could be $150 to $250 per month while the person negotiates bills, adds income, or searches for lower fixed costs.

Debt-heavy budget

Rent is manageable, but credit card minimums and personal loans consume cash flow. This person should build a small emergency fund, pay minimums, then attack high-interest balances before sending a large amount to investing.

These examples matter because they prevent false comparison. Someone with shared housing and no debt is not playing the same game as someone with high rent and old balances. If your budget cannot save $400 today, the question is not whether you failed. The question is which constraint needs work first.

When you ask how to budget 2000 salary income, the answer should include both a target and a path. The target might be saving $400. The path might be saving $150 now, cutting $80 in recurring bills, adding $100 of side income, and redirecting a $70 debt payment once it is paid off. That path is more useful than pretending the perfect number appears immediately.

Use sinking funds so surprise bills do not destroy the budget

One reason a $2,000 budget feels impossible is that people plan only the regular month. Then a car repair, annual fee, dentist bill, school expense, gift, clothing purchase, or insurance renewal arrives and the budget looks broken. Those expenses are not always emergencies. Many are predictable but irregular.

A sinking fund solves that problem by turning irregular costs into small monthly amounts. If car repairs usually cost $600 per year, save $50 per month. If holiday gifts usually cost $480, save $40 per month. If annual subscriptions cost $240, save $20 per month. The monthly budget becomes calmer because the future bill is already being funded.

| Sinking fund | Annual estimate | Monthly amount | Why it helps |

|---|---|---|---|

| Car repairs or transit extras | $600 | $50 | Prevents one repair from becoming credit card debt. |

| Gifts and holidays | $480 | $40 | Keeps generosity from disrupting rent or savings. |

| Clothing and personal care | $360 | $30 | Makes non-monthly needs visible. |

| Annual subscriptions and fees | $240 | $20 | Stops yearly renewals from feeling unexpected. |

This is especially important when you learn how to budget 2000 salary income because there is not much room for surprises. Sinking funds are not extra spending. They are delayed spending made visible. They can also make the $400 savings goal more honest: part of the $400 may be emergency savings, part may be sinking funds, and part may become investing once the budget is stable.

If income is too tight, side income can accelerate the plan, but it should have rules before it arrives. For example, the first $100 of monthly side income can go to emergency savings, the next $50 can go to debt, and anything above that can support flexible spending. Without a rule, extra money often disappears into the same categories that were already leaking.

When a $2,000 budget can start investing

Investing on a small income is possible, but it should not compete with rent, food, minimum debt payments, or a starter emergency fund. Once the basics are stable, even $50 to $100 per month can build the habit. The first investing goal is not to look rich. It is to make regular contributions feel normal.

If you can save $400 per month, you do not need to invest all $400 immediately. You might save $250 in cash until the emergency fund is ready and invest $150 monthly for long-term growth. Later, when the emergency fund is complete, more of the same $400 can move into recurring investments.

| Budget stage | Cash savings | Debt payoff | Investing | Tool to use |

|---|---|---|---|---|

| No emergency fund | $300-$400 | Minimums | $0-$50 | WhatIfBudget |

| Starter buffer ready | $150-$250 | $100-$200 | $50-$100 | Compound Interest Calculator |

| Debt controlled | $50-$150 | Minimums or targeted extra | $200-$300 | DCA Calculator |

| Stable surplus | Maintenance | As needed | $300-$400+ | Investment Simulator |

The key is progression. A beginner budget starts with protection. A stable budget starts building wealth. A strong budget compares strategies. That is the WhatIfInvested path: simulate the cash flow, compare the options, and understand what the numbers actually mean.

If your budget can only invest $50 per month, that is still a start. If it can invest $150 per month, the habit becomes more meaningful. If it can invest $300 or more, scenario testing becomes valuable because fees, assumptions, time horizon, and market behavior can change the outcome. The premium path should only matter when the user has a real recurring amount to compare.

Use WhatIfInvested to turn a $2,000 budget into a plan

The article gives the structure, but the numbers become more useful when you test them. Start with budget capacity, then move to future-value projection, then compare recurring investing scenarios.

WhatIfBudget

Find monthly surplus, spending pressure, savings capacity, and the next best move.

Compound Interest Calculator

Project what recurring savings could become over a fixed timeline.

DCA Calculator

Model recurring investing once cash flow and emergency savings are stable.

Budget mistakes to avoid on a $2,000 salary

Using a rule that ignores rent

A 50/30/20 rule is useful only if the fixed costs fit. If rent is too high, use a transitional rule while you work on housing, income, or debt.

Saving whatever is left over

Leftover savings usually disappears. Automate the savings transfer near payday, even if the first version is only $50 or $100.

Forgetting irregular expenses

Annual fees, gifts, clothing, repairs, and medical costs should be divided into monthly sinking funds so they do not surprise the budget.

Investing before a starter buffer

A small cash buffer reduces the chance that one emergency forces you to sell investments or use high-interest debt.

Trying to change every habit at once

Pick one large fixed cost, one weekly spending cap, and one automatic transfer. Build from there.

Copying a budget without adjusting for location

A $2,000 salary stretches differently in a low-cost town than in a high-rent city. Use templates as a starting point, then adapt for housing, transport, taxes, and family obligations.

Treating side income as spending money only

Side income can help, but it works best when part of it is assigned before it arrives. For example, the first $100 can go to emergency savings and the rest can support flexibility.

Frequently asked questions

Can you really save $400 on a $2,000 salary?

Yes, but only if fixed costs are controlled. Saving $400 is a 20% savings rate. If rent, debt, or transport are high, start with $100 to $250 and increase as the budget improves.

What is the best budget rule for a $2,000 income?

A 60/20/20 or 60/30/10 rule may be more realistic than 50/30/20 when income is tight. The best rule is the one that covers essentials, avoids new debt, and protects at least one automatic savings transfer.

How much rent can I afford on $2,000 a month?

Keeping rent around $600 to $800 makes saving easier. If rent is above $1,000, the budget may still work, but saving $400 will be much harder without lower transport costs, side income, or reduced debt.

Should I save or pay off debt first?

Build a small emergency fund first, pay minimums on all debt, then prioritize high-interest debt. After that, balance savings, debt payoff, and investing based on your goals.

How do I stop overspending mid-month?

Use weekly caps. Divide groceries, personal spending, and eating out into weekly amounts. A weekly limit is easier to manage than trying to remember the whole monthly budget.

When should I start investing on a small salary?

Start after essential bills, minimum debt payments, and a starter emergency fund are stable. Even $50 to $100 per month can build the investing habit.

Which WhatIfInvested tool should I use first?

Start with WhatIfBudget to find your monthly surplus. Then use the Compound Interest Calculator or DCA Calculator when part of that surplus can become savings or investing.

What if my budget does not fit the template?

Use the template as a diagnostic tool. If the numbers do not fit, identify the constraint: housing, debt, income, transport, or flexible spending. Then adjust one lever at a time.

The best $2,000 budget is simple enough to repeat

If you want to save $400 per month on a $2,000 salary, the budget needs three things: controlled fixed costs, weekly spending limits, and an automatic savings transfer. If $400 is not realistic yet, start smaller and protect the habit. A consistent $150 transfer is better than an impressive plan that fails after one month.

Once the budget creates surplus, the next step is to give that surplus a job. Some belongs in emergency savings. Some may go to debt payoff. Some can eventually become long-term investing. The goal is not only to survive on $2,000. The goal is to turn a tight budget into a system that creates options.

Educational content only. This article is not financial, tax, or investment advice. Budget decisions depend on income, expenses, debt, tax situation, account rules, risk tolerance, location, and personal goals.