Compound Interest With Monthly Contributions

Compound interest with monthly contributions shows how a starting balance, recurring deposits, time and return assumptions can work together. The monthly contribution adds new fuel, while compounding lets past growth create more future growth.

Compound interest with monthly contributions: what it shows

The projection separates the money you add from the growth those deposits may earn over time. That makes it easier to see whether your future value depends mostly on savings behavior, investment return, time or a mix of all three.

Quick answer: how compound interest with monthly contributions works

Compound interest with monthly contributions works by adding new money at regular intervals while the existing balance continues to earn returns. Each month, the contribution increases the capital base. Over time, returns can begin earning additional returns of their own, which is why long horizons can make the growth curve steeper.

The key is that contributions and compounding are different forces. In the early years, your monthly deposits often do most of the work. Later, if the balance becomes large enough and returns stay invested, compounding may contribute more of the yearly growth. A good calculator should show both total invested and interest earned so you can see which force is driving the result.

On this page

The inputs that matter most

The first input is the starting balance. This is the amount already available before the contribution plan begins. A starting balance gives compounding something to work on immediately. Someone starting with $20,000 and adding $300 per month will see a different curve from someone starting at zero and adding the same amount.

The second input is the monthly contribution. This is the repeatable deposit that keeps the plan moving. It should come from real cash flow, not from a number that only looks good in a spreadsheet. A sustainable $250 monthly contribution is usually stronger than an unrealistic $800 contribution that stops after a few months.

The third input is time. Time gives both existing money and future deposits more opportunities to grow. A monthly contribution plan over three years is mostly a savings habit. The same plan over twenty or thirty years can become a compounding system.

The fourth input is the expected annual return. This assumption has a major impact on the ending value, but it is also the easiest input to abuse. If the plan only works with a very optimistic return, the plan is fragile. Test lower returns first.

The fifth input is compounding frequency. Many investing calculators use annual, monthly or daily compounding assumptions. For long-term investment planning, the exact frequency usually matters less than contribution amount, time horizon, fees and whether returns remain invested.

Monthly contribution examples

Examples are helpful because compounding can feel abstract until you connect it to a real monthly deposit. The exact result depends on the calculator assumptions, but the pattern is consistent: larger monthly deposits, longer time horizons and higher returns usually increase the final value. The risk is that higher return assumptions may also imply more volatility.

| Monthly contribution | Typical use case | What it teaches | Useful next step |

|---|---|---|---|

| $50 to $100 | Beginner habit building | Small deposits can still build discipline. | Focus on consistency and low fees. |

| $200 to $400 | Early investing plan | Contribution behavior starts to matter. | Run 10-year and 20-year projections. |

| $500 to $1,000 | Serious wealth-building plan | Return assumptions and allocation matter more. | Compare conservative and base cases. |

| $1,000+ | High-savings household | Taxes, fees and planning workflow become more important. | Use advanced scenario tools. |

A person investing $100 per month should not dismiss the plan because the early years look slow. The first job is to build the habit. A person investing $750 per month should pay more attention to assumptions because the stakes are higher. A small error in return, fees or tax treatment can compound into a larger difference.

If you do not know how much you can afford to contribute, start with WhatIfBudget or the guide on how much to save monthly. A compound projection is only as useful as the monthly amount behind it.

How to read the result

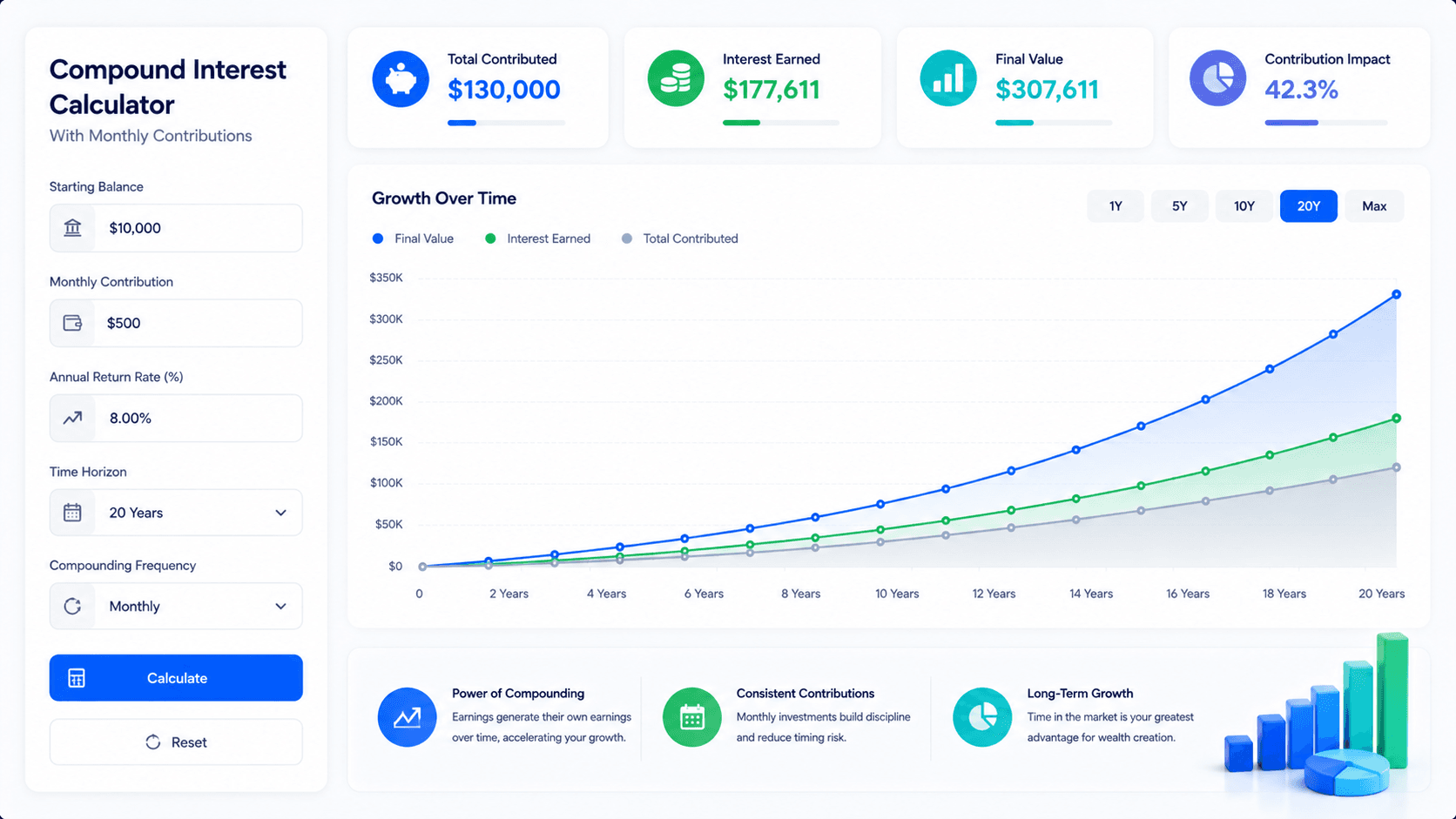

The final value is the number most people notice first, but it is not the only number that matters. A good projection should show total contributions, interest earned and ending value. Total contributions show the money you added. Interest earned shows the growth created by the model. The ending value combines both.

In the early years, total contributions may dominate the result. That is normal. Compounding often looks underwhelming at first because the balance is still small. Later, as the account grows, returns can become a larger part of each year’s increase. This shift is one of the main reasons long-term investing can become powerful.

It also helps to read the yearly table. The yearly breakdown shows when the balance begins to accelerate, when interest earned becomes meaningful and how much of the final value came from repeated deposits. A single final number hides this progression. A yearly view makes the story easier to understand.

Finally, compare multiple scenarios. Run a conservative case first, then a base case, then an optimistic case. If the plan only looks good in the optimistic case, the monthly contribution, time horizon or goal may need adjustment.

Why time changes the contribution story

Time is the part of compound interest that is easiest to underestimate. A monthly contribution made today has more time to grow than a contribution made ten years from now. That means early deposits can have a larger long-term impact than later deposits, even when the dollar amount is the same.

This does not mean late contributions are useless. It means the growth engine changes over time. Early on, the plan depends heavily on what you add. Later, the existing balance may become large enough that returns begin to matter more. A calculator can show this handoff by comparing total contributions with interest earned year by year.

For example, an investor adding $300 per month for five years is mostly building a contribution base. The same investor contributing for twenty-five years is building both a contribution base and a compounding base. The monthly amount may be unchanged, but the time horizon changes the role each deposit plays.

The most useful lesson is behavioral. Starting earlier can reduce the pressure to choose an aggressive return assumption. If time is on your side, the plan can rely more on consistency and less on optimism. If time is short, the monthly contribution amount may matter more than the compounding assumption.

Beginning-of-month vs end-of-month contributions

Some calculators assume contributions happen at the end of each month. Others assume deposits happen at the beginning. This detail can create a difference because earlier deposits have slightly more time to earn returns. Over one month, the difference is small. Over decades, it can become more noticeable.

In real life, the best contribution timing is usually the timing you can automate. If you are paid on the first of the month, investing shortly after payday may be practical. If your bills come first, investing later may be safer. The perfect mathematical date is less important than the schedule that does not create cash-flow stress.

For most long-term investors, the exact monthly day is not the main driver. Contribution amount, time horizon, allocation, fees and behavior usually matter more. Still, it is useful to know what the calculator assumes. If two calculators produce slightly different results, contribution timing may be one reason.

Increasing monthly contributions over time

Many people do not keep the same monthly contribution forever. Income can rise, debt can fall, family expenses can change and savings goals can become more serious. A realistic plan may start with $150 per month, then increase to $250, $400 or more over time.

A basic compound interest calculator may use one fixed contribution amount. That is still useful as a baseline. But if you expect contributions to increase, you should run separate scenarios. One scenario can model your current contribution. Another can model a future higher contribution. The difference shows how much contribution increases may matter.

Increasing contributions can be powerful because the habit is already built. The investor does not need to redesign the whole plan. They simply raise the monthly deposit when cash flow improves. This is often easier than trying to start with a contribution that is too large from day one.

For advanced planning, contribution increases are one reason to use a deeper workflow. If your plan includes changing deposits, different phases, fees, withdrawals or saved scenarios, Premium tools may be more useful than a single fixed-contribution projection.

Choosing realistic return assumptions

Return assumptions can make compound interest projections look exciting, but they can also make them misleading. A high annual return creates a larger ending value, but it may not be realistic for the asset or time horizon. A lower return may feel less impressive, but it may be a better planning baseline.

For long-term investing, many people test three cases. A conservative case uses a lower return to reflect weak markets, higher fees or inflation. A base case uses a moderate assumption. An optimistic case shows what could happen if returns are stronger. The value is not in guessing the exact future. The value is in seeing how sensitive the result is to the assumption.

Inflation also matters. A future balance may look large in nominal dollars but have less purchasing power than the same number today. If your goal is retirement or long-term financial independence, consider testing a lower real return or mentally discounting the final value.

Investor.gov’s overview of compound interest calculators is a useful external reference because it reinforces the same idea: inputs such as time, deposits and rate of return shape the projection. The calculator is a planning aid, not a guarantee.

Compound interest calculator vs DCA calculator

A compound interest calculator and a DCA calculator can both use monthly contributions, but they answer different questions. A Compound Interest Calculator is best for smooth future-value planning. It helps you understand what could happen under a steady return assumption.

A DCA Calculator is better when your main question is about recurring investing behavior and contribution schedules. The article on DCA Calculator With Monthly Contributions is specifically about using recurring deposits to model a DCA plan.

For historical market paths, use the Investment Simulator. A compound interest calculator uses smooth assumptions. A simulator shows real historical volatility, timing risk and drawdowns. The tools work best together when each one answers the right question.

| Question | Best tool | Why |

|---|---|---|

| How could my balance grow with monthly deposits? | Compound Interest Calculator | Best for future-value planning. |

| How do recurring investments behave as DCA? | DCA Calculator | Best for contribution strategy. |

| How did an asset perform historically? | Investment Simulator | Best for real market paths. |

| How much can I afford monthly? | WhatIfBudget | Best before projecting growth. |

When monthly contributions are not enough

A projection may show that your current monthly contribution does not reach the target. That is useful information. It means the plan needs a change before time passes. The possible levers are contribution amount, timeline, expected return, fees, goal size and starting balance.

If the contribution is too small, the safest fix is often to improve cash flow rather than chase a higher return. That may mean reducing expenses, increasing income or using a budget planner to find investable surplus. If the timeline is short, more contribution usually matters more than compounding.

If the return assumption is too low for the goal, increasing risk may appear tempting. But higher expected return usually comes with higher volatility. A plan that requires aggressive risk may be harder to follow during downturns. The calculator can show the gap, but it cannot decide your risk tolerance.

If the goal is flexible, lowering the target may be more realistic than forcing a fragile plan. A strong plan is not the one with the biggest final value. It is the one that survives real income, real expenses and real market uncertainty.

Examples by investor profile

The right way to use compound interest with monthly contributions depends on the person using the calculator. A student, a new investor, a high-savings household and a late starter do not need the same interpretation. The inputs may look similar, but the decision behind them is different.

Beginner with a small monthly amount

A beginner contributing $50 to $100 per month should focus on consistency and low friction. The early projection may not look dramatic, but the goal is to build the habit and understand how the calculator works. This investor should avoid high fees because costs can be large relative to the contribution.

Paycheck investor with steady surplus

A paycheck investor contributing $250 to $600 per month can use the calculator to test realistic long-term goals. This person should compare conservative and base returns, then ask whether the monthly amount can survive normal expenses. If the answer is yes, automation can turn the plan into a repeatable system.

High-savings household

A household contributing $1,000 or more per month should pay close attention to taxes, fees, asset allocation and scenario design. At this level, the monthly habit is already meaningful. The next improvement may come from better assumptions, account location and planning discipline.

Late starter

A late starter has less time for compounding to work, so contribution amount becomes more important. This investor should avoid relying on unrealistic returns to close the gap. It may be better to increase contributions, extend the timeline, reduce the target or combine several changes.

Fees, taxes and inflation reduce real compound growth

Compound interest projections often look cleaner than reality. Real investors may face fund fees, advisory fees, tax drag, trading spreads, currency conversion and inflation. Each friction can reduce the final value. The longer the timeline, the more those small differences can compound.

Fees are especially important because they are recurring. A 1% annual cost may not feel large in one year, but it can create a meaningful gap over decades. Lower-cost funds and efficient accounts can preserve more of the growth for the investor.

Taxes depend on account type and location. A tax-advantaged account may allow growth to compound more efficiently than a taxable account. A taxable account may create annual tax obligations from dividends, interest or realized gains. A simple calculator may not include all of those details.

Inflation affects purchasing power. A future value of $500,000 may sound large, but what matters is what it can buy when you reach that date. For long-term planning, consider using a lower real return or comparing nominal results with inflation-adjusted expectations.

A practical workflow before using the calculator

Start by defining the goal. Are you estimating retirement savings, a long-term investment account, an education fund, a house down payment or a general wealth-building plan? The goal affects the timeline, risk level and monthly amount.

Next, confirm the monthly contribution. If the amount is uncertain, use a budget tool first. A projection based on a fictional contribution can lead to false confidence. The best monthly amount is the one that survives ordinary life.

Then choose three return assumptions. Use a conservative case, a base case and an optimistic case. Do not begin with the optimistic case. A plan that works under conservative assumptions is stronger than a plan that only works when everything goes well.

Finally, write down the result and the action. A calculator should lead to a decision: automate a contribution, lower the target, increase savings, compare tools or revisit the plan later. Without a next action, the projection is just a chart.

- Define the financial goal and time horizon.

- Confirm a realistic monthly contribution.

- Run conservative, base and optimistic assumptions.

- Compare total invested, interest earned and final value.

- Choose one next action based on the result.

It also helps to separate saving goals from investing goals. If the money is needed soon, the priority may be stability rather than compound growth. If the money is for a long-term goal, market exposure may be more reasonable, but volatility becomes part of the plan. The calculator can support both conversations, but the time horizon should decide how much risk belongs in the assumption.

That distinction keeps the projection grounded. A short-term savings goal should not depend on an aggressive investment return. A long-term investing goal should not be judged only by the first few years. Matching the tool to the timeline makes the final number more useful.

Common mistakes with compound interest and monthly contributions

The first mistake is assuming smooth returns. Real investments do not grow in a perfect line. A calculator may use a steady annual return, but the market will not. Treat the result as a planning estimate, not a promise.

The second mistake is ignoring fees. Fund expenses, advisory fees, platform costs and taxes can reduce the ending value. Even a small annual cost can matter over a long horizon.

The third mistake is choosing a monthly contribution that does not fit the budget. If the deposit is too high, the plan may fail quickly. A smaller deposit that continues for years is often more powerful than a larger deposit that stops.

The fourth mistake is looking only at the final value. Read total invested, interest earned and yearly growth. Those details show whether the plan depends mostly on your deposits or on investment growth.

The fifth mistake is starting too late and expecting return to fix the gap. Higher returns may help, but time is the cleanest compounding advantage. If time is limited, focus on contribution amount and realistic goals.

Free vs Premium workflow

The free Compound Interest Calculator is the right starting point when you need a clean future-value projection. It is useful for testing a starting balance, recurring contribution, timeline and return assumption. It helps you understand the basic math before the plan becomes more complex.

Premium becomes more relevant when the decision includes multiple portfolios, fees, withdrawals, saved scenarios, exports or deeper comparisons. If you need to compare several plans and keep the assumptions organized, the Premium DCA Calculator can support historical scenario work, while the Premium Compound Growth Planner is better for forward-looking contribution schedules, inflation assumptions and export-ready growth projections.

Frequently asked questions

What is compound interest with monthly contributions?

Compound interest with monthly contributions means a starting balance and recurring monthly deposits both participate in growth. Over time, returns can earn additional returns, which can increase the final value.

How do monthly contributions affect compound interest?

Monthly contributions increase the balance that can earn future returns. In early years, deposits often do most of the work. Later, compounding can become a larger part of the growth.

What calculator should I use?

Use the Compound Interest Calculator for smooth future-value projections. Use the DCA Calculator for recurring investment strategy. Use the Investment Simulator for historical market paths.

How much should I contribute monthly?

The best monthly contribution is the amount you can repeat after expenses, debt payments, emergency savings and normal cash flow needs. Use a budget tool first if you are unsure.

Does compounding guarantee investment growth?

No. Compounding can increase growth when returns are positive and reinvested, but investments can lose value. A projection is an estimate, not a guarantee.

Should I include inflation?

Yes, especially for long-term goals. Inflation reduces purchasing power, so a future balance may be worth less than the same number today.

Is monthly compounding the same as monthly contributions?

No. Monthly compounding describes how often returns are applied. Monthly contributions describe how often you add new money. Both can affect the projection.

When should I use Premium?

Use Premium when you need multiple scenarios, portfolio assumptions, fees, withdrawals, saved plans or exportable reports. The free calculator is enough for a simple projection.