Portfolio Backtesting for Beginners

Portfolio backtesting for beginners is about testing an allocation before you trust it with real money. Instead of asking whether one asset went up, you test how a mix of assets behaved through growth periods, crashes, recoveries and long flat stretches.

This guide shows how to build a simple portfolio test, read the results clearly, avoid beginner mistakes and know when a free simulator is enough versus when a Premium workflow becomes useful.

Portfolio backtesting for beginners: what it means

Portfolio backtesting means replaying a portfolio through historical market data. You choose assets, weights, a time period, contribution rules and rebalancing assumptions. The simulator then shows how that portfolio would have grown, fallen and recovered.

For beginners, the goal is not to find a perfect portfolio. The goal is to understand trade-offs. A portfolio with higher final value can still be harder to hold if the drawdowns are deep. A smoother portfolio can feel easier to follow even if the ending balance is lower.

Quick answer: how to backtest a portfolio

To backtest a portfolio, choose a small set of assets, assign a target weight to each one, select a historical period, decide whether you are investing a lump sum or recurring contributions, and review both return and risk. The most important beginner mistake is judging the portfolio only by ending value.

A better beginner workflow is to compare at least two portfolios. For example, you might test a 100% stock portfolio against a 70% stock and 30% bond portfolio. The first may produce higher long-term return in some periods, but the second may have smaller drawdowns and a smoother path. The answer depends on the decision you are trying to make.

On this page

Start with the free Investment Simulator

The best beginner path is to run one clean portfolio backtest before opening a larger planning workflow. Start with the free Investment Simulator, compare one simple allocation against one alternative, then decide whether the result creates a real planning question.

The inputs every beginner should define first

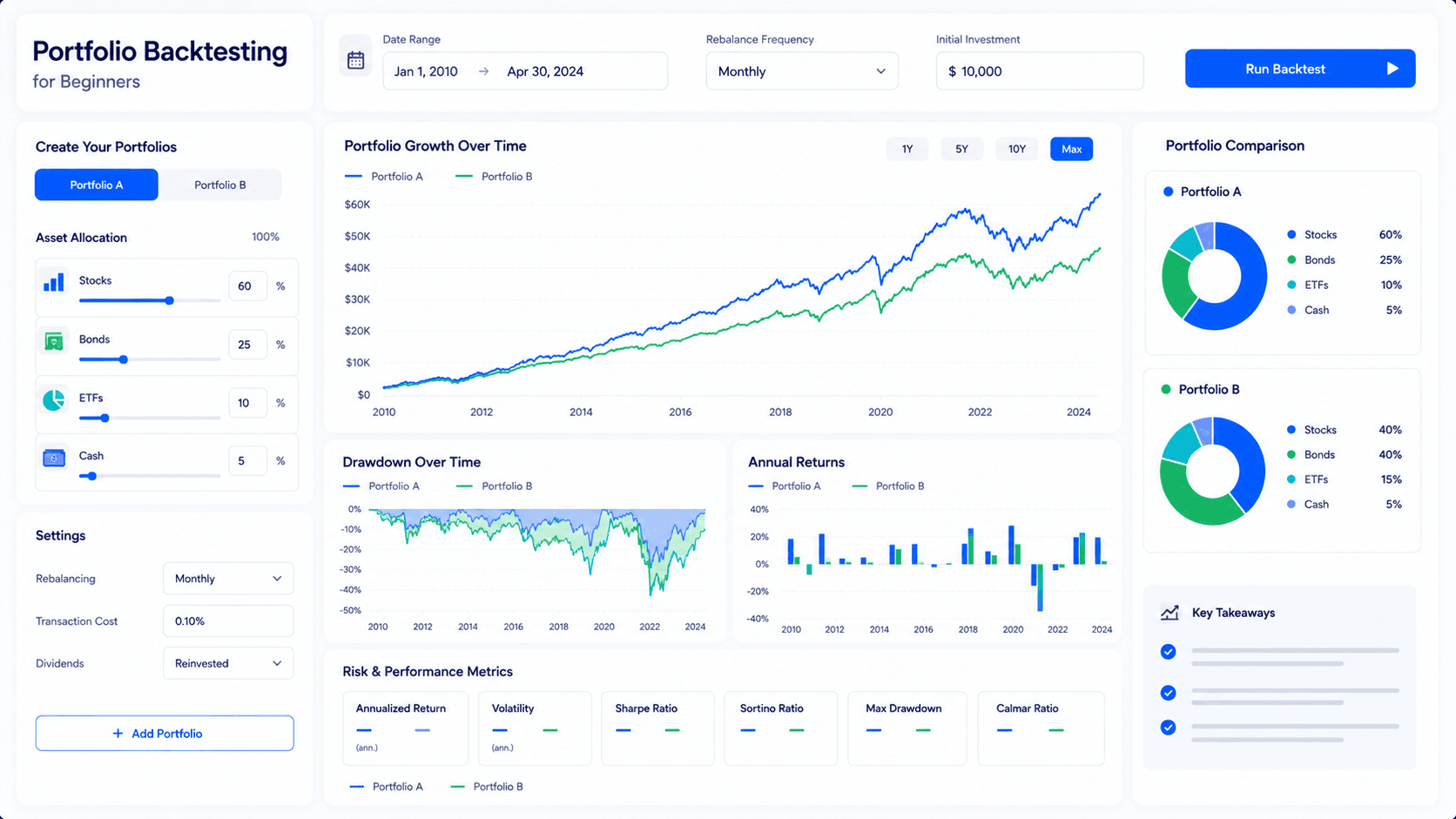

The first input is the portfolio list. A beginner portfolio should usually start with a small number of broad assets, such as a stock ETF, a bond ETF and cash. This keeps the test readable. If you add too many assets too early, it becomes difficult to know which decision changed the result.

The second input is target weight. A target weight is the intended percentage of the portfolio assigned to each asset. A 60/40 portfolio means 60% stocks and 40% bonds. A three-asset portfolio might use 70% stocks, 20% bonds and 10% cash. The weights matter because they shape both growth and risk.

The third input is the test period. A backtest from 2010 to 2021 tells a very different story from a backtest that includes 2008, 2020 or 2022. Beginners should test at least one full cycle when possible, including a difficult period. A portfolio that only looks good in good markets has not been tested hard enough.

The fourth input is contribution behavior. Are you investing once at the beginning, adding monthly, or adding only when cash is available? A portfolio backtest with recurring contributions can produce a very different emotional experience from a lump sum backtest. Contributions can soften timing risk, but they can also hide poor portfolio design if you only look at final balance.

The fifth input is rebalancing. Rebalancing means moving the portfolio back toward target weights. If stocks rise quickly, a 60/40 portfolio might become 75/25. Rebalancing sells some of what grew and buys what lagged. This can reduce risk, but it can also lower returns during long trends. Beginners should test both no rebalancing and annual rebalancing before assuming one is better.

Asset allocation is the decision you are really testing

Many beginners think portfolio backtesting is mainly about choosing the best ticker. In reality, the biggest decision is often allocation. Allocation controls how much of the portfolio is exposed to growth assets, defensive assets and cash-like stability. A single high-return asset can make a chart look exciting, but a portfolio needs to survive the periods when that asset performs badly.

A stock-heavy portfolio usually aims for higher growth. It can also create larger drawdowns. A bond-heavy portfolio may reduce volatility, but it can lag during strong equity markets and it can still lose value when rates move sharply. A cash allocation can reduce stress and provide flexibility, but too much cash can weaken long-term growth after inflation.

For a practical beginner test, compare three simple allocations. Portfolio A can be aggressive, such as 100% equities. Portfolio B can be balanced, such as 70% equities and 30% bonds. Portfolio C can be conservative, such as 50% equities, 40% bonds and 10% cash. The purpose is not to crown a universal winner. The purpose is to understand which trade-off fits your time horizon and tolerance for drawdown.

The concept of asset allocation is important enough that Investor.gov maintains a plain-language explanation of asset allocation. That kind of external grounding matters because backtesting should not be separated from basic portfolio construction.

The metrics that matter more than final value

Final value is the first number most people check, but it is not enough. A portfolio can finish with a high ending balance while producing a painful path. If the drawdown would have caused you to quit, the ending value is not realistic for your behavior.

| Metric | What it tells you | Beginner interpretation |

|---|---|---|

| Final value | Ending portfolio value after the test period. | Useful, but incomplete without risk. |

| Total return | Overall percentage gain or loss. | Good for comparing portfolios over the same period. |

| Maximum drawdown | Largest peak-to-trough decline. | Shows the worst pain point in the historical test. |

| Recovery time | How long it took to regain a previous high. | Helps you understand patience required. |

| Volatility | How much the portfolio moved around. | Useful for judging emotional difficulty. |

| Contribution impact | How much growth came from deposits versus returns. | Important for DCA and monthly investing plans. |

A beginner should not obsess over every advanced metric. Start with final value, drawdown, recovery time and contribution impact. Those four numbers answer a very practical question: did the portfolio grow, how bad did it feel, how long did it take to recover and how much of the result came from your savings behavior?

For a focused downside review, a max drawdown calculator can help separate the return story from the worst decline and recovery period.

Beginner portfolio backtesting examples

Example one is a simple growth portfolio. Imagine a user compares 100% stocks against a balanced allocation. The stock portfolio may win over a long growth period, but it may also fall more during crashes. If the investor is young and investing monthly, the drawdown may be acceptable. If the investor needs the money soon, the same drawdown may be unacceptable.

Example two is a retirement transition portfolio. A user nearing retirement might compare 80/20, 60/40 and 40/60 allocations. The main question is no longer just growth. The question becomes whether the portfolio can reduce large losses while still keeping enough growth to fight inflation. Backtesting helps make that trade-off visible.

Example three is a contribution portfolio. A beginner with limited capital may want to know whether adding $300 per month to a diversified portfolio historically produced meaningful progress. This is where the free Investment Simulator and the DCA Calculator work together. The simulator helps with historical portfolio behavior, while the DCA calculator helps with recurring contribution planning.

How portfolio backtesting fits the WhatIfInvested workflow

The WhatIfInvested workflow is simple: Simulate, Compare, Understand. Portfolio backtesting belongs in the middle of that system. You simulate an allocation, compare it against alternatives and then understand whether the result fits your real-life plan.

The free simulator is the right starting point when the question is straightforward. For example, you may want to compare one or two assets, test a historical period and understand how a recurring investment might have performed. A beginner does not need a complex premium workflow on day one. The first win is clarity.

Premium becomes relevant when the number of scenarios grows. If you need to compare several portfolios, use custom weights, keep assumptions organized, model exports, or revisit saved scenarios, the value of a structured workflow increases. That is why this article introduces Premium only after the beginner understands the basic portfolio test.

How to choose the right backtesting period

A backtest period should match the decision. If you are testing a long-term retirement allocation, a five-year window is usually too short. If you are testing a short-term cash reserve strategy, a thirty-year window may be less relevant. The time window should reflect how long the portfolio is expected to be used.

Beginners should avoid the temptation to pick only favorable start dates. Starting a test right after a major market crash can make almost every strategy look strong. Starting at the top of a bubble can make almost every strategy look worse. A more honest approach is to run several start dates and compare the range of outcomes.

This is why the article How to Backtest Your Investment Strategy remains important. It covers the broader workflow and methodology. This beginner article keeps the focus on portfolio construction, but the deeper guide helps users understand data quality, assumptions and testing discipline.

How rebalancing changes the result

Rebalancing is one of the most misunderstood parts of portfolio backtesting for beginners. It sounds technical, but the idea is simple. If your target is 70% stocks and 30% bonds, and stocks rise enough to become 85% of the portfolio, rebalancing moves the portfolio back toward 70/30.

Rebalancing can help control risk. It can also force you to sell some of the asset that recently performed well and buy the asset that lagged. In a trending market, that can reduce returns. In a volatile market, it can help maintain discipline. The result depends on the period, the asset mix and the rebalancing rule.

For a beginner, annual rebalancing is often a reasonable first test. It is simple to understand and avoids over-trading. After that, you can test no rebalancing and threshold-based rebalancing. The point is not to create the most complicated rule. The point is to understand whether rebalancing changes the risk enough to justify the behavior.

Common mistakes beginners make with portfolio backtesting

The first mistake is overfitting. Overfitting means building a portfolio that looks perfect in one historical window because you adjusted it to that exact past. A portfolio that wins one chart may not be robust. Beginners should prefer simple portfolios that work reasonably well across several periods instead of complex portfolios that only win one test.

The second mistake is ignoring inflation. A portfolio can grow in nominal dollars while losing purchasing power. This matters most for long periods. If the backtest is meant to support retirement, education savings or long-term wealth planning, inflation should be part of the interpretation.

The third mistake is ignoring fees and taxes. A no-fee backtest may be useful for learning, but real portfolios often include fund expenses, transaction costs and tax consequences. A beginner does not need to model every detail immediately, but they should understand that real-world results may be lower than clean historical charts.

The fourth mistake is comparing portfolios across different assumptions. If Portfolio A starts in 2009 and Portfolio B starts in 2015, the comparison is not fair. If one portfolio includes dividends and another does not, the comparison is not fair. Keep assumptions consistent before drawing conclusions.

The fifth mistake is treating past performance as a prediction. Backtesting helps you understand what happened under historical conditions. It does not tell you what must happen next. The best use of a backtest is to improve decision quality, not to pretend the future is known.

A practical beginner workflow before using the simulator

- Write the question in one sentence. For example: "Would a balanced portfolio have been easier to hold than an all-stock portfolio?"

- Choose two or three portfolios to compare. Keep the assets and weights simple.

- Choose a period that includes both growth and stress if possible.

- Decide whether the test uses lump sum investing, monthly contributions or both.

- Run the test and record final value, maximum drawdown, recovery time and contribution impact.

- Change one assumption at a time. If you change everything at once, you cannot tell what mattered.

- Use the result to make a clearer decision, then save or document the assumptions.

This workflow keeps the backtest useful. It also prevents the most common beginner trap: running many simulations without a decision framework. More charts are not automatically more insight.

How to compare two portfolios without fooling yourself

Portfolio comparison is where many beginner backtests become misleading. The problem is not the simulator. The problem is that the comparison is often unfair. If one portfolio uses a different start date, different contribution schedule, different dividend treatment or different rebalancing rule, the result is no longer a clean comparison.

Start by making Portfolio A and Portfolio B share the same test period. If the first portfolio starts in January 2010 and the second starts in January 2015, you are comparing two different market environments. The portfolio that starts later may avoid a weak period, or it may miss a strong period. Either way, the conclusion becomes less useful.

Next, keep contribution rules identical. If Portfolio A receives monthly contributions and Portfolio B is tested as a lump sum, the result may reflect the funding method more than the asset allocation. That can be a valid test if your question is about contribution timing, but it is not a clean test of portfolio design. For allocation comparison, keep deposits the same.

Then make sure the benchmark is simple. A beginner does not need ten competing portfolios. A clean comparison might use a broad stock portfolio, a balanced stock and bond portfolio, and a conservative allocation. If the beginner cannot explain each portfolio in one sentence, the comparison is probably too complex.

Finally, compare the story, not only the score. Look at when each portfolio struggled. Did Portfolio A fall more in a crash but recover faster? Did Portfolio B lag in strong markets but create a smoother experience? Did Portfolio C protect capital but fail to grow enough? The answer should help you choose a behavior you can actually repeat.

Reading drawdown like a real investor

Drawdown is the decline from a previous portfolio high to a later low. If a portfolio grows to $100,000 and then falls to $75,000, the drawdown is 25%. This number matters because it describes the emotional test the investor had to survive. A portfolio that looks attractive at the end of a chart may have required unusual patience in the middle.

Beginners often underestimate drawdown because they see it as a statistic instead of a lived experience. A 30% decline does not feel like an abstract number when it happens during a recession, job uncertainty or negative market headlines. If the backtest shows a large drawdown, ask whether you would have kept contributing, stopped investing, sold part of the portfolio or changed the plan.

Recovery time matters alongside drawdown. A portfolio that falls 25% and recovers in six months feels different from a portfolio that stays below its old high for five years. Long recovery periods can be emotionally harder than the initial decline. This is especially important for investors who may need the money before the portfolio has time to recover.

For a beginner, drawdown should not automatically eliminate a portfolio. Growth assets often require tolerating declines. The point is to know the size of the historical pain before committing. If a backtest shows a drawdown you could not realistically tolerate, the portfolio may be too aggressive even if the ending return is impressive.

What beginners should leave out of the first backtest

A beginner portfolio backtest should be simple enough to understand. That means some advanced details can wait. You do not need Monte Carlo simulations, tax-lot accounting, factor models, tactical signals or complex withdrawal rules in the first session. Those can become useful later, but they can distract from the main allocation decision.

Do not start with too many assets. A portfolio with twelve holdings may look professional, but it can make the result harder to interpret. If the portfolio wins, you may not know why. If it loses, you may not know what to change. A beginner can learn more from three clear assets than from a complicated portfolio that hides the cause of the outcome.

Do not start with unrealistic return assumptions. Historical backtesting uses actual market data, but some tools also allow expected return projections. If you move from historical testing into future projection, keep the assumptions modest. A plan that only works under optimistic returns is fragile.

Do not start by optimizing for the best past result. It is tempting to adjust weights until the historical chart looks perfect. That usually creates a portfolio designed for yesterday. A more durable approach is to choose sensible weights first, test them, and then adjust only if the result reveals a real problem.

When a beginner backtest becomes a portfolio planning system

The first backtest is usually a learning exercise. You want to see how an allocation behaved and whether the risk feels acceptable. Over time, the workflow can become more serious. You may want to test multiple contribution levels, compare several portfolio mixes, account for fees, model rebalancing and save scenarios for later review.

This is the moment when portfolio backtesting starts to become portfolio planning. The question changes from "what happened in the past?" to "which plan should I follow now, and how should I review it later?" That shift matters because the tool must support repeatable decisions. A one-time chart is helpful, but a saved, organized comparison is more useful when real money is involved.

For example, a beginner might first test a 70/30 allocation in the free simulator. Later, the same user may want to compare 70/30, 80/20 and 60/40 across different contribution levels. They may want to export a report, review the assumptions, or compare the result with a DCA plan. At that stage, Premium is not just an upgrade button. It becomes a workflow for keeping scenario analysis organized.

This is also why WhatIfInvested connects tools instead of treating each calculator as isolated. The Investment Simulator helps with historical portfolio behavior. The DCA Calculator helps with recurring investment strategy. The Premium workflow supports more advanced comparison when the decision needs depth.

Frequently asked questions

What is portfolio backtesting for beginners?

Portfolio backtesting for beginners means testing a simple asset allocation against historical market data. The goal is to understand growth, drawdown, recovery and behavior before relying on a portfolio plan.

How do I backtest a portfolio?

Choose assets, assign target weights, select a time period, decide whether to use lump sum or recurring contributions, and compare final value with drawdown and recovery. Start simple before adding advanced assumptions.

Is portfolio backtesting accurate?

Portfolio backtesting can be useful, but it is not a prediction. It depends on data quality, assumptions, fees, rebalancing rules and the historical period chosen. Use it to understand trade-offs, not to guarantee future returns.

What metrics should beginners look at first?

Beginners should start with final value, total return, maximum drawdown, recovery time and contribution impact. These metrics explain both the outcome and the difficulty of staying invested.

Should I include rebalancing in a beginner backtest?

Yes, but test it simply. Compare no rebalancing with annual rebalancing first. This shows whether keeping target weights changed the risk and return enough to matter.

Can I backtest a portfolio with monthly contributions?

Yes. Monthly contributions are useful because many investors build portfolios gradually. A contribution-based test can show how savings behavior interacts with historical returns.

When should I use Premium instead of the free simulator?

Use Premium when you need multiple scenarios, custom portfolio assumptions, saved comparisons, exports or a more organized research workflow. Use the free simulator first when the question is simple.

Does a strong backtest mean the portfolio will work in the future?

No. A strong backtest only shows how the portfolio behaved in the selected historical period. Future markets can be different, so results should be treated as context rather than certainty.

Final takeaway

Portfolio backtesting for beginners should make investing decisions clearer, not more complicated. Start with a simple allocation, compare it against one or two alternatives, review risk as carefully as return and use the result to understand whether the portfolio fits your behavior.

When you are ready, open the Investment Simulator and test your first portfolio. If your planning grows into multiple scenarios, deeper comparisons or export-ready analysis, move the workflow into Premium.