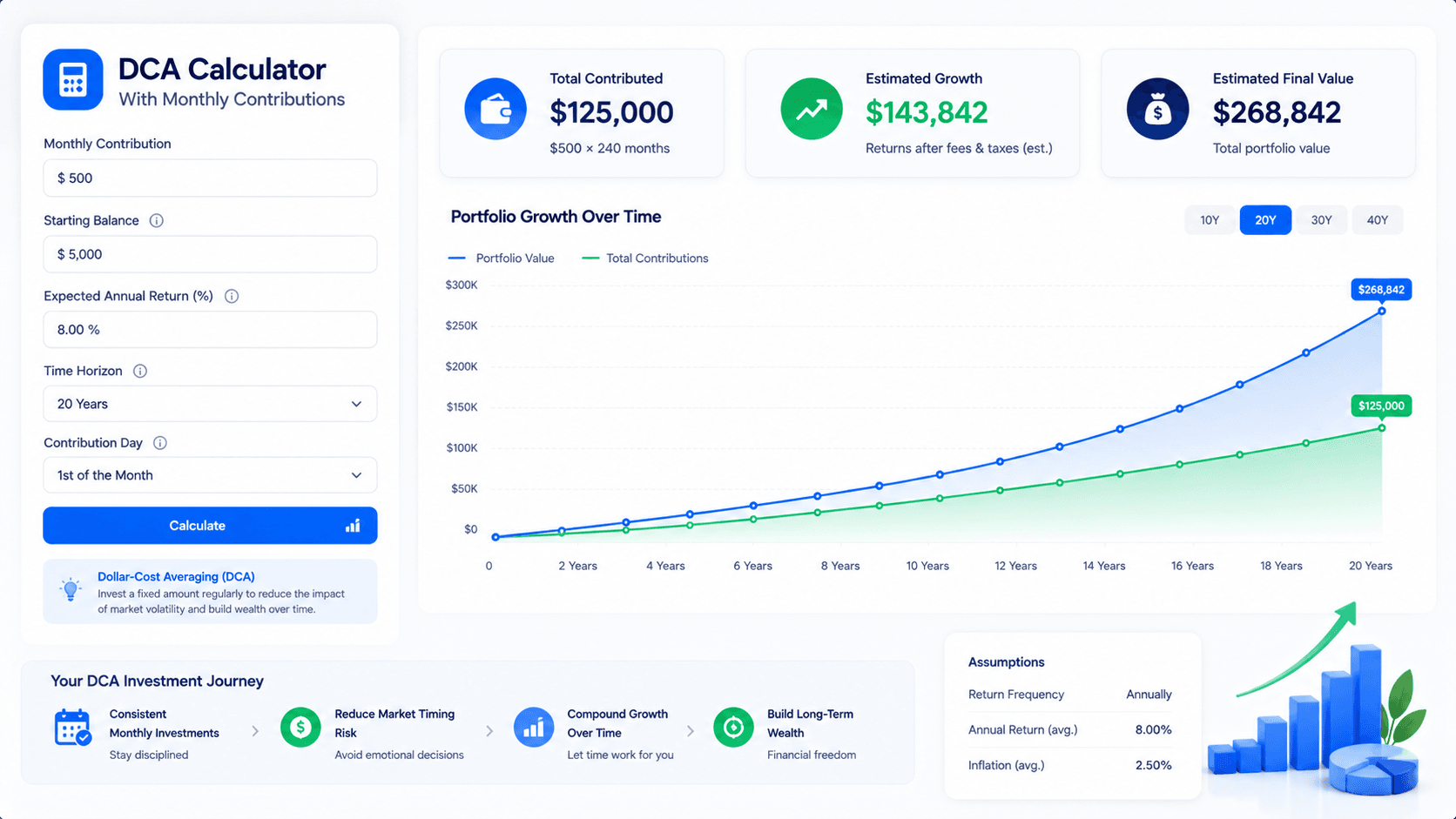

DCA Calculator With Monthly Contributions

A DCA calculator with monthly contributions helps you estimate how a recurring investment habit could grow over time. Instead of guessing whether $100, $250 or $500 per month is enough, you can model the starting balance, monthly deposit, expected return, timeline and final value before committing to a plan.

DCA calculator with monthly contributions: what it shows

The calculator turns a simple monthly deposit into a year-by-year investment path. The output is useful because it separates money you contributed from growth created by returns. That makes the result easier to understand than a single final number.

Quick answer: how to use a DCA calculator with monthly contributions

To use a DCA calculator with monthly contributions, enter your starting balance, the amount you can invest every month, the expected annual return, the number of years you plan to invest, and any relevant fees. The calculator then estimates your ending value, total contributions, estimated growth and the yearly path of your investment plan.

The most important input is not the expected return. It is the monthly contribution you can actually sustain. A realistic $250 monthly contribution that runs for ten years is more useful than an aggressive $700 monthly contribution that stops after three months. The calculator is a planning tool, not a promise. It helps you compare scenarios before the market, your budget or your emotions make the decision for you.

On this page

The five inputs every monthly DCA calculation needs

A monthly DCA calculation looks simple, but the result depends heavily on the assumptions. The first input is your starting balance. This is the amount already invested before the monthly plan begins. A person starting from zero and a person starting with $20,000 can use the same monthly contribution, but their ending values will not look the same because the starting balance has more time to compound.

The second input is the recurring contribution. This is the amount added every month. It should come from real cash flow, not from a number that only looks good in a spreadsheet. If the contribution is too high, the plan may force you to pause, withdraw money early or use debt to cover normal expenses. A DCA calculator is most useful when the contribution is boring enough to repeat.

The third input is time horizon. Time changes everything. A $200 monthly contribution over three years is mostly a savings habit. The same $200 monthly contribution over twenty-five years becomes a compounding engine. Longer horizons make the expected return more important because returns have more time to earn returns of their own.

The fourth input is expected annual return. This is where many people become too optimistic. A calculator can show any result if the return assumption is high enough. That does not make the result realistic. A better workflow is to test a conservative return, a base case and an optimistic case. The spread between those outcomes is often more useful than the headline number.

The fifth input is friction: fees, taxes, expense ratios, spreads and inflation. These do not always appear in simple calculators, but they matter in real life. Even a small annual fee can reduce a long-term result. Inflation can make a future dollar worth less than it looks today. This is why the calculator should support decision-making, not replace judgment.

How to choose a monthly contribution amount

The best monthly contribution is the amount that fits your budget after essential expenses, minimum debt payments, emergency savings and normal life costs. It should stretch you slightly, but it should not make the plan fragile. If the number creates stress every month, it is probably too high. A smaller contribution that survives volatility is often better than a larger contribution that depends on perfect conditions.

Start by looking at monthly surplus. If you do not know your surplus, use WhatIfBudget first. A budget tool shows income, expenses, savings and investable cash flow. Once you know the amount available for investing, the DCA calculator can show how that surplus could grow if invested consistently.

A useful method is to test three contribution levels. The first is your minimum contribution: the amount you can invest even during a normal expensive month. The second is your target contribution: the amount you hope to invest most months. The third is your stretch contribution: the amount you invest only when cash flow is unusually strong. This prevents the calculator from turning a best-case month into a permanent assumption.

If you are unsure where to start, compare this guide with how much to save monthly. The calculator can show the future value, but the budget decides whether the monthly number is realistic.

Monthly contribution examples

Examples help because monthly investing is easier to understand when the numbers feel concrete. The table below is not a return promise. It is a planning frame. It shows how contribution size and time horizon can change the relationship between money invested and potential future value.

| Monthly contribution | Best for | What to watch | Useful next step |

|---|---|---|---|

| $50 to $100 | Beginners building the habit | Fees and minimum trade sizes can matter | Focus on automation and consistency |

| $150 to $300 | Early investors with stable cash flow | Small return differences matter less than staying consistent | Run a 10-year and 20-year projection |

| $400 to $800 | Serious monthly investing plans | Asset allocation and volatility become more important | Compare DCA with lump sum and portfolio scenarios |

| $1,000+ | High-savings households or advanced investors | Tax location, fees and rebalancing rules matter more | Use Premium workflow for scenario comparison |

A beginner investing $75 per month should not feel discouraged by a small starting amount. Monthly DCA is partly about building a behavior system. The habit becomes easier to increase later when income rises or expenses fall. A consistent small contribution also teaches the investor how volatility feels before the account becomes large.

An investor contributing $500 per month has a different problem. The habit is already meaningful, so the question becomes whether the asset mix, time horizon and assumptions are strong enough. This investor should compare different returns, contribution increases and possible downturns. If the monthly plan is tied to retirement or a major goal, the investor should also think about inflation and whether future contributions will rise over time.

How to read the calculator results

The first result most people notice is the estimated ending value. That number is useful, but it should not be the only number you read. A better interpretation starts by separating total contributions from estimated investment growth. Total contributions show how much money came directly from your monthly deposits. Estimated growth shows how much the portfolio may have added through returns. This distinction matters because it helps you understand whether the plan is being driven mostly by savings behavior, market growth, or both.

In the early years, monthly contributions often do most of the work. That can feel disappointing if you expected compounding to look dramatic right away. But this is normal. Compounding becomes more visible after the account has a larger base. A plan that looks slow in year three can look much more powerful in year fifteen because returns are being earned on a larger balance.

The yearly breakdown is often more useful than the final value. It shows the path, not just the destination. If the year-by-year result feels too slow, you can test a higher contribution, a longer timeline or a different return assumption. If the result depends on an unrealistic contribution or aggressive return, the calculator is warning you that the plan may need adjustment.

Also pay attention to the gap between scenarios. If a conservative return and an optimistic return lead to very different outcomes, that means uncertainty is high. That does not mean the plan is bad. It means you should avoid building your entire financial expectation around one number. Use the calculator to create a range of outcomes, then decide whether the plan still works if the future is less generous than expected.

Choosing realistic expected return assumptions

Expected return is the input that can make a calculator feel magical or misleading. If you enter a very high annual return, the ending value can look exciting. But a high expected return often means higher risk, higher volatility or an assumption that may not survive a full market cycle. A DCA calculator with monthly contributions should be used to compare possible paths, not to manufacture certainty.

For broad stock market investing, many investors test long-term assumptions around conservative, base and optimistic cases. For example, a conservative case might use a lower return to reflect weak markets or higher fees. A base case might reflect a moderate long-term assumption. An optimistic case might show what happens if markets perform well. The value is in comparing the range.

It is also important to separate nominal and real returns. A nominal return does not adjust for inflation. A real return does. If inflation averages 2% to 3%, a future account value may have less purchasing power than the same number suggests today. For long-term planning, it can help to run one scenario using a lower return that roughly accounts for inflation.

External investor education resources such as Investor.gov’s material on dollar-cost averaging frame DCA as a disciplined investing method, not a guarantee of profit. That is the right mindset. The calculator helps you understand scenarios. The market still decides actual returns.

Fees, inflation and taxes can change the result

Monthly investing can be powerful, but small frictions compound too. A fund expense ratio, trading commission, currency conversion spread, platform fee or advisory fee may look tiny in one month. Over many years, those costs reduce the amount that remains invested. This is especially important for smaller monthly contributions because fixed transaction costs can be large relative to the deposit amount.

If you invest $50 per month and pay a $2 trading fee, the fee is 4% of the contribution before the investment even begins. If you invest $500 per month and pay the same $2 fee, the drag is much smaller. This is why commission-free fractional investing can make monthly DCA more practical for small investors. It is also why daily investing can become inefficient when costs are not close to zero.

Taxes also matter. Contributions in taxable accounts, retirement accounts and tax-advantaged accounts may produce different after-tax results. A simple calculator may not know your exact tax situation. If taxes are central to the decision, treat the DCA result as a pre-tax planning estimate and adjust your expectations. For serious planning, compare scenarios in a more advanced workflow.

Inflation is the silent adjustment. A $500,000 future balance may sound large, but its purchasing power depends on how far in the future it arrives. When modeling long horizons, you can either use a lower real return or mentally discount the final value. Either approach is better than assuming future dollars and today’s dollars are identical.

When monthly contributions are not enough

A monthly contribution plan can be disciplined and still fall short of the goal. This usually happens for one of four reasons: the contribution is too small, the timeline is too short, the expected return is too low for the goal, or the goal itself is larger than the current savings rate can support. The calculator helps reveal that gap early, which is better than discovering it years later.

If the monthly amount is too small, there are only a few honest options. You can increase income, reduce expenses, extend the timeline, lower the target or accept more investment risk. The last option should be handled carefully. Taking more risk may increase potential return, but it can also increase volatility and the chance that you abandon the plan during a downturn.

If the timeline is too short, increasing the monthly contribution may matter more than chasing return. For example, someone investing for a goal three years away should usually care more about safety and contribution amount than aggressive market growth. Someone investing for twenty-five years may have more room to let compounding work, but still needs a contribution that is large enough to matter.

If the calculator shows a gap, treat it as useful information rather than failure. A gap means the plan needs a better design. You might use WhatIfBudget to identify extra monthly surplus, use the DCA Calculator to test a higher contribution, then use Premium later if the decision involves multiple portfolios, fees or saved scenarios. The goal is not to force the first scenario to work. The goal is to find a plan that can survive real life.

Monthly DCA vs compound interest calculator

A DCA calculator and a compound interest calculator can look similar because both handle recurring contributions. The difference is the decision context. A DCA Calculator is best when your question is about recurring investing behavior, contribution schedules and gradual entry. A Compound Interest Calculator is best when your question is about general future value, savings growth or long-term compounding.

If you are investing into markets monthly, start with the DCA Calculator. It matches the mental model of dollar-cost averaging: steady contributions through changing markets. If you are projecting a savings account, a fixed return assumption or a long-term growth target, the compound interest calculator may be cleaner. The tools overlap, but they serve different moments in the planning process.

| Question | Better tool | Reason |

|---|---|---|

| How much could monthly investing grow? | DCA Calculator | Built around recurring investment behavior. |

| How much will a fixed-return savings plan become? | Compound Interest Calculator | Cleaner for future value and compounding assumptions. |

| What if my monthly amount changes? | Premium workflow | Advanced scenarios can compare more moving parts. |

| How much can I afford to invest? | WhatIfBudget | Budgeting comes before investing assumptions. |

Common mistakes when using a DCA calculator with monthly contributions

The first mistake is entering a monthly contribution that does not match real cash flow. A calculator can make any plan look organized, but the budget decides whether the plan survives. If the contribution competes with rent, debt payments or emergency savings, it may create more stress than progress.

The second mistake is using one expected return as if it were guaranteed. Markets do not move in straight lines. A calculator that assumes a smooth 8% annual return may hide the discomfort of bad years. Run lower-return scenarios. Test shorter horizons. Ask whether you would keep contributing during a weak period.

The third mistake is ignoring fees. This matters most when contributions are small or when the platform charges transaction costs. Fees can also appear through fund expenses, spreads, currency conversion and taxes. The monthly contribution is only one part of the outcome. The cost of investing that contribution matters too.

The fourth mistake is confusing a final value estimate with a plan. A final number is not a strategy. A real plan includes where the money comes from, which assets receive the contribution, how often assumptions are reviewed and what happens when income changes. The calculator gives the math. You still need the process.

The fifth mistake is comparing yourself to unrealistic examples. Someone investing $2,000 per month with a high income is not the benchmark for a beginner investing $100 per month. The right question is not “is my number impressive?” It is “is my number sustainable and moving me closer to the goal?”

A simple monthly DCA planning workflow

Use this workflow if you want a practical path from idea to action. First, confirm your monthly investable surplus with a budget. Second, choose a baseline contribution that you can repeat. Third, open the DCA Calculator and enter your starting balance, monthly contribution, time horizon and expected return. Fourth, run at least three scenarios: conservative, base and optimistic.

After that, compare the difference between scenarios. If the optimistic scenario is exciting but the conservative scenario is unacceptable, you may need a higher contribution, longer timeline or different goal. If the conservative scenario still moves you forward, the plan is more resilient. Finally, decide how often you will review the plan. Monthly review may be too frequent for long-term investing. Quarterly or semiannual review is often calmer.

- Find your investable monthly surplus.

- Choose a minimum, target and stretch contribution.

- Run the DCA Calculator with conservative assumptions.

- Compare the base and optimistic cases.

- Automate the contribution if the plan is realistic.

- Review the plan on a scheduled cadence instead of reacting to market noise.

This workflow connects directly with the broader dollar-cost averaging strategy. Monthly contributions are not just numbers. They are a system for turning income into long-term exposure without requiring perfect timing.

Related guides and tools

Frequently asked questions

What is a DCA calculator with monthly contributions?

A DCA calculator with monthly contributions estimates how recurring monthly investments could grow over time. It usually uses a starting balance, monthly deposit, expected return and time horizon to project total contributions, growth and ending value.

How much should I invest monthly with DCA?

The best monthly amount is the amount you can repeat after covering essential expenses, debt payments, emergency savings and normal cash flow needs. Start with a sustainable baseline, then increase it later if your budget allows.

Is monthly DCA better than weekly DCA?

Monthly DCA is usually simpler and works well for long-term investors. Weekly DCA can make sense if it matches your paycheck or if you want smoother entries. The best schedule is the one you can automate consistently with low fees.

Can I use a DCA calculator for ETFs?

Yes. A DCA calculator is useful for ETF investing because many ETF plans use recurring monthly contributions. Use realistic return assumptions and remember that actual market returns will vary.

Does a DCA calculator include fees and inflation?

Some calculators include fees and inflation, while simpler calculators may not. Even when fees are not built in, you should consider fund expenses, trading costs, taxes and inflation before relying on the final result.

What is the difference between DCA and compound interest calculators?

A DCA calculator is focused on recurring investing behavior and gradual market entry. A compound interest calculator is focused on future value and growth from compounding. They overlap, but the decision context is different.

Should I use Premium for monthly contribution planning?

Use the free calculator for a quick monthly contribution estimate. Use Premium when you need multiple scenarios, portfolio weights, fees, saved assumptions, withdrawals or exportable reports.

Can I change my monthly contribution later?

Yes. Most investors should revisit their monthly contribution as income, expenses and goals change. The key is to update the plan intentionally rather than changing it every time the market moves.