RESP Explained: How to Maximize CESG Grants and Invest Smart

A practical Canadian guide to RESP rules, CESG grant strategy, contribution planning, investment choices, withdrawals, and common mistakes families should avoid.

The basic CESG can add 20% on eligible RESP contributions, subject to annual and lifetime limits.

The earlier grants and contributions are invested, the longer they can compound before post-secondary education.

An RESP is not just a savings bucket. Asset allocation should evolve as the student approaches school.

Quick Verdict: Why an RESP Matters

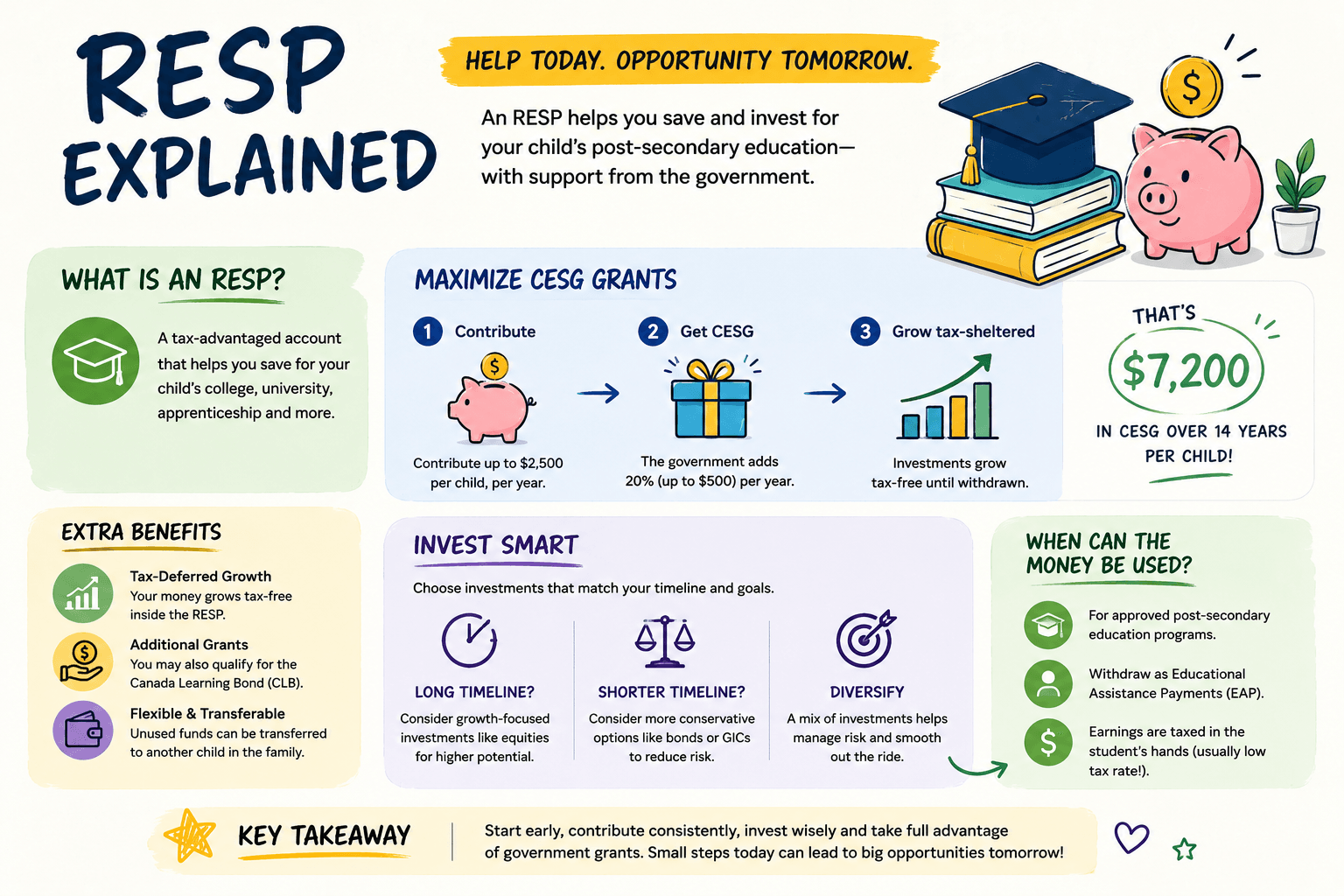

A Registered Education Savings Plan is one of the most valuable education savings accounts for Canadian families because it combines government grants, tax-deferred growth, and a long investment horizon. The main opportunity is not only saving money for school. It is capturing grants early and letting those grants compound.

The basic Canada Education Savings Grant generally matches 20% of eligible RESP contributions, up to the government’s annual and lifetime limits. Canada.ca notes that unused CESG room can be carried forward, which means families who started late may still recover some missed grant room if they contribute strategically.

What Is an RESP?

An RESP is a registered account designed to help save for a child’s post-secondary education. Contributions are made with after-tax money, but investment growth inside the account is tax-deferred. When funds are withdrawn for eligible education, grants and investment earnings are generally paid to the student as education assistance payments, which are taxable to the student.

This structure can be powerful because students often have low income while studying. Contributions themselves can usually be withdrawn tax-free by the subscriber because they were made with after-tax dollars. The planning challenge is making sure the account is funded, invested, and withdrawn correctly.

| RESP feature | Why it matters |

|---|---|

| Government grants | CESG can boost eligible contributions before market returns are even considered. |

| Tax-deferred growth | Investment income can compound inside the plan until withdrawn. |

| Education assistance payments | Grants and growth are generally taxable to the student when used for school. |

| Family planning | Contribution timing, beneficiary rules, and withdrawal strategy should be planned in advance. |

For official rules, use the Government of Canada’s RESP and education savings pages as the source of truth.

How CESG Works

The Canada Education Savings Grant is the main reason many families prioritize RESP contributions. Canada.ca explains that eligible beneficiaries can receive a basic CESG amount based on contributions, with a lifetime maximum per beneficiary. Additional CESG may also be available for eligible families based on income, but the thresholds can change, so they should be verified directly with the government.

The basic idea is simple: contribute to the RESP, receive grant room if eligible, then invest both the contribution and the grant. The grant itself is valuable, but the compounding on the grant can be even more valuable over a long period.

| CESG rule | Planning implication |

|---|---|

| Basic CESG matching | Families often aim to contribute enough each year to capture the available grant. |

| Lifetime CESG maximum | There is a ceiling, so the goal is to capture grants efficiently over time. |

| Carry-forward room | Late starters may recover some missed grant room with larger future contributions. |

| Additional CESG | Eligible lower and middle income families may receive extra grant on the first part of contributions. |

RESP Contribution Strategy

The cleanest RESP strategy is usually to start early, contribute consistently, and aim to capture available grants. Early contributions matter because they give both your money and the government grant more time to compound. Waiting can still work, but late catch-up contributions have less time to grow before school begins.

The best contribution strategy depends on cash flow. Some families can contribute annually. Others may prefer monthly contributions. Monthly deposits can make the plan easier to sustain and reduce the risk of forgetting. The important part is building a repeatable system.

Early starter strategy

- Open the RESP as soon as practical.

- Automate monthly or annual contributions.

- Invest according to a long time horizon.

- Track grant room and beneficiary limits.

Late starter strategy

- Check unused CESG room.

- Prioritize catch-up contributions if cash flow allows.

- Avoid taking excessive investment risk just to catch up.

- Plan withdrawals before the student starts school.

Use a budget tool like WhatIfBudget to identify a sustainable monthly amount, then use the Compound Interest Calculator to model how contributions and growth can add up.

A Simple RESP Contribution Scenario

Imagine a family that wants to contribute monthly instead of waiting for one large annual deposit. The first advantage is behavior: a smaller automatic contribution is easier to keep than a large year-end decision. The second advantage is planning: monthly deposits make it easier to see whether the RESP fits the household budget without sacrificing rent, food, emergency savings, or debt repayment.

The family should not only ask how much it wants the RESP to reach. It should ask which contribution rhythm is sustainable through normal life. A plan that captures a grant for one year and then stops may be less useful than a smaller contribution that continues for many years. RESP planning works best when it is treated as a long-term family cash-flow decision, not a one-time tax-season task.

| Family situation | Better RESP move | Reason |

|---|---|---|

| Stable monthly surplus | Automate monthly RESP deposits. | Consistency reduces missed contributions. |

| Irregular income | Use small monthly deposits plus occasional top-ups. | The plan survives weak cash-flow months. |

| Late starter | Verify unused grant room before increasing deposits. | Catch-up only helps if it fits the broader budget. |

| Child close to school | Reduce portfolio risk before withdrawals. | Protects education money from a poorly timed drawdown. |

Canada Learning Bond and Additional Support

The Canada Learning Bond is another government education savings incentive for eligible children from lower-income families. It does not require personal contributions to receive the bond, but an RESP must be opened for the child. This makes it especially important for eligible families to open an RESP even if they cannot contribute much immediately.

Canada.ca explains that the Canada Learning Bond can be deposited directly into the child’s RESP. Because eligibility rules and application details can change, families should verify directly on the official Canada Learning Bond page or with an RESP promoter.

How to Invest Inside an RESP

An RESP should not sit in cash for the entire childhood unless the education date is very close or the family has a specific low-risk reason. Over many years, inflation can reduce the value of cash. Investing the contributions and grants can help the account grow, but the asset allocation should match the child’s timeline.

For a young child, a growth-oriented allocation may make sense because the money has more time to recover from market declines. As the child approaches post-secondary school, the risk should usually come down. A severe market drop right before withdrawals can be damaging if the account is still too aggressive.

| Timeline | Possible allocation mindset | Main risk |

|---|---|---|

| Long horizon | More growth-oriented, diversified ETFs may fit. | Short-term volatility. |

| Middle years | Begin balancing growth with stability. | Ignoring risk until too late. |

| Near school | More conservative mix or cash-like holdings may fit. | Market drop before withdrawal. |

| During school | Match investments to planned withdrawal schedule. | Liquidity and timing risk. |

For ETF ideas, connect this with Top ETFs for Long-Term Investing and Top ETFs for Monthly DCA.

RESP Withdrawals: Plan Before School Starts

RESP withdrawal planning matters because contributions, grants, and investment earnings are treated differently. Contributions can generally be withdrawn by the subscriber without being taxed again. Grants and investment growth are paid as education assistance payments and are taxable to the student when used for eligible education.

Families should avoid waiting until the last minute to understand withdrawals. Before school begins, review the student’s expected program, expenses, timing, and income. Then coordinate withdrawals so the money supports tuition, housing, books, transportation, and other eligible education needs without creating unnecessary confusion.

Before withdrawals

- Confirm eligible post-secondary enrollment.

- Understand contribution vs EAP withdrawals.

- Check grant and growth balances.

- Coordinate with the RESP provider.

During withdrawals

- Keep proof of enrollment.

- Plan timing around school expenses.

- Consider student tax situation.

- Avoid leaving the strategy to the last month.

Family RESP vs Individual RESP

One of the first decisions is whether to use an individual RESP or a family RESP. An individual plan has one beneficiary, while a family plan can include more than one eligible beneficiary who is related to the subscriber by blood or adoption. The right choice depends on how many children you are planning for, how much flexibility you want, and how comfortable you are tracking grant room for more than one child.

A family RESP can be convenient when parents expect to fund education for multiple children. It can make account management simpler and may allow some flexibility if one child uses less money than expected. However, it also requires careful tracking because CESG limits apply per beneficiary. A family account should not become a vague pool of money where nobody knows which child has received which grants.

| Plan type | Best fit | Planning note |

|---|---|---|

| Individual RESP | One child, simple tracking, or a child who may not have siblings in the plan. | Cleaner record keeping because all activity belongs to one beneficiary. |

| Family RESP | Multiple eligible children in the same family. | Useful, but track contributions and grants per beneficiary. |

| Group RESP | Families who understand the contract and fee structure very clearly. | Read terms carefully because flexibility and fees can differ from self-directed plans. |

RESP Catch-Up Strategy for Missed CESG Room

Families do not always start at birth. Sometimes cash flow is tight, parents discover RESP rules late, or the account was opened but contributions were inconsistent. That does not mean the opportunity is gone. Canada.ca explains that unused CESG room can be carried forward, subject to program rules and maximums. This makes catch-up planning one of the highest-impact RESP topics for late starters.

The catch-up approach is different from a normal contribution schedule. Instead of only asking, “How much can I contribute this month?” the better question is, “How much eligible grant room can I realistically capture without hurting my emergency fund, debt repayment, or rent and food budget?” RESP optimization should support the family plan, not create short-term stress.

Good catch-up behavior

- Verify unused CESG room with the provider.

- Contribute more only when cash flow allows.

- Keep an emergency fund outside the RESP.

- Use a monthly plan if lump sums are difficult.

Bad catch-up behavior

- Borrowing at high interest just to get a grant.

- Taking aggressive market risk near school age.

- Ignoring each beneficiary’s lifetime grant limit.

- Using RESP money as if it were a regular chequing account.

For families trying to find room in the budget, the best sequence is usually budget first, RESP second, investing third. Use How to Make a Monthly Budget or WhatIfBudget to identify a sustainable contribution amount before increasing deposits.

RESP Investment Timeline by Child Age

RESP investing is different from retirement investing because the withdrawal date is easier to estimate. A child may not attend school at the exact expected age, but the window is still much more defined than a retirement account. That means the investment strategy should become more conservative as the education date approaches.

When the child is young, the account can usually tolerate more volatility because there may be many years before withdrawals. In the middle years, a balanced approach can make sense. In the final years before school, protecting the money becomes more important than chasing the highest return. The closer the withdrawal date, the less time there is to recover from a major market decline.

| Stage | Goal | Common approach |

|---|---|---|

| Young child | Maximize long-term compounding. | Diversified growth-oriented ETFs may fit risk-tolerant families. |

| Middle school years | Balance growth and preservation. | Gradually add more fixed income or lower-volatility holdings. |

| Final years before school | Protect near-term withdrawals. | Shift planned withdrawals toward safer assets or cash-like instruments. |

| During school | Match money to expense timing. | Keep near-term tuition and living costs liquid. |

What If the Child Does Not Attend Post-Secondary School?

This is one of the reasons families hesitate to use an RESP, but it should not be ignored or exaggerated. If the beneficiary does not attend an eligible post-secondary program, the treatment of contributions, grants, and accumulated income depends on the plan rules and government rules. Contributions are generally treated differently from grants and investment earnings, so families should speak with their RESP provider before making assumptions.

In some cases, another eligible beneficiary may be available, especially with a family RESP. In other cases, grants may need to be returned and accumulated income may have specific withdrawal rules and tax consequences. The important planning point is that an RESP is designed for education, not as a general savings account. It is powerful when used for school, but less flexible than a regular taxable account.

Questions to ask your provider

- Can another beneficiary use the plan?

- Which grants would need to be returned?

- What happens to accumulated income?

- Are there deadlines or plan age limits?

How to reduce uncertainty

- Avoid overfunding beyond realistic education needs.

- Keep separate savings for non-education goals.

- Review plan rules before major contributions.

- Update the plan as the child’s path becomes clearer.

RESP Checklist for Parents

A strong RESP plan does not need to be complicated, but it should be organized. The families who benefit most usually have a repeatable process: open the account early, confirm eligibility, contribute consistently, invest with the right time horizon, and review the plan as the child gets closer to school.

- Open the RESP: choose the plan type and provider carefully.

- Confirm documents: make sure the child has the required identification and beneficiary information.

- Check grant eligibility: verify CESG and Canada Learning Bond possibilities.

- Set a contribution rhythm: monthly automation is often easier than relying on memory.

- Invest the money: avoid leaving long-term education savings idle if the time horizon is long.

- Review annually: compare contributions, grants received, investment mix, and school timeline.

- Plan withdrawals early: contact the provider before school starts so the process is clear.

This checklist also improves family decision-making. Instead of reacting every few years, you create a simple annual routine. That routine is what turns a useful account into a real education funding strategy.

Common RESP Mistakes

- Starting too late: late contributions may still help, but early grants have more time to compound.

- Leaving everything in cash: cash can be too conservative for a long horizon.

- Taking too much risk near school: equity volatility can hurt when withdrawals are close.

- Missing CESG room: not tracking grants can leave government money unclaimed.

- Ignoring Canada Learning Bond eligibility: eligible families may miss support that does not require contributions.

- Not planning withdrawals: understanding EAPs before school begins can prevent stress.

Bottom Line

An RESP is powerful because it combines government support with long-term investing. The family’s job is to capture available grants, invest the money according to the student’s timeline, and avoid taking either too little risk early or too much risk late.

The best RESP strategy is not complicated, but it does require consistency. Open the account, check grant eligibility, contribute what your budget allows, invest appropriately, and revisit the plan as school gets closer.

Frequently Asked Questions

What is an RESP?

An RESP is a registered education savings account in Canada designed to help save and invest for post-secondary education.

What is CESG?

The Canada Education Savings Grant is government money added to eligible RESP contributions, subject to annual and lifetime limits.

Can unused CESG room be carried forward?

Yes, Canada.ca explains that unused CESG room can be carried forward, subject to the program’s rules and maximums.

Should an RESP be invested?

Often yes, especially when the child is young. The investment mix should become more conservative as withdrawals approach.

What happens if the child does not attend school?

There are specific rules for contributions, grants, and accumulated income. Families should check official rules and speak with their RESP provider.

Where should I verify current RESP rules?

Use official Government of Canada pages and your RESP provider, because grant eligibility, limits, and program details can change.

Official RESP Resources

Verify current rules directly with Government of Canada resources. The main education savings hub is the best starting point because RESP, CESG, Canada Learning Bond, contribution, and withdrawal details can change over time: