What If You Had Invested in Gold Since 2000?

Gold has moved from an ignored asset near the start of the 2000s to a major store-of-value conversation. This guide breaks down what that journey actually teaches investors about returns, inflation, drawdowns, and portfolio diversification.

Gold rewarded patience, but not without long uncomfortable stretches.

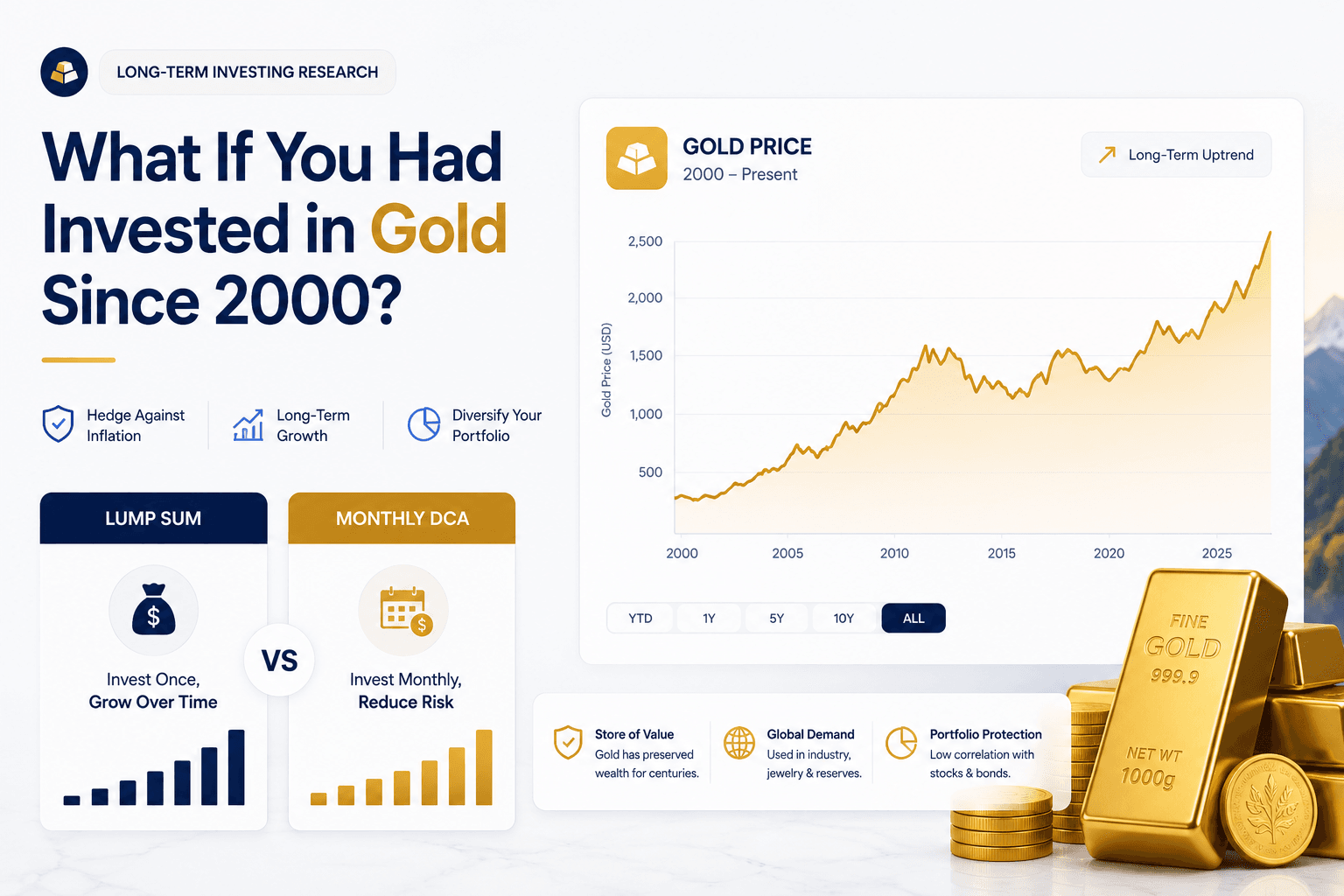

If you invested in gold around 2000 and stayed patient, the nominal result would have been strong. Gold moved from the high-$200s per ounce around 2000 to annual average prices above $2,400 in 2024, based on long-run historical price datasets.

The lesson is not that gold should replace stocks. The stronger lesson is that gold can behave very differently from stocks, bonds, cash, and crypto. That difference is exactly why some investors use it as a diversifier.

Gold's annual average price moved from roughly $279 per ounce in 2000 to above $2,400 in 2024.

- 2000Near multi-decade lows

- 2024Above $2,400 annual average

Why the year 2000 is such an interesting starting point

The year 2000 was a fascinating entry point for gold. Stocks had just finished a powerful technology-led bull market. Many investors were focused on internet companies, growth stocks, and equity optimism. Gold, by contrast, was deeply out of favor after a long bear market. Prices were near multi-decade lows, and the metal did not look exciting compared with the booming stock market narrative of the late 1990s.

That is exactly why the question matters: what if you had bought the asset that looked boring when the popular asset looked unstoppable? From that point forward, investors lived through the dot-com crash, the 2008 financial crisis, aggressive central bank policy, the European debt crisis, the pandemic, inflation pressure, rising-rate cycles, and renewed demand for safe-haven assets. Gold did not move in a straight line, but it had several periods where it behaved very differently from equities.

According to long-run historical price tables such as Macrotrends, gold's annual average price was roughly $279 per ounce in 2000 and above $2,400 in 2024. That is a major nominal move. But a smart investor should not stop at the headline return. The more useful question is how that return was earned, how volatile the journey was, and what role gold would have played inside a broader portfolio.

Gold was unloved

Gold entered the 2000s after a long period of weak sentiment. This made the setup very different from buying after a huge public mania.

Crises mattered

Financial stress, currency concerns, inflation expectations, and policy uncertainty all helped shape gold demand over the next two decades.

Popularity is not value

Assets that look boring at the wrong moment can later become useful when the market environment changes.

Gold performance since 2000: strong, but not simple

If you look only at the start and ending price, gold's performance since 2000 looks spectacular. A move from below $300 per ounce to multiple thousands per ounce is a powerful long-term return. However, gold's path was uneven. It had major bull markets, long sideways periods, and painful corrections.

The first major phase came during the early 2000s, when gold began recovering from its long bear market. The second phase accelerated around the financial crisis, when investors became more concerned about banking risk, monetary expansion, and systemic uncertainty. Gold then surged into the early 2010s, before entering a difficult period of consolidation and decline. Later, pandemic shock, inflation pressure, central bank activity, and geopolitical uncertainty supported renewed demand.

The World Gold Council's gold market data track gold spot prices, returns, volatility, ETF flows, and related market data. Their broader research also frames gold as a strategic asset because it can serve multiple roles: long-term store of value, crisis hedge, source of liquidity, and portfolio diversifier.

| Period | Gold backdrop | Investor experience |

|---|---|---|

| Early 2000s | Gold recovered from low sentiment and weak prices. | Patient buyers began seeing a trend reversal while equities struggled after the dot-com bubble. |

| Financial crisis era | Safe-haven demand rose as credit markets and banks came under stress. | Gold became more visible as a hedge against systemic uncertainty. |

| Post-2011 consolidation | Gold corrected after a major rally and spent years frustrating trend followers. | Investors learned that gold can have long periods of weak performance. |

| Pandemic and inflation era | Policy response, inflation concerns, and risk events supported renewed interest. | Gold again showed why some investors keep a strategic allocation. |

A useful gold article should not oversell the metal. Gold does not produce earnings, dividends, coupon income, or business growth. Its return comes from price appreciation, supply and demand, currency dynamics, inflation expectations, real interest rates, central bank activity, and investor behavior. That makes gold different from productive assets like stocks, but different does not mean useless.

Lump sum vs DCA into gold since 2000

There are two common ways to think about a gold investment since 2000. The first is a lump sum: you invest a single amount at the beginning and hold. The second is dollar-cost averaging: you invest a fixed amount every month, buying more ounces when the price is low and fewer ounces when the price is high.

A lump sum investment near the start of 2000 would have benefited enormously from buying gold when it was cheap relative to later decades. Because the starting price was so low, the early capital had the full benefit of the long bull market. In that specific historical setup, lump sum had a powerful advantage.

DCA would have looked different. It would not place all the capital at the low starting price, so it may not maximize return in a long upward trend. But it would reduce timing pressure and make the strategy easier to follow for investors who did not have a large lump sum or who were unsure about gold's future. DCA is especially useful when contributions come from monthly cash flow.

Best if you bought early and held

Because gold was low around 2000, a lump sum investor captured more of the long-term move. The tradeoff was accepting the risk of being fully exposed to gold's volatility immediately.

Best for habit and risk control

A monthly buyer did not need to pick a perfect entry. DCA reduced emotional pressure and created exposure gradually, though it may have bought at higher prices as gold rose.

What this teaches investors

The gold example is a clean reminder that DCA and lump sum are not moral categories. They are implementation methods. Lump sum often wins when the asset rises strongly after the start date. DCA helps when prices fall after the start date or when investor psychology is the main obstacle. This is the same logic explored in our full DCA vs lump sum guide.

If you are investing in gold today, the decision should not be based only on what worked from 2000. That period had a unique starting valuation, macro environment, and sequence of crises. The better process is to define your target gold allocation, choose the vehicle, understand the costs, and then decide whether lump sum, DCA, or a hybrid schedule fits your risk tolerance.

Gold drawdowns: why patience mattered

Gold's long-term chart can look smooth when compressed into a multi-decade graph. Up close, the ride was far more uncomfortable. Gold investors experienced periods where the metal fell significantly from prior highs and stayed below those highs for a long time. This matters because a return that looks obvious in hindsight can feel very uncertain while you are living through it.

After gold's early 2010s peak, for example, investors faced a painful decline and a long period where other assets appeared more attractive. Someone who bought near the high had a very different experience from someone who started in 2000. This is why any "what if you invested" article must be careful about start-date bias.

Why gold can be hard to hold

Gold can be emotionally difficult because it does not produce income. If a stock portfolio declines, investors can still point to earnings, dividends, innovation, or business growth. If a bond declines, investors can point to coupons and maturity value. Gold is different. Its value is based on market price, scarcity, demand, monetary confidence, and investor perception.

This makes gold useful but psychologically strange. It can shine when other assets struggle, then frustrate investors when stocks recover. It can hedge certain types of risk, but it does not hedge every risk. It can protect purchasing power over long horizons, but it does not perfectly track inflation year by year.

Inflation, real returns, and purchasing power

When people ask whether gold was a good investment since 2000, they are usually asking two questions at the same time. First, did gold go up in dollar terms? Second, did gold preserve or improve purchasing power after inflation? The first answer is easier: gold rose significantly in nominal terms. The second answer requires more nuance.

Gold is often called an inflation hedge, but that phrase can be misleading if it suggests a perfect year-by-year relationship. Gold does not move in lockstep with consumer prices. There are years when inflation is high and gold struggles. There are also years when inflation is moderate and gold performs strongly because investors are worried about currency stability, real interest rates, geopolitical risk, or central bank policy.

Over very long periods, gold has often been used as a store of value because it is scarce, globally recognized, and not issued by a government. But in a modern portfolio, its inflation role is more complex. Gold may respond not only to current inflation, but also to expected inflation, real yields, monetary credibility, and investor demand for alternatives to fiat currency.

Nominal return is not the whole story

A nominal return tells you how many more dollars you have. A real return tells you how much more purchasing power you have. If an asset rises 100% while prices for goods and services rise 60%, the investor is wealthier in real terms. If an asset rises 20% while inflation rises 40%, the investor has more dollars but less purchasing power.

Gold's rise since 2000 was large enough to matter even after inflation, but investors should still avoid treating gold as a guaranteed inflation solution. Treasury inflation-protected securities, real estate, equities, commodities, and cash management can all play different roles. Gold is one tool, not the entire toolbox.

Price in dollars

This is the chart most people see: gold price per ounce rising or falling in U.S. dollars.

Purchasing power

This adjusts for inflation and asks whether gold actually improved buying power.

Risk behavior

This asks whether gold helped the total portfolio during stress, not just whether gold rose alone.

Gold's real role: diversifier, not magic asset

The strongest case for gold is usually not "gold beats everything." The stronger case is that gold behaves differently. The World Gold Council's strategic asset research argues that gold can play a role in long-term portfolios because of its diversification, liquidity, and behavior during periods of stress.

That role is important. A portfolio made only of growth assets can perform very well in good times but suffer heavily when risk appetite collapses. A portfolio with some diversifying assets may give up some upside during strong bull markets, but it may be easier to hold through turbulence. Gold is often considered for that second job.

| Gold role | Potential benefit | Important limitation |

|---|---|---|

| Store of value | Gold has maintained monetary relevance across very long periods. | It can still underperform for years after bad entry points. |

| Inflation hedge | Gold can perform well during certain inflation or currency-stress regimes. | It does not track consumer inflation perfectly year by year. |

| Diversifier | Gold often behaves differently from stocks and bonds. | Diversification does not guarantee positive returns or prevent losses. |

| Crisis asset | Gold can attract demand during financial or geopolitical stress. | It can also fall during liquidity events when investors sell assets broadly. |

How much gold should be in a portfolio?

There is no universal answer. Some investors use no gold at all. Others use a small allocation such as 5% to 10%. More defensive investors may use more, but higher allocations increase the risk of lagging equity-heavy portfolios during long stock bull markets.

The right allocation depends on your objective. If gold is meant to reduce portfolio stress, a small allocation may be enough. If gold is meant to be a major store-of-value position, the allocation may be higher. If gold is a speculative trade, the sizing should reflect that risk. The key is to define the job before buying the asset.

Gold allocation examples for different investors

One of the most practical questions is not whether gold went up since 2000. It is how much gold would have made sense inside a real portfolio. An investor who put 100% of their net worth in gold had a very different risk profile from an investor who kept a 5% or 10% allocation and rebalanced annually.

Small allocations can have an outsized psychological benefit because they give the investor exposure to an asset that may perform differently during market stress. But large allocations can create opportunity cost if stocks and productive assets outperform. This is why gold is usually discussed as a diversifier rather than a replacement for an equity portfolio.

| Investor type | Possible gold allocation | Reason | Key risk |

|---|---|---|---|

| Growth-focused long-term investor | 0% to 5% | Focus remains on equities, with limited gold for diversification. | Too much gold may reduce long-term growth potential. |

| Balanced investor | 5% to 10% | Gold can provide a non-stock diversifier alongside bonds and cash. | Gold may lag during long equity bull markets. |

| Capital preservation investor | 10% to 15% | Higher allocation may help reduce dependence on stocks and bonds. | Higher opportunity cost if risk assets perform well. |

| Speculative gold believer | 15%+ | Investor is making a strong macro or currency view. | Concentration risk and long periods of underperformance. |

Rebalancing matters

A gold allocation is not only about the initial percentage. Rebalancing changes the experience. Suppose an investor targets 10% gold. If gold rises sharply and becomes 18% of the portfolio, rebalancing trims gold and buys other assets. If gold falls and becomes 6%, rebalancing buys more gold. This creates a disciplined process instead of emotional guessing.

Rebalancing is especially important because gold can have explosive moves followed by long pauses. Without a rebalancing rule, investors may chase after rallies or abandon gold after weak periods. A target allocation forces the investor to define the role of the asset before emotions take over.

Gold and withdrawal planning

For retirees or investors approaching withdrawals, gold's role can be different. It may act as part of a defensive reserve, though it should not be confused with cash. Gold can still fall when you need liquidity. However, because it can behave differently from equities, some investors use it alongside cash, short-term bonds, and diversified assets to reduce dependence on selling stocks during market stress.

Want to test gold against your own portfolio?

A historical article can show what happened, but your own decision depends on allocation size, contribution schedule, portfolio mix, rebalancing, fees, and time horizon. Use WhatIfInvested tools to compare gold with stocks, ETFs, Bitcoin, or a diversified allocation.

Free simulator

Use the Investment Simulator for quick historical comparisons.

DCA calculator

Use the DCA Calculator to model recurring contributions into an asset or portfolio.

Premium DCA

Use Premium DCA for weighted portfolios, fees, benchmarks, rebalancing, withdrawals, saved scenarios, and exports.

Ways to invest in gold

Investing in gold is not one single thing. The vehicle matters. Physical coins, bullion, gold ETFs, gold mining stocks, royalty companies, futures, and tokenized gold products can all produce different investor experiences. Costs, liquidity, counterparty risk, taxes, spreads, and storage all matter.

| Gold exposure type | What it gives you | Main tradeoff |

|---|---|---|

| Physical gold | Direct ownership of coins or bars. | Storage, insurance, bid-ask spreads, and liquidity friction. |

| Gold ETFs | Easy brokerage exposure to gold price movement. | Expense ratios, fund structure, tracking, and tax treatment. |

| Gold miners | Equity exposure to companies that mine gold. | Company risk, operating leverage, management risk, and stock-market behavior. |

| Gold royalty companies | Business exposure to gold production streams and royalties. | Still equity risk, valuation risk, and company-specific risk. |

| Futures or leveraged products | Tactical exposure for advanced traders. | Complexity, leverage risk, rollover, and potential losses beyond beginner expectations. |

Physical gold vs gold ETFs

Physical gold appeals to investors who want direct ownership outside the financial system. That can be valuable for certain risk concerns, but it comes with real-world friction. You need to think about storage, security, insurance, dealer spreads, authenticity, and how you would sell.

Gold ETFs are easier for many investors. They can be bought through a brokerage account, tracked in a portfolio, and rebalanced alongside stocks and bonds. But they introduce fund structure considerations and ongoing expense ratios. They may also have tax treatment that differs from ordinary stock ETFs depending on the jurisdiction.

Gold miners are not the same as gold

Gold mining stocks can rise more than gold when conditions are favorable, but they can also fall for reasons unrelated to the metal price. Mining companies deal with costs, labor, energy, political risk, geology, debt, management decisions, and operational execution. A gold miner is an equity investment, not pure gold exposure.

Gold vs stocks, bonds, cash, and Bitcoin

Gold should be compared by role, not only by return. Stocks are productive ownership claims on businesses. Bonds are contractual debt instruments. Cash is liquidity. Bitcoin is a scarce digital asset with very different volatility and adoption dynamics. Gold is a scarce physical monetary asset with deep history and global demand.

From 2000 onward, gold benefited from a very favorable starting point and several macro tailwinds. Stocks also performed well over long periods, especially when including dividends, but had major crashes early in the period. Bitcoin did not exist in 2000 and later produced extraordinary returns with extreme volatility. Bonds had their own cycles, including a difficult rising-rate period.

This is why a portfolio conversation is more useful than a single winner conversation. A person with 100% gold may miss growth from productive assets. A person with no diversifiers may struggle during deep equity stress. A person with too much cash may lose purchasing power. The best allocation depends on time horizon, risk tolerance, and purpose.

Gold vs Bitcoin

Gold has centuries of monetary history and lower volatility than Bitcoin. Bitcoin has a fixed supply schedule and digital portability, but it is far more volatile. Read our Bitcoin vs Gold comparison for a deeper look.

Gold vs ETFs

Broad equity ETFs are designed for productive long-term growth. Gold is usually used for diversification, crisis behavior, and monetary protection. Read our ETF vs Crypto guide if you want a broader risk comparison across asset classes.

What should investors do with gold today?

The fact that gold performed well from 2000 does not automatically mean a new investor should buy aggressively today. Historical case studies are useful because they teach behavior, risk, and market structure. They are not direct instructions. A better approach is to translate the lesson into a decision framework.

Start by asking what job gold would do in your portfolio. If the job is diversification, the allocation can be modest and rules-based. If the job is speculation on monetary stress, then you are making a macro bet and should size it accordingly. If the job is emergency liquidity, gold may not be the right tool because its price can fluctuate and physical sales can involve friction.

How to read a gold backtest correctly

A gold backtest is most useful when it is treated as a behavior study, not a prediction machine. The point is to see how an asset behaved through different environments: equity drawdowns, inflation fears, currency stress, rising rates, falling rates, and long periods of investor boredom. Gold can look brilliant if the chart starts near a low and ends near a high. It can also look frustrating if the chart starts near a peak and measures a long consolidation period.

That is why the start date matters so much. An investor beginning in 2000 saw a very different outcome from an investor who bought after a major gold rally. The same is true for stocks, Bitcoin, Tesla, bonds, and almost every volatile asset. Backtesting should help you understand range of outcomes, sequence risk, and emotional pressure. It should not be used to cherry-pick the most flattering window.

The cleaner process is to compare several scenarios: lump sum at the beginning, monthly DCA, a small strategic allocation inside a stock portfolio, and a rebalanced portfolio. That reveals whether gold improved the full portfolio, not only whether gold itself rose. For many investors, the better question is not “Did gold win?” but “Did gold make the portfolio easier to hold through bad markets?”

A simple gold decision checklist

- Do you already have an emergency fund separate from investments?

- Are you buying gold as a diversifier, inflation hedge, crisis hedge, or speculation?

- Will you use physical gold, ETF exposure, miners, or another vehicle?

- Do you understand costs, spreads, storage, expense ratios, and taxes?

- What target allocation will you use?

- How often will you rebalance?

- What would make you sell?

If you cannot answer those questions, it may be too early to buy. The right sequence is education first, then allocation design, then implementation. That is true for gold, stocks, Bitcoin, ETFs, and every other investment.

When DCA may make sense today

DCA into gold may make sense if you want exposure but feel uncomfortable buying all at once after a strong move. A defined DCA schedule, such as six or twelve monthly purchases, can reduce regret risk. The key word is defined. If you keep delaying because the price feels high, you are no longer following a DCA plan. You are market timing.

When lump sum may make sense today

Lump sum may make sense if you have decided on a target allocation and simply need to bring your portfolio to that target. For example, if your investment policy says gold should be 5% of your portfolio and you currently hold 0%, investing to target may be cleaner than slowly drifting toward it. But if the amount is emotionally uncomfortable, a hybrid path is reasonable.

The important part is to choose a rule before the market tests you. Gold can move quickly. Headlines can become dramatic. Without a rule, every price movement feels like a new decision. With a rule, gold becomes part of a portfolio system.

Common mistakes when analyzing gold since 2000

Gold's long-term performance since 2000 can be impressive, but it is easy to draw the wrong conclusion from one start date. A strong article needs to show both the opportunity and the traps.

Mistake 1: assuming the next 20 years must look like the last 20 years

Gold's starting valuation around 2000 was unusually favorable. Future returns depend on future prices, real rates, inflation expectations, central bank behavior, investor demand, and macro conditions. A good past return is not a guarantee of a repeated future return.

Mistake 2: ignoring inflation-adjusted returns

Nominal gold returns can look dramatic, but purchasing power matters. Investors should compare gold not only against dollars, but also against inflation, stocks, bonds, housing, and their own spending needs. A nominal gain is useful only if it improves real purchasing power.

Mistake 3: confusing gold with gold miners

Gold miners may be correlated with gold, but they are businesses. They have costs, management, reserves, debt, political risk, and stock-market risk. A gold mining ETF is not the same as holding physical gold or a gold bullion ETF.

Mistake 4: over-allocating after a strong run

Investors often become interested in gold after it has already performed well. That does not mean it is wrong to buy, but it does mean allocation discipline matters. Buying any asset after a major rally without a plan can create regret if the asset consolidates.

Mistake 5: forgetting fees, spreads, and taxes

Physical gold dealer spreads, storage costs, ETF expense ratios, currency conversion, and tax treatment can all reduce real investor returns. A backtest that ignores costs is useful for direction, but incomplete for planning.

Educational simulation only. Historical performance does not guarantee future results. This article is educational, not financial advice. Always consider your own risk tolerance, tax situation, liquidity needs, and time horizon.

Frequently asked questions

Was gold a good investment since 2000?

Yes, from the 2000 starting point gold delivered a strong nominal long-term return. But the result depended heavily on the low starting price and required patience through multi-year drawdowns and consolidation periods.

Would lump sum or DCA have worked better for gold since 2000?

A lump sum near the beginning of 2000 likely benefited more from the low starting price and long-term rise. DCA was still useful for investors who were adding from monthly income or wanted to reduce timing pressure.

Does gold beat inflation?

Gold can protect purchasing power over certain long periods and can perform well during some inflationary or currency-stress environments. However, it does not track inflation perfectly year by year.

How much gold should I hold?

There is no universal allocation. Some investors hold none, while others use a small allocation such as 5% to 10% for diversification. The right amount depends on your objectives, risk tolerance, and overall portfolio.

Is physical gold better than a gold ETF?

Physical gold offers direct ownership but involves storage, insurance, spreads, and liquidity friction. Gold ETFs are easier to trade and rebalance, but they involve fund structure, expense ratios, and tax considerations.

Can I simulate gold with WhatIfInvested?

Yes. Use the Investment Simulator for quick historical tests or the Premium DCA Calculator for deeper portfolio comparisons with fees, benchmarks, rebalancing, and saved scenarios.