Dollar-cost averaging works best when the process is consistent. The problem is that many beginners do not break DCA with bad math. They break it with skipped contributions, hidden fees, emotional timing, ignored rebalancing, and too much concentration in one asset. These DCA investing mistakes are fixable when the plan has rules.

A strong DCA plan needs rules for timing, fees, rebalancing, and diversification, not only recurring contributions.

The short version: DCA investing mistakes happen when the process is weak

The biggest DCA investing mistakes usually do not come from the formula itself. They come from the investor’s behavior around the formula. DCA can help reduce the pressure of choosing one perfect entry point, but it cannot protect you from abandoning the schedule, investing in the wrong assets, paying unnecessary costs, or increasing risk without noticing.

That is why the best DCA plan is not just a monthly dollar amount. It is a small operating system: what you buy, how often you buy, when you review, how you rebalance, what fees you accept, and what conditions would make you pause or change the plan. If those rules are vague, the strategy becomes easy to break exactly when markets become uncomfortable. Most DCA investing mistakes become obvious once you write the rules down.

Beginner trap

Thinking DCA means “I can invest randomly whenever I feel comfortable.” Real DCA needs a repeatable schedule, because DCA investing mistakes often start with irregular buying.

Better rule

Choose an amount, frequency, asset list, and review rhythm before the market tests your emotions.

Best outcome

A plan that keeps buying through boring months, scary months, and euphoric months without constant second-guessing.

What DCA is supposed to do for a new investor

Dollar-cost averaging means investing a fixed amount at regular intervals, usually monthly, biweekly, or weekly. If you invest $250 every month into a broad ETF, you buy more shares when prices are low and fewer shares when prices are high. Over time, your average purchase price becomes the result of many entries instead of one single entry point.

DCA is especially attractive to new investors because it reduces decision overload. Instead of asking “Is today the perfect day to invest?” you ask “Is my long-term plan still valid?” That shift matters. Most beginners do not fail because they lack access to information. They fail because they face too many decisions, too many headlines, and too many emotional triggers. The best way to reduce DCA investing mistakes is to reduce unnecessary decisions.

However, DCA is not magic. It does not guarantee better returns than lump sum investing. In many rising markets, investing a lump sum earlier has historically had a higher expected return because more money is exposed to the market sooner. But DCA can be easier to follow, easier to automate, and psychologically more comfortable. That makes it useful for investors who are building positions from monthly income or who would otherwise hesitate to invest at all. The goal is to avoid DCA investing mistakes that turn a simple habit into a weak process.

For a deeper strategy comparison, use the DCA vs lump sum guide. To test your own contribution amount and timeline, use the DCA calculator. For an external definition of dollar-cost averaging, Investor.gov explains the concept in its dollar-cost averaging glossary. This article focuses on the operational mistakes that can make a good DCA idea perform worse than expected.

DCA benefit

What it helps with

What it does not solve

What to check

Reduced timing pressure

You avoid betting everything on one date.

You can still panic and stop buying.

Contribution automation and written rules.

Habit building

Investing becomes part of your monthly cash flow.

The habit can fail if your budget is unstable.

Emergency fund, budget margin, and realistic contribution size.

Lower regret

You reduce the pain of investing right before a decline.

You may regret not investing more in strong markets.

Whether lump sum, DCA, or a hybrid approach fits your temperament.

Gradual exposure

You scale into the market over time.

You may underinvest if you keep waiting forever.

Clear deployment timeline and target allocation.

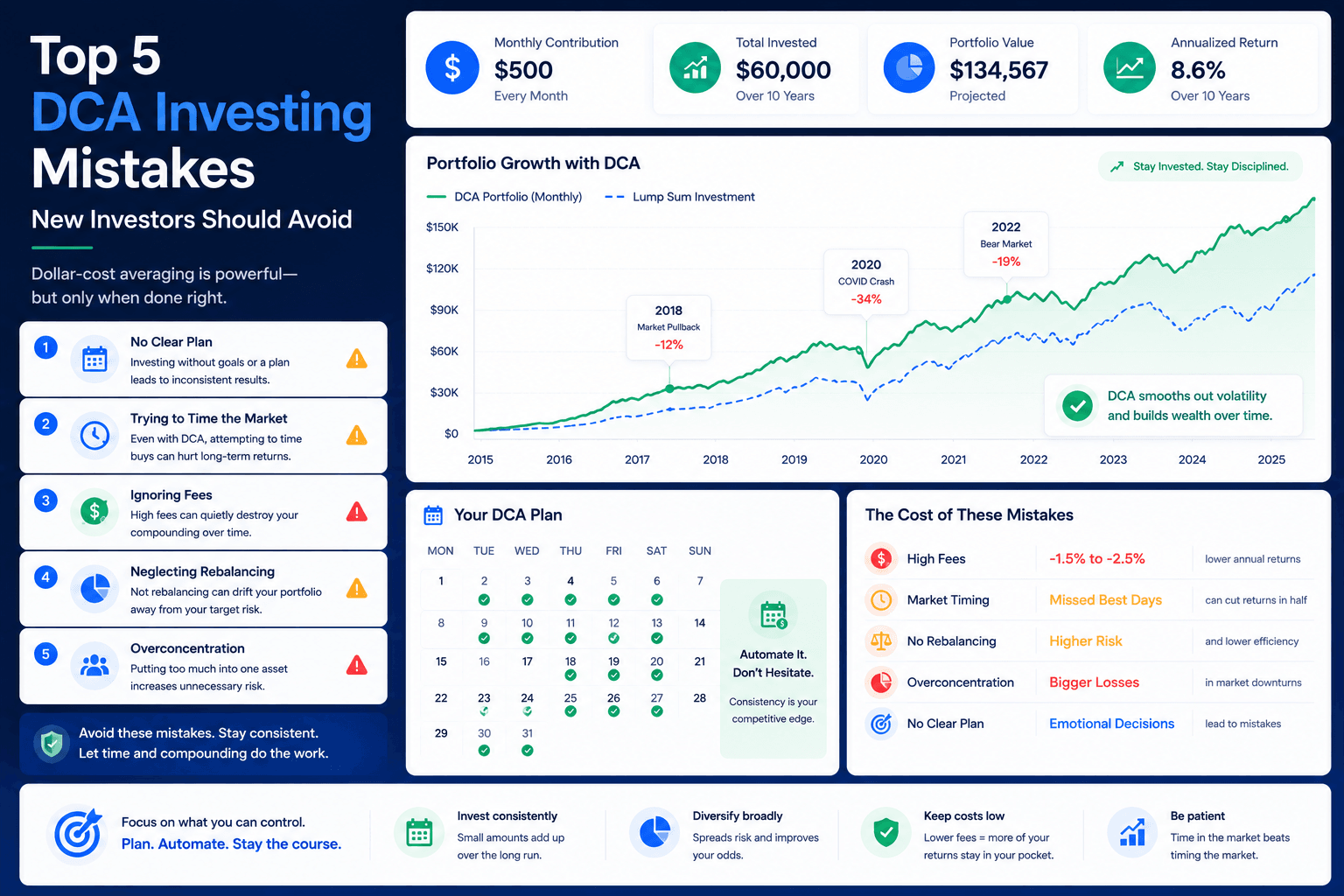

The top 5 DCA investing mistakes and how to fix them

Each mistake below has two parts: the behavior that causes the problem and the system that repairs it. The repair matters more than the warning. A useful investing rule should make the right action easier to repeat, especially when you are tired, busy, or stressed by market news. Treat these DCA investing mistakes as an audit checklist, not as a reason to abandon the strategy.

1

Mistake: stopping after a drawdown

Not sticking to the contribution schedule

The most common DCA mistake is abandoning the plan during a downturn. A new investor starts with confidence, automates a few purchases, then sees the portfolio fall. The next contribution feels uncomfortable, so they pause “just for one month.” That pause often becomes two months, then six months, then a full missed recovery. Among all DCA investing mistakes, this is often the most damaging because it breaks the schedule at the exact moment the plan matters.

This behavior removes one of DCA’s main advantages. The strategy is designed to keep buying when prices are lower. If you stop investing during lower-price periods and resume only after confidence returns, you may end up buying more during comfortable, higher-price periods and less during uncomfortable, lower-price periods.

The same mistake can happen in strong markets. Some investors pause because prices “look too high” and wait for a pullback. Others increase contributions aggressively after recent gains, then panic during the next correction. In both cases, the plan becomes a reaction to emotion rather than a schedule, and small DCA investing mistakes become recurring habits.

Repair rule: automate the contribution, choose a review date separate from the buying date, and write down the specific conditions that would justify changing the plan. “The market is scary” should not be one of them. This single rule prevents several DCA investing mistakes at once.

2

Mistake: letting costs leak quietly

Ignoring fees, spreads, and fund expense ratios

DCA often uses frequent purchases. That makes costs especially important. If every purchase includes a commission, a wide bid-ask spread, or an expensive fund fee, the drag compounds quietly. A $2 fee may look small, but if the contribution is only $50, that is a 4% cost before the investment even has a chance to grow.

Expense ratios matter too. A broad ETF charging 0.03% annually and a similar fund charging 0.75% may feel similar in the first month. Over decades, the higher-cost product can remove a meaningful portion of returns. New investors sometimes focus on the asset’s story and ignore the cost structure that sits underneath the investment.

Fees are not always bad. Sometimes a platform, fund, or tool provides value. The mistake is not paying any fee. The mistake is paying fees without knowing what they are, how often they occur, and how they change your net return. This is one of the DCA investing mistakes that feels invisible until the plan has been running for years.

Repair rule: compare zero-commission options, use low-cost diversified funds for core positions, and test transaction fees in a simulator before committing to very frequent small purchases. Cost awareness keeps DCA investing mistakes from compounding quietly.

3

Mistake: pretending DCA is timing

Trying to “improve” DCA by predicting short-term moves

Some investors start with DCA, then slowly turn it into market timing. They delay the monthly purchase because a recession headline appeared. They double the contribution because a chart looks strong. They wait for a specific price that never arrives. They call this “being smart,” but often it is just emotional timing with extra steps.

DCA’s purpose is to reduce the need for short-term prediction. If you keep overriding the schedule, you reintroduce the problem the strategy was meant to solve. Over time, this can create a messy pattern: too much cash sitting idle, inconsistent contributions, and decisions based on recent price movement instead of long-term allocation. Many DCA investing mistakes start with this exact compromise.

A better approach is to separate tactical curiosity from core discipline. If you want to test whether a lump sum, accelerated DCA, or hybrid deployment would have worked better historically, run a scenario in the investment simulator. But do not let every headline rewrite your core contribution plan.

Repair rule: use a fixed default schedule. If you want flexibility, predefine it: for example, 80% of contributions on schedule and 20% reserved for opportunistic purchases. This separates a planned exception from DCA investing mistakes caused by headlines.

4

Mistake: ignoring portfolio drift

Neglecting rebalancing and asset allocation

DCA can make investors feel diversified because money is being added regularly. But regular contributions do not automatically keep a portfolio balanced. If one asset rises much faster than the others, it can become a larger share of the portfolio than intended. If one asset falls and you never buy enough to restore the target weight, your allocation can drift in the opposite direction.

Rebalancing is not about perfect precision. It is about keeping the portfolio aligned with your risk level. A beginner may start with an 80/20 stock/bond allocation, or a diversified ETF mix, or a small crypto sleeve. Without a rebalancing rule, the actual portfolio can become more aggressive or more concentrated over time. Ignoring this drift is one of the quieter DCA investing mistakes because it happens gradually.

New contributions can help. Instead of selling winners every month, you can direct new DCA money toward underweight assets. This can reduce taxes and transaction costs while still improving alignment. For more advanced portfolios with multiple assets, benchmarks, fees, and saved scenarios, the Premium DCA calculator is designed to model those tradeoffs in more detail.

Repair rule: set a rebalance review rhythm, such as quarterly or twice per year, and define a drift threshold, such as 5 percentage points from target. Rebalancing rules turn DCA investing mistakes into measurable maintenance tasks.

5

Mistake: mistaking conviction for concentration

Over-allocating every contribution to one stock, sector, or crypto asset

DCA can reduce timing risk, but it does not remove concentration risk. If every contribution goes into one speculative stock, one sector ETF, or one volatile crypto asset, the portfolio can still suffer a severe drawdown. Buying consistently does not make an undiversified asset safe. Overconcentration is one of the DCA investing mistakes that can hide behind confidence.

This mistake often happens because one asset has an exciting story. A beginner sees a strong historical return chart and assumes the same path will continue. They start DCA into the winner, then experience the other side of concentration: sharp declines, long recovery periods, and the emotional pressure of deciding whether to keep buying.

Concentration can be reasonable if it is intentional, sized correctly, and understood as a risk. But a DCA plan meant for retirement or long-term wealth building usually needs a diversified core. Single assets can be satellites around that core, not the entire engine.

Repair rule: build a broad core first, then cap concentrated positions. A simple rule is to keep speculative or single-name exposure small enough that a major decline would not derail the full plan. Diversification reduces DCA investing mistakes that come from overconfidence in one asset.

A simple framework to repair your DCA plan

Fixing DCA investing mistakes does not require a complicated spreadsheet. It requires a clear structure that turns investing from a recurring decision into a recurring process. The process below is useful for beginners because it answers the questions that usually trigger hesitation.

1. Define the contribution source

Is the money coming from salary, business income, budget surplus, dividends, or a cash reserve? The source determines how reliable the schedule can be.

2. Pick the default frequency

Monthly is easiest for most investors. Biweekly can align with paychecks. Weekly is usually only worth it if fees and platform rules are friendly.

3. Choose the asset list

Write the assets before you begin. Broad ETFs are often better as core DCA holdings than single stocks or narrow themes.

4. Set review rules

Decide when you will review allocation, fees, contribution amount, and progress. Avoid reviewing too often if it makes you trade emotionally.

The beginner DCA checklist

Before you invest the next contribution, ask these questions:

Can I keep this contribution amount going for at least six to twelve months without stressing my budget?

Do I understand what each asset owns, charges, and represents in my portfolio?

Have I chosen a buying frequency that does not create unnecessary transaction costs?

Do I know when I will rebalance or at least review the allocation?

Have I written down what would make me change the plan?

If the answer to several of these is no, the issue is not that DCA is bad. The issue is that the plan is under-designed. A little structure now can prevent expensive emotional decisions later. This is why the best defense against DCA investing mistakes is a written process.

That structure also makes your results easier to interpret. When the process is consistent, you can judge the strategy instead of wondering whether inconsistent behavior created the outcome.

Which DCA mistakes matter most for your investor profile?

Not every investor is exposed to the same DCA investing mistakes. A student investing a small monthly amount has a different problem from a high-income professional deploying a bonus, and both are different from a retiree trying to reduce timing risk while preserving capital. The strategy may have the same name, but the weak point changes with the investor.

This is why generic advice like “just keep investing” is incomplete. It is directionally useful, but it does not tell you what to watch. A good DCA investing plan should match your cash flow, your account type, your time horizon, and your tolerance for temporary losses. Below are common investor profiles and the specific DCA investing mistakes each one should prioritize.

The beginner with a small monthly contribution

If you are investing $25, $50, or $100 per month, the biggest risk is not that your contribution is too small. The biggest risk is that friction eats the habit before it compounds. Transaction fees, confusing platforms, complicated asset choices, and unrealistic expectations can all make the plan feel pointless. Small DCA amounts need simplicity more than complexity.

For this profile, the best repair is a low-cost platform, one broad diversified fund or a very simple allocation, and an automatic schedule. Avoid the temptation to split tiny contributions across too many assets. Five dollars into ten different positions may look diversified, but it can create tracking headaches and unnecessary cost. A cleaner plan is easier to continue.

The high-income investor with irregular bonuses

Some investors do not only invest monthly income. They also receive bonuses, commissions, tax refunds, business profits, or cash from asset sales. The common mistake here is treating every cash event emotionally. After a bonus, the investor may wonder whether to invest everything at once, DCA over six months, or keep waiting for a better entry point.

A useful rule is to separate normal contributions from irregular cash. The monthly contribution can remain automatic. The larger cash amount can follow a preset deployment plan, such as 50% immediately and 50% over six months, or 25% per month for four months. This turns lump sum vs DCA into a designed choice instead of a recurring debate.

The investor building a multi-ETF portfolio

Once you use more than one ETF, DCA becomes an allocation problem. The mistake is assuming that equal monthly dollars automatically equal a balanced portfolio. If one ETF grows faster or if one asset receives more contributions because it feels safer, the portfolio can drift away from the intended risk profile.

For this investor, rebalancing rules matter. Contributions can be directed toward underweight assets, and a drift threshold can decide when larger changes are needed. This is also where benchmarks become useful. If your portfolio is more complex than a single broad index fund, you should know what you are comparing it against.

The investor using DCA into volatile assets

DCA is popular for volatile assets because it reduces the regret of buying all at once before a large drawdown. But volatility also creates a different danger: emotional overconfidence after strong rallies and emotional exhaustion after deep declines. A DCA investor in a volatile asset needs position sizing rules before the volatility arrives.

The key question is not “Can this asset rise a lot?” It is “Can I keep following this plan if the asset falls sharply?” If the answer is no, the position size is probably too large. A smaller allocation that you can hold through volatility is often better than an oversized allocation that forces panic decisions.

The retirement-focused investor

For retirement investors, DCA is usually less about excitement and more about reliability. Contributions may be going into a retirement account, a tax-advantaged account, or a long-term ETF portfolio. The biggest mistake is letting short-term market noise interrupt a multi-decade plan. Another mistake is becoming too aggressive near the point where the money will be needed.

Retirement-focused DCA should include a review of time horizon. A 25-year-old investor and a 60-year-old investor may both use monthly contributions, but they should not necessarily use the same allocation. As the goal gets closer, risk management, diversification, and withdrawal planning become more important.

Investor profile

Main DCA mistake

Best rule to add

Useful tool

Small monthly investor

Overcomplicating a small plan

Use one simple low-cost core allocation

DCA Calculator

Bonus or lump sum investor

Re-deciding every cash event emotionally

Create a preset deployment schedule

Investment Simulator

Multi-ETF investor

Ignoring allocation drift

Use target weights and rebalancing thresholds

Premium DCA

Volatile asset investor

Oversizing the exciting asset

Cap speculative exposure before investing

Simulator plus Premium scenarios

Retirement investor

Using the same risk level forever

Review allocation as the goal approaches

Retirement and DCA guides

Examples: how the same DCA amount can create different outcomes

Imagine two investors each contribute $300 per month. The first investor uses a broad diversified ETF, pays no trading commissions, and reviews allocation twice per year. The second investor rotates between popular assets based on social media, sometimes pauses during drawdowns, and uses a platform where small purchases create meaningful costs. Both are “doing DCA,” but they are not running the same quality of process.

That difference becomes more visible over time. The disciplined investor may not always choose the highest-return asset, but the plan is durable. The reactive investor may occasionally buy a winner, but the process is fragile. Long-term investing rewards a system that survives market cycles more than a system that looks brilliant for a few months.

Investor behavior

Short-term feeling

Long-term risk

Better alternative

Pauses DCA during market drops

Feels safer temporarily

Misses lower-price purchases and recovery periods

Automate buys and review only on preset dates

Uses high-cost funds or frequent small trades

Feels active and sophisticated

Fees reduce net compounding

Choose low-cost funds and sensible frequency

Chases recent winners

Feels like momentum

Buys after strong performance and increases concentration

Use target allocation and contribution rules

Never rebalances

Feels easy

Portfolio risk drifts away from intent

Review allocation quarterly or semiannually

A 30-day plan to make your DCA system harder to break

The easiest way to avoid DCA investing mistakes is to build the system before the market tests you. A beginner who waits until the next correction to decide how to behave is usually too late. The better approach is to spend one month turning the investing idea into a process. This does not require advanced finance knowledge. It only requires clear choices.

Week 1: clean up the contribution rule

Start with the amount. Many beginners choose a number that feels impressive instead of a number that can survive real life. A $500 monthly contribution is excellent if it is sustainable. It is fragile if it forces you to use credit cards, skip emergency savings, or cancel the plan after two months. DCA rewards persistence, so a boring amount you can repeat is often better than an ambitious amount you cannot maintain.

Next, choose the date. If you are paid twice per month, you might invest after the second paycheck. If you are paid monthly, you might invest two or three days after the paycheck clears. The exact date matters less than the consistency. Your goal is to remove the “Should I invest today?” question from the calendar.

Week 2: simplify the asset list

New investors often confuse diversification with complexity. Owning ten random assets is not automatically better than owning one broad fund. A clean DCA plan usually starts with a core holding that already owns many companies or a balanced mix of assets. Once the core is stable, satellite positions can be added carefully.

Use this test: if you cannot explain why an asset belongs in your plan in one sentence, it may not belong yet. That does not mean the asset is bad. It means your process is not ready for it. DCA works better when every recurring purchase has a clear role.

Week 3: document fees and rebalancing

Write down the annual expense ratio of each fund, any transaction costs, and whether your platform charges currency conversion or spread costs. Small costs are easier to tolerate when you know them. Unknown costs are dangerous because they hide inside the strategy and reduce returns without creating a visible warning.

Then write one rebalancing rule. It can be simple: review allocation every six months and rebalance if a holding is more than five percentage points away from target. If you are still building the portfolio, you may rebalance by directing new contributions toward the underweight asset. That keeps the process practical and avoids unnecessary trading.

Week 4: stress-test the behavior

Before you call the plan finished, imagine three uncomfortable scenarios. First, the market falls 25% after you start. Second, the market rises quickly and you feel you should have invested more earlier. Third, one of your holdings performs far worse than the others for a full year. For each scenario, write the default action.

This exercise is powerful because it separates planning from panic. If your rule says you continue the monthly contribution unless your income changes, you do not need to debate every scary headline. If your rule says you review allocation quarterly, you do not need to rebalance every week. The point is not to predict the future. The point is to reduce the number of emotional decisions the future can force on you.

Minimum viable DCA plan

One recurring amount, one default asset or allocation, one purchase schedule, one review date, and one rule for changing the plan.

Stronger DCA plan

Add fee tracking, a rebalancing threshold, a benchmark, and a written response to drawdowns or missed contributions.

Risky DCA plan

No written rules, changing assets based on headlines, pausing when prices fall, and increasing contributions only after recent gains.

Use tools to make DCA less emotional

The best tools do not replace judgment. They make the tradeoffs visible before you commit real money. Use the free tools for simple planning and the Premium workflow when you need deeper scenario work.

DCA Calculator

Estimate future value from recurring contributions, expected return, time horizon, and compounding assumptions.

Investment Simulator

Backtest simple historical scenarios and compare how past contributions would have behaved.

Premium DCA

Model weighted portfolios, fees, benchmarks, rebalancing, withdrawals, saved scenarios, and exportable reports.

A beginner can start with a simple monthly contribution into one diversified ETF. But as the portfolio grows, the questions usually become more advanced. Should you split contributions across multiple assets? Should you compare DCA with a lump sum? How much do fees change the result? What happens if you withdraw money later? How do you know whether rebalancing helped?

These questions are not signs that DCA is failing. They are signs that your investing process is becoming more serious. At that stage, it is useful to treat DCA as part of a broader portfolio workflow rather than just a deposit habit.

For example, a Canadian investor may contribute monthly across a Canadian-listed equity ETF, a U.S. equity ETF, and a bond ETF. Another investor may use a core ETF and a small satellite allocation to technology or crypto. A retiree may use contributions less and focus more on withdrawals, drawdowns, and asset mix. Each case needs different assumptions.

This is where Premium DCA becomes more relevant. It is designed for investors who want to compare multiple weighted portfolios, include management fees, test benchmarks, save scenarios, and produce a decision-ready report. The free tools are enough for quick tests. Premium is more useful when the plan has moving parts.

Educational simulation only. Historical performance does not guarantee future results. This article is general educational content and is not personal financial advice.

Related guides and tools

Use these next if you want to build a better DCA system instead of just reading about mistakes.

What is the biggest mistake new investors make with DCA?

The biggest mistake is not sticking to the plan. DCA works best when contributions happen consistently through both strong and weak markets. Pausing during downturns can remove the benefit of buying at lower prices.

Can DCA lose money?

Yes. DCA reduces timing pressure but does not eliminate market risk. If the asset declines for a long period or if the portfolio is too concentrated, a DCA investor can still lose money.

How often should a beginner use DCA?

Monthly is usually the simplest frequency because it aligns with budgets and pay cycles. Weekly or biweekly can work too, but only if transaction fees, spreads, and platform rules do not create unnecessary cost.

Is DCA better than lump sum investing?

Not always. Lump sum investing often has a higher expected return in rising markets because more capital is invested earlier. DCA can be better for investors who need emotional comfort, gradual deployment, or a system tied to monthly income.

Should I rebalance a DCA portfolio?

Yes, if your portfolio has multiple assets or target weights. Rebalancing helps keep risk aligned with your plan. You can often use new contributions to buy underweight assets before selling anything.

What tools can help avoid DCA mistakes?

A DCA calculator can model recurring contributions, an investment simulator can test historical scenarios, and Premium DCA can compare portfolios with fees, benchmarks, rebalancing, saved scenarios, and reports.

Are DCA investing mistakes more dangerous for beginners?

They can be, because beginners are still building habits and may not yet have written rules for contributions, rebalancing, fees, and panic decisions. A simple automated plan reduces the chance of turning every market move into a new decision.

Can fees make a DCA plan perform worse?

Yes. Frequent small purchases can be hurt by commissions, spreads, currency conversion costs, and high fund expense ratios. A DCA plan should use low-cost assets and a contribution frequency that does not create unnecessary friction.

Final takeaway

DCA is popular because it is simple, but the simplicity can be misleading. The strategy still needs rules. A strong DCA plan defines the contribution amount, frequency, asset list, fee limits, rebalancing rhythm, and review process before emotions take over.

The top DCA investing mistakes are avoidable: do not stop the plan during drawdowns, do not ignore fees, do not turn every contribution into a timing decision, do not let allocation drift unnoticed, and do not confuse conviction with concentration. If you repair those five areas, DCA becomes less of a hope-based habit and more of a durable investing system.

Start with the free DCA calculator if you need a clean projection. Use the investment simulator if you want historical context. When your plan involves multiple portfolios, fees, benchmarks, withdrawals, or saved scenarios, compare the advanced workflow on the Premium DCA page.